![]() I lent out my first $25 to a stranger on Prosper nearly 8 years ago, in October 2007. Since then, the peer-to-peer (P2P) lending environment has undergone a variety of changes. I’ve made hundreds of P2P loans both hand-picked and algorithm-driven, sold them on the secondary market, and experienced the effect of defaults on my returns.

I lent out my first $25 to a stranger on Prosper nearly 8 years ago, in October 2007. Since then, the peer-to-peer (P2P) lending environment has undergone a variety of changes. I’ve made hundreds of P2P loans both hand-picked and algorithm-driven, sold them on the secondary market, and experienced the effect of defaults on my returns.

I’ve written several posts along the way, but here is my condensed (but still detailed) overview. Many of the other Prosper reviews tend to focus on the positives. While Prosper certainly has potential, I’d rather go deeper into the possible risks to an investor’s hard-earned money.

The attraction: Be the bank. Earn high interest rates. We’ve all seen the big banks charge mountains of interest, while us regular folks pay it. The average interest rate on credit card loans remains around 15% APR. The basic model for P2P loans is that anyone can become that bank and invest in loans to other individuals. Prosper will take a little cut for helping out, but the bulk of the interest (and risk) goes to the investor.

The reality: Higher net returns than other alternatives, but the risks hide in the details.

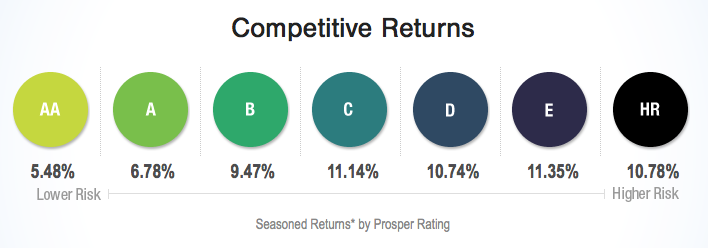

Detail #1: Significant loan defaults occur over time. The good news now that P2P loans have been around for a while is that you have more historical performance numbers to consider. Prosper lets you see this historical data in great detail, but you have to look carefully. Here’s a snapshot of what you’d see now at Prosper.com/Invest, labeled “Seasoned Returns*”.

Here’s what that asterisk means:

*Seasoned Return calculations represent historical performance data for the Borrower Payment Dependent Notes (“Notes”) issued and sold by Prosper since July 15, 2009. To be included in the calculations, Notes must be associated with a borrower loan originated more than 10 months ago; this calculation uses loans originated through May 31, 2012. Our research shows that Prosper Note returns historically have shown increased stability after they’ve reached ten months of age. For that reason, we provide “Seasoned Returns”, defined as the Return for Notes aged 10 months or more.

The initial interest rate on your notes is only a theoretical maximum return. For example, for the last quarter of 2015, the average interest rate was 11.06% for 36-months 15.47% for 60-month loans. Every time a borrower defaults – and trust me, if you buy any meaningful amount of notes, some will default on you – your return will go down. With loans as little as 10 months old, their quoted “increased” stability is not the same as stability.

Here’s a chart from competitor LendingClub showing how net annualized return has decreased with loan age (for different vintages of past loans). Note that the net return numbers still keep going down after 10 months.

If anything, I would prefer to use this alternative table provided by Prosper. These estimated net numbers are more realistic. The table also includes a daily snapshot of their current inventory, which may give you an idea of relative availability by rating. Note that there are much fewer of the highest-risk, highest-expected return loans available.

Finally, don’t forget that not everyone gets the average. You can’t buy a “Prosper index fund”. You may be above average, but be prepared for below-average returns as well.

