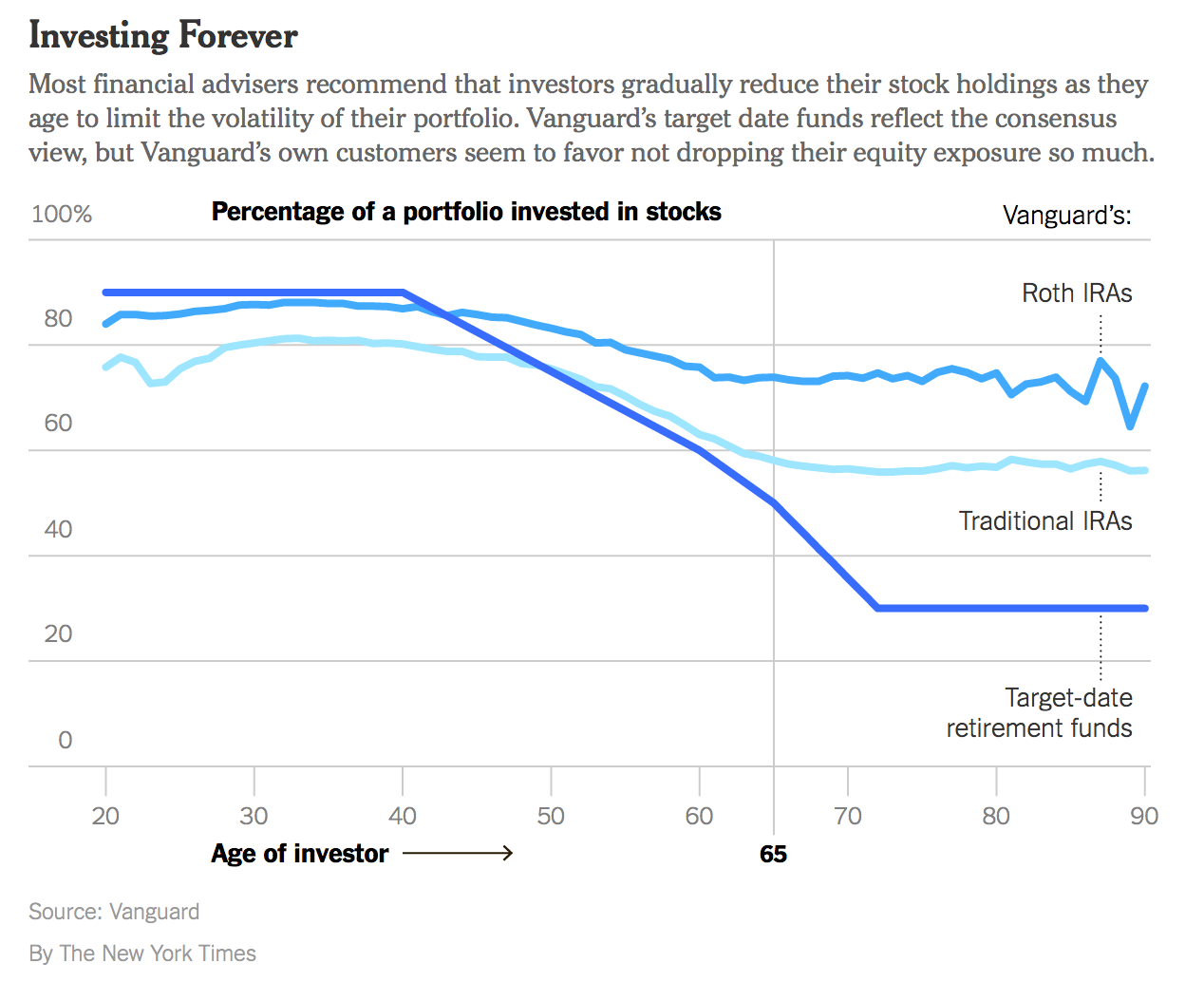

As a follow-up to my last post on 100% stocks forever, the referenced NYT article had some neat data that I hadn’t seen anywhere else. This chart shows how the overall asset allocation of IRAs held by Vanguard change according to the age of the investor. The glide path of Vanguard Target Retirement mutual funds is also included for comparison.

Eyeballing things, it appears that past age 65, Traditional IRAs settle at roughly 58% stocks, while Roth IRAs settle at roughly 67% stocks. This “real world glide path” declines much more gradually than ones from the major all-in-one fund providers, and also stays flat from retirement age onward. For comparison, here are additional glide paths for Fidelity, T. Rowe Price, Blackrock, and American Century, taken from a Morningstar paper. (For this chart, retirement age would be roughly 2015.)

I don’t know any studies that have found the real reason behind the “real world” numbers. I would suggest as a possible explanation that the average percentage must be asset-weighted, and “rich” people have more assets in aggregate. The “rich” don’t need to make big withdrawals (unless required by law), and so they don’t need to spend every penny before they die. They will leave a chunk of money to heirs and thus have a long time horizon. In turn, this longer time horizon would support the holding of more stocks. Roth IRAs are especially useful as an inheritance vehicle as they don’t have required minimum distributions (RMDs), which could also explain why they are even more strongly weighted in stocks.

Meanwhile, if you need to spend down your assets during retirement, then the asset allocation suggested by Vanguard Target Retirement funds (and all the other major target-date funds) would make more sense. But it’s certainly a good point that these one-size-for-all solutions will not apply to everyone.

If you like low costs, diversification, and simplicity but want more control, I would suggest the option of switching to a Vanguard LifeStrategy all-in-one fund that stays fixed at 40%, 60% or 80% stocks. I use the 60/40 LifeStrategy Moderate Growth Fund (VSMGX) as a benchmark for my own long-term portfolio asset allocation.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

It’s generally recommend to draw down Roth IRAs last. Sometimes it’s recommended that Roth IRAs contain assets with the greatest expected return to create the biggest benefit for tax-free withdrawals.

Good post and I think you’re probably right on the reasons. Another (probably less important) thing that can be misleading is that the “fixed income” portion of the portfolio might be held in non-IRA accounts (bank CDs, traditional pensions, etc.). For example, while I’m younger than the people featured here, I work for Uncle Sam and consider that pension to be the fixed-income portion of my portfolio. I am “100% equities” but not really. Also, perhaps the investors consider their paid-off home to be the equivalent of a fixed income asset, but the Lifecycle funds do not take that into account.