Here’s another neat (and free!) portfolio analysis tool – PortfolioVisualizer.com. You can upload a custom asset allocation and get all sorts of backtest data and Monte Carlo simulation results from it. If you register for an account, it will remember your model portfolios for future use.

Here’s another neat (and free!) portfolio analysis tool – PortfolioVisualizer.com. You can upload a custom asset allocation and get all sorts of backtest data and Monte Carlo simulation results from it. If you register for an account, it will remember your model portfolios for future use.

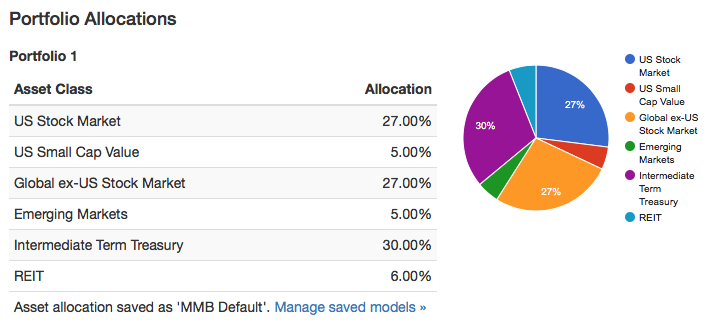

I created a custom portfolio “MMB Default” similar to my current portfolio asset allocation and below are selected charts that were produced. Here’s the summary:

Historical portfolio growth and annual returns. (Note that the time period shown was limited because the available data for Emerging Markets only went from 1995-2017. Apparently there are some ongoing issues with data licensing.)

Historical drawdowns during the same period. This provides a good feel of how “painful” it was to hold this portfolio. 2009 was certainly a stressful year when both our portfolio and future job prospects were being questioned.

Monte Carlo simulation of 4% withdrawal rate over a 30-year retirement period. I used my custom portfolio and had it simulate a withdrawal rate of $40,000 from a $1,000,000 portfolio (4%), adjusted annually for inflation, for a 30-year period. You can alter nearly all of these variables (withdrawal rate, inflation adjustments, period length, etc). Monte Carlo basically looks at many possible trajectories based on historical asset return characteristics. If things turn out well, you end up with a “runaway” portfolio, but if they don’t you can hit zero pretty fast.

The success rate looks at the percentage of simulated scenarios that end up with a positive value at the end of the period. At a 4% withdrawal rate for 30 years, it was 95%. At a 5% withdrawal rate for 30 years, it was only 84%. At a 5% withdrawal rate for 50 years, it was only 69%.

Here’s where I warn you that Monte Carlo simulations are not the end-all of portfolio safety. You can’t predict the next 50 years when you can barely look back 50 years. Living off a portfolio for decades involves not just a reasonable rate of withdrawal but planning as to how you could cut expenses or create additional income if conditions go sour for an extended time period. I’d rather have 90% theoretical safety and a flexible backup plan over 99% theoretical safety and no backup plan.

Portfolio Visualizer has several additional features that I may never use, but even the above is enough to make it a very interesting tool for the DIY investor. I hope they get their data source issues sorted out eventually. You can find all of my posts about portfolio tools in the Tools & Calculators category.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Cool post! Thanks for sharing! I’ll have to check out Portfolio Visualizer.

Love to see the graphs from the simulations. Thanks for sharing the tool!

Jordan @ NewRetirement

I’m a little confused on the monte carlo graph. Maybe I’m over analyzing.

Starting value is $1M and all three values show increases, which does not make sense as you would be drawing $40K/yr. It looks like you would be still drawing but because the market continues to move upward, your portfolio will still have increases.

Can you explain further the three trajectories and what they represent?

I think you have it right. If the historical average return is say 8% a year then you would on average have an ever-increasing balance when only withdrawing 4% a year. The charts above only show 25th/50th/75th percentile. In terms of running out of money, you’d be more worried about a series of negative returns in the beginning which would probably be in the 5th percentile or lower. There are other Monte Carlo simulators that do show these lines.

So what you are saying is the 75th percentile represents my $1M grew over 30 years to $7.3M even though I was pulling out 4%.

That seems counter to every other article I’ve researched, but maybe it is like that because most would have this rebalanced in retirement to a more conservative approach. Which would lead to less than an 8% average return and would steady draw the portfolio down to $0 after 30 years. Am I off on this logic?

Personally I still have not grasped the full concept of retirement rebalancing to a very conservative portfolio because you can still use low cost indexes that can have growth over the life of the portfolio which would provide even further longevity.

BTW, love the blog and have been a reader for years. Many of your posts I have saved in my email for referencing later.

I don’t know the details behind the results, but a quick calculation shows that 7.3X initial balance over 30 years would require a 6.8% annualized return. Add in 4%, that’s 10.8%. Historically, that is above average but we are talking the 75th percentile so that’s by definition above average. Also, we’re probably talking a preferable sequence of returns?

Hi Jonathan,

portfolio visualizer once was for free but nowadays it costs. The question is probably quite late but can u recommend other tools that are for free? I just found https://portfoliometrics.net/ but maybe there are other options?