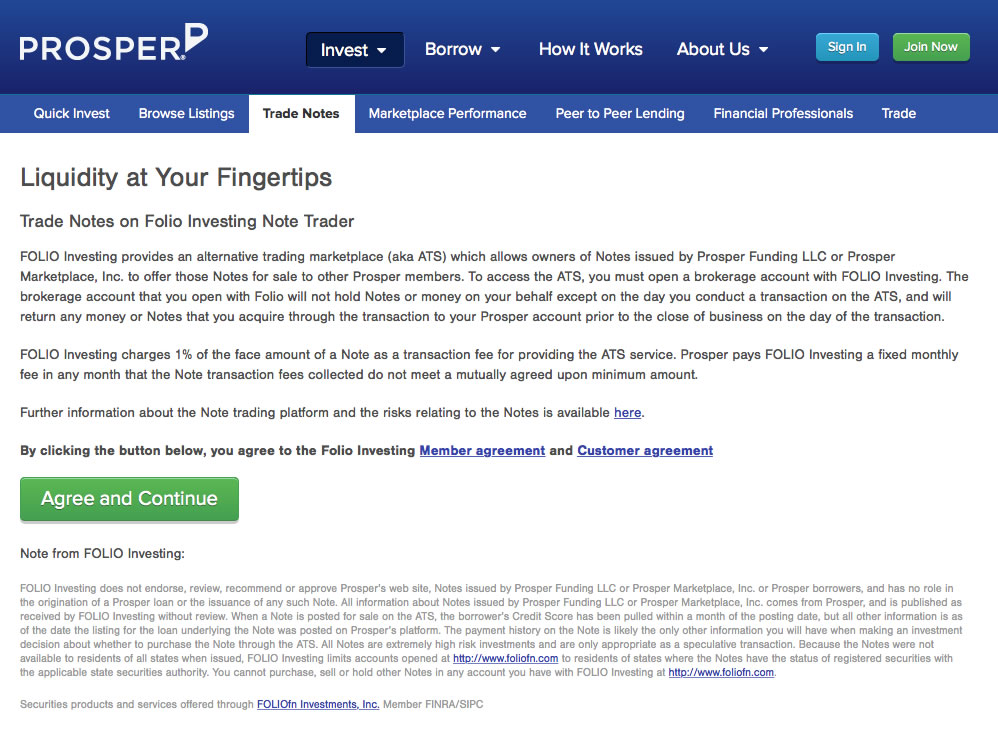

Detail #2: Liquidity concerns. When you buy traditional mutual fund that holds investment-grade bonds, with just a few clicks, you can sell that investment on any given trading day. You will get a fair market price, and you will find a buyer for all of your shares.

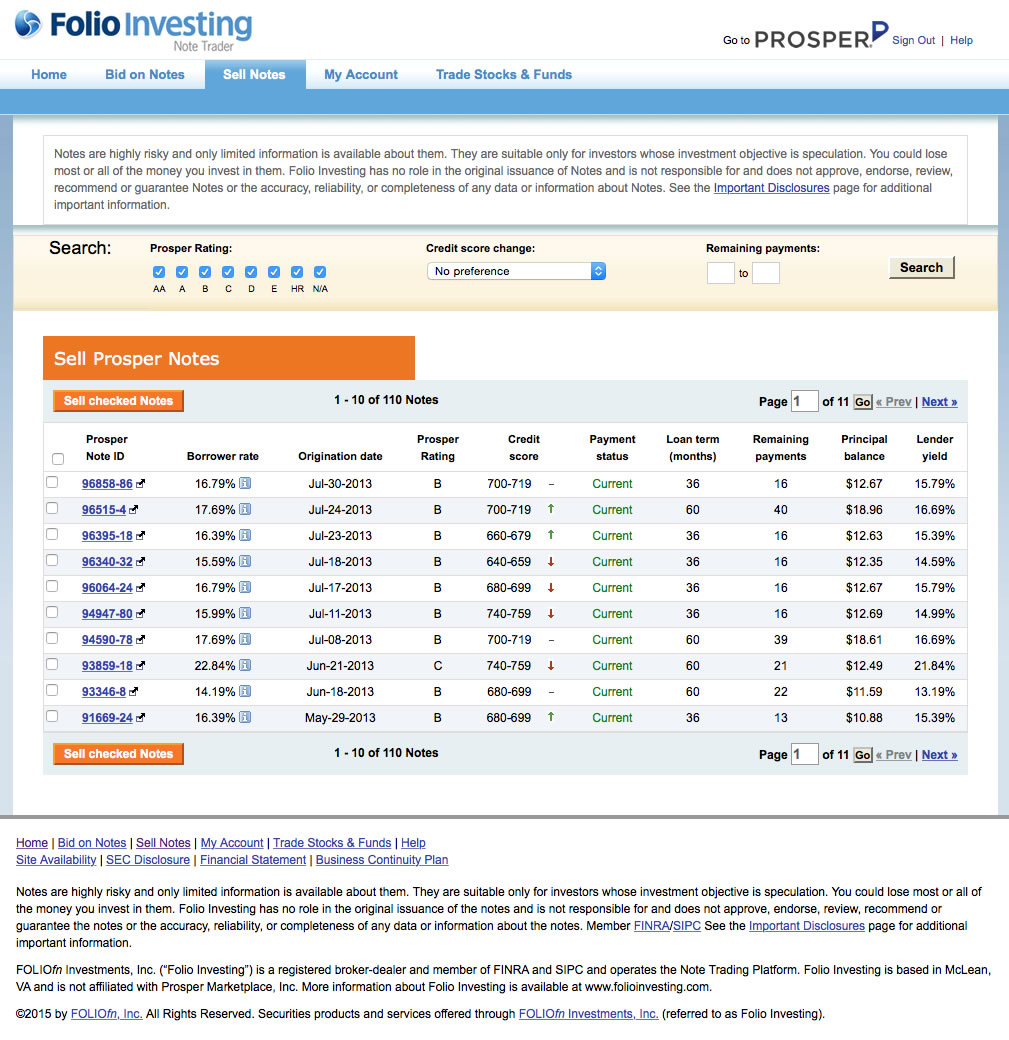

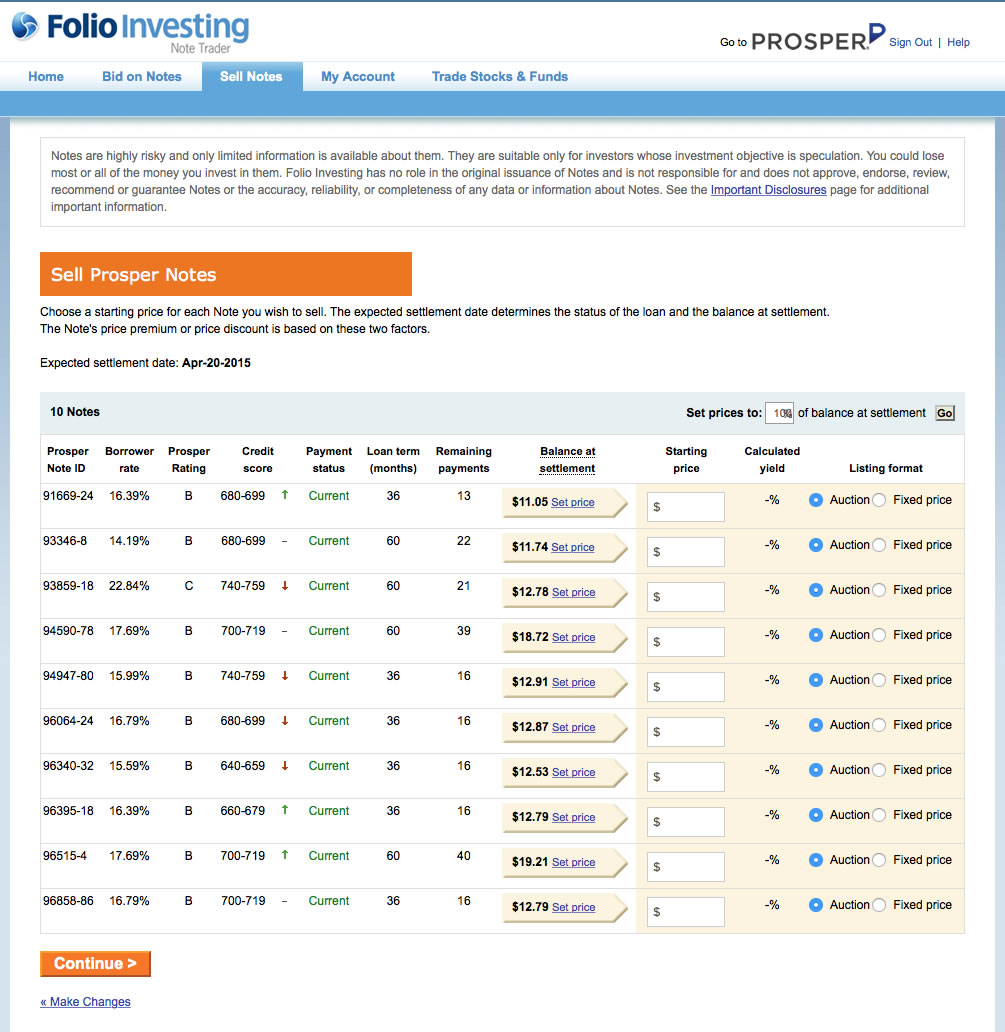

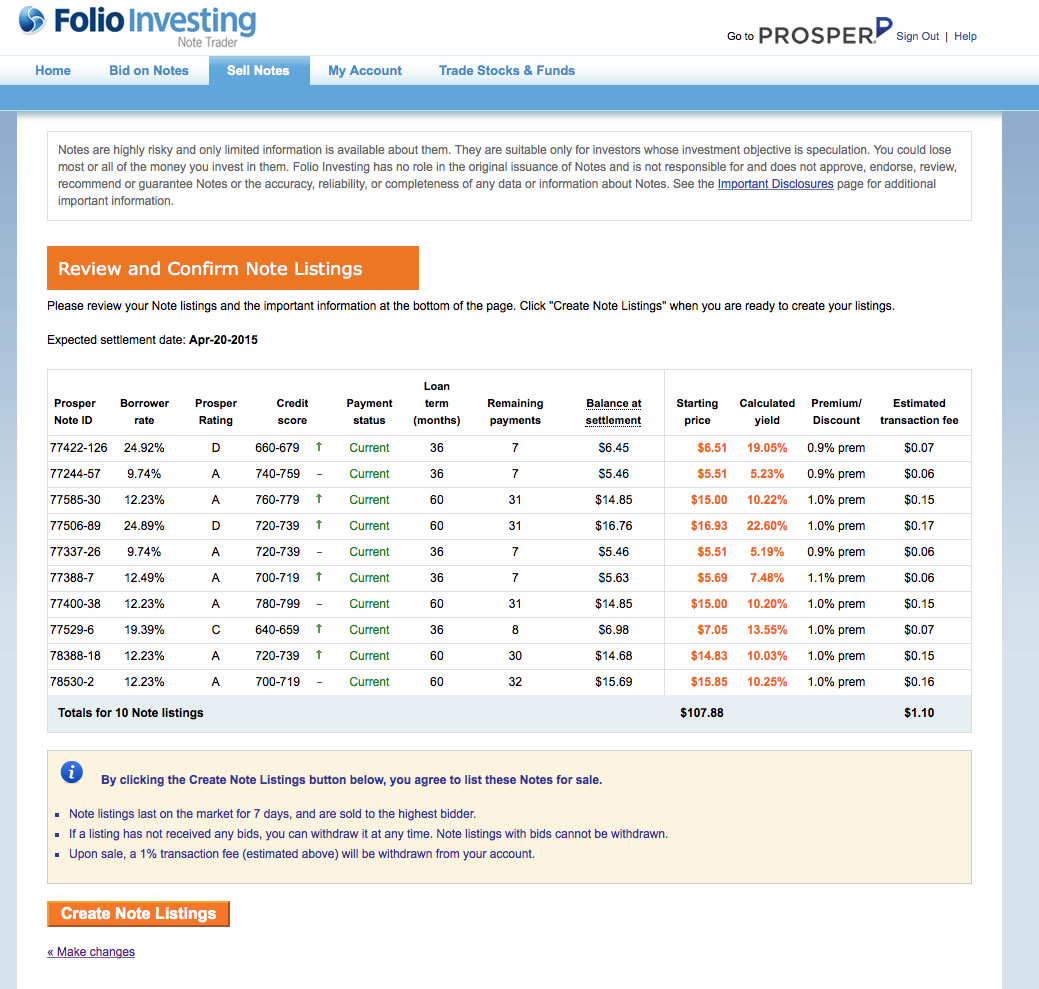

If you invest in a Prosper note and you need to cash out before maturity, you will have to sell on the secondary market. Now, if you have pristine loans with a perfect payment history, today you’ll probably be able to sell your notes at near or even slightly above face value. But here are the possible haircuts:

First, you will have to pay a transaction fee of 1% of face value on all sales. Second, if you have loans that have ever been late or has a borrower whose credit score has decreased since loan origination (they track that), you will have a harder time finding a buyer and the price will probably be lower than face value. Finally, for Prosper if your loan is currently late, you can’t sell it on the secondary market for any price. You can’t even offload it for a penny.

In my experience, I liquidated ~85% of my loans at about a 0% net haircut, ~10% were sold at a slight loss due to their imperfect history, and ~5% could not be sold at all. While this is certainly better than having no liquidity at all (like a lot of real-estate crowdfunded debt), it also takes a few hours of work at least to maximize your selling prices on 100 or 200 loans.

All of these haircuts taken together can take a significant hit against your total returns. Also, just because you have buyers today doesn’t mean there will be buyers tomorrow. Therefore, I would not invest if you don’t expect to hold the loan until maturity. Some people try to arbitrage things by buying notes and selling them quickly on the secondary market to residents of states that can only buy notes on the secondary market.

Detail #3. Diversification is critical. A defaulted loan wipes out both principal and interest, resulting in a big hit on your overall return. Therefore, your best bet is to never put any more than the $25 minimum into any one note. Remember this statistic: For Notes purchased since July 2009, every Prosper investor with 100 or more Notes has experienced positive returns. In other words, no investor has lost money overall if they held at least 100 notes! 100 times $25 = $2,500 which I think is the minimum you should invest with.

Detail #4. Taxes. P2P notes are a somewhat different animal, and at year-end you’ll receive some tax forms that will be unfamiliar to most people. These may include:

- 1099-OID

- 1099-B (Recoveries for Charge-offs)

- 1099-B (Folio secondary market)

- 1099-MISC

If you file your income taxes yourself, it is not impossible to figure out but it will take some extra research and effort. Here is my Prosper tax guide that offers some guidance. If you pay a tax professional, they may charge extra for the added complication.

For the most part, the interest you receive will be taxed as ordinary income, the same rate as interest from bank savings accounts. This can be quite high depending on your income, so you may want to consider holding your Prosper notes inside a tax-sheltered IRA. Looking back, I wish I put my Prosper notes inside an IRA.

Detail #5. Automatic investing. The days of hand-picking loans are pretty much over. I recommend using the Quick Invest feature that Prosper offers in order to automatically filter through and buy the notes that fit your criteria. Loan supply is often limited, and this way you can actually get those loans before someone else buys them.

You can let Prosper pick the loans for you, or you can spend your time looking for “better” filters. There are some free tools out there that help sift through the past performance data. There are even paid services out there that do this for you, but I am uncertain how the cost/benefit would shake out.

Detail #6. Past performance vs. future possibilities. Although past returns are great, another economic recession may have a severe impact on your future loan returns. In the end, these are unsecured loans like credit card debt. If people lose their jobs, they will stop paying. Just because nobody has lost money in the past with 100+ loans, that doesn’t guarantee that you won’t lose money in the future. Unlikely does not mean impossible.

Traditionally, high-quality bonds are a diversifier to stocks. But Prosper notes are more like low-quality bonds. If the economy tanks, defaults will rise and your returns will drop. But if the economy tanks, your stocks will drop too. Are you ready for both to suffer significant drops during times of financial stress?

Detail #7. What if Prosper goes bankrupt? As a company, Prosper Marketplace Inc. (PMI) has historically had a hard time actually making a steady profit themselves. In 2013, Prosper started structuring their notes so that they are held in a new legal entity called Prosper Funding LLC (PFL). This remote entity is designed to stand alone and be protected from any creditor claims in the event that Prosper Marketplace, Inc. goes bankrupt. PFL can keep on running and servicing loans. This is a good move in my opinion, but it is still unknown how well this legal strategy will work, or if future lawsuits can put the assets of PFL at risk.

In other words, don’t put all your eggs in one basket. Due to #6 and #7, Prosper notes should only be a portion of your fixed income assets.

Summary. P2P loans are becoming a legitimate asset class, gathering billions of dollars from Wall Street and other institutional investors. Interest rates remain low, and thus the high yields and competitive past returns from these Prosper notes are still very attractive. Let’s face it, even a tempered expectation of 8% net annual return is hard to ignore! But before you make the jump, make sure you fully understand the risks and how to best mitigate them.

- Understand that your final returns will be significantly less than your starting yield. Look at historical numbers for guidance.

- Don’t invest money you will need before the loan ends (3-5 years).

- Diversify across as many loans a possible (100+ notes).

- P2P notes should only be a portion of your fixed income assets.

- Expect to spend extra time to acquire notes and prepare taxes.

- Consider holding notes inside a tax-sheltered IRA.

I hope that this information helps you decide whether investing in Prosper loans is right for you.

Bloomberg has a new article about how hard money loans to house flippers are the next asset class to be both crowdfunded and taken over by institutions. Like peer-to-peer loans and LendingClub, it may have started out with individuals lending to other individuals, but there is still a lot of money looking for higher yields and that means Wall Street is coming. The catchy title is now

Bloomberg has a new article about how hard money loans to house flippers are the next asset class to be both crowdfunded and taken over by institutions. Like peer-to-peer loans and LendingClub, it may have started out with individuals lending to other individuals, but there is still a lot of money looking for higher yields and that means Wall Street is coming. The catchy title is now

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT.

I’m not sure exactly what details of this investment I am allowed to share, so I’ll save that part for later. It will be good for you guys to pick apart, but it doesn’t really matter for other investors as the project is already 100% funded. I’m just waiting on my first interest payment in May, and hope to be done by October. At the end of the year I will get a 1099-INT. I started following Jonathan’s blog about five years ago because I shared the same interest in personal finance and the goal of early retirement. I’ve made a lot of investing mistakes over the years, but with my 40th birthday coming up later this month I thought I’d share my approach which had the primary goal of income generation and capital preservation.

I started following Jonathan’s blog about five years ago because I shared the same interest in personal finance and the goal of early retirement. I’ve made a lot of investing mistakes over the years, but with my 40th birthday coming up later this month I thought I’d share my approach which had the primary goal of income generation and capital preservation. Being a peer-to-peer lender been a bumpy ride.

Being a peer-to-peer lender been a bumpy ride.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)