(Updated. Lending Club ended their first day of trading at $23.43 a share, up 57% from their IPO price. With roughly 361 million outstanding shares, LC is roughly a $8.5 billion dollar company! I have updated the post to include the rest of the IPO documents and process. I ended up selling my 100 shares for roughly a $800 gain during the first day of trading. Details and rationale below.)

LendingClub connects individual borrowers with individual lenders, and I’ve been writing about them since 2007. They successfully had their IPO on Thursday, December 11th, 2014 and they actually set aside a few shares for individual investors. Usually you’d either need serious cash or insider access. If you were an investor at LC by 9/30/14 you should have gotten an e-mail asking if you were interested.

I participated in this IPO for a few reasons:

- I’ve been a lender on LendingClub since 2007 and have been following their progress since.

- I have never participated in an IPO before, and am curious about the process.

- I view this investment as purely speculative. It is not an investment, it is a gamble!

- I can commit as little as $250 and up to about $5,000 (details below). I can choose a number that will keep my interest but it won’t break the bank either way.

I’ve documented the process below:

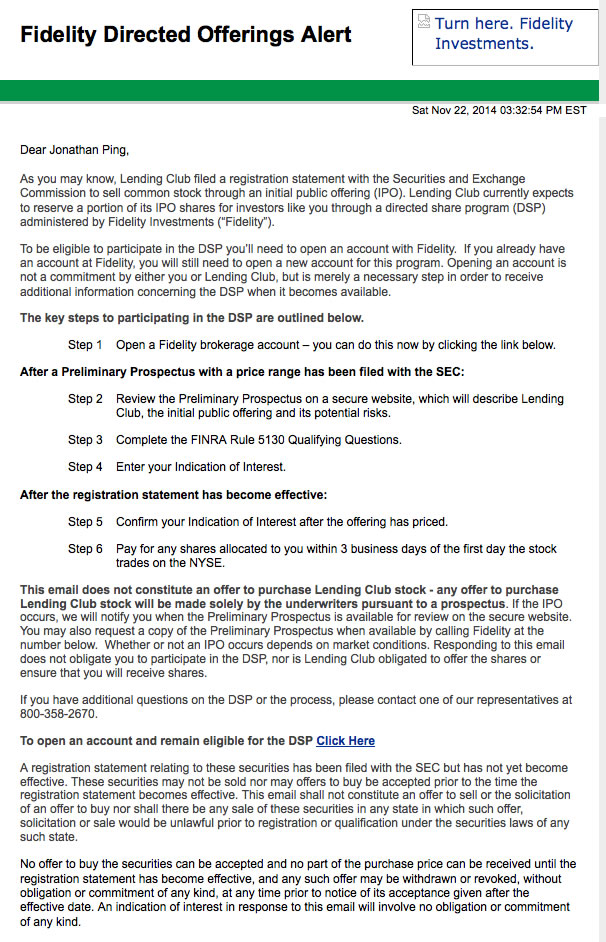

11/17/2014. I got an e-mail with the subject “Lending Club IPO – Directed Share Program (DSP)” telling me that I was eligible to participate and that I had to opt-in to sharing my information with Fidelity Investments. Here is a screenshot:

I clicked, and then was instructed to wait. (More below)

11/22/2014. I got another e-mail with the subject “LendingClub Corporation Directed Share Program – Notification of Eligibility” telling me that I had to open a new brokerage account with Fidelity to be eligible for this IPO.

Since I already had a Solo 401(k) and an existing taxable brokerage account with Fidelity, the process only took a few minutes and was completely online. More waiting…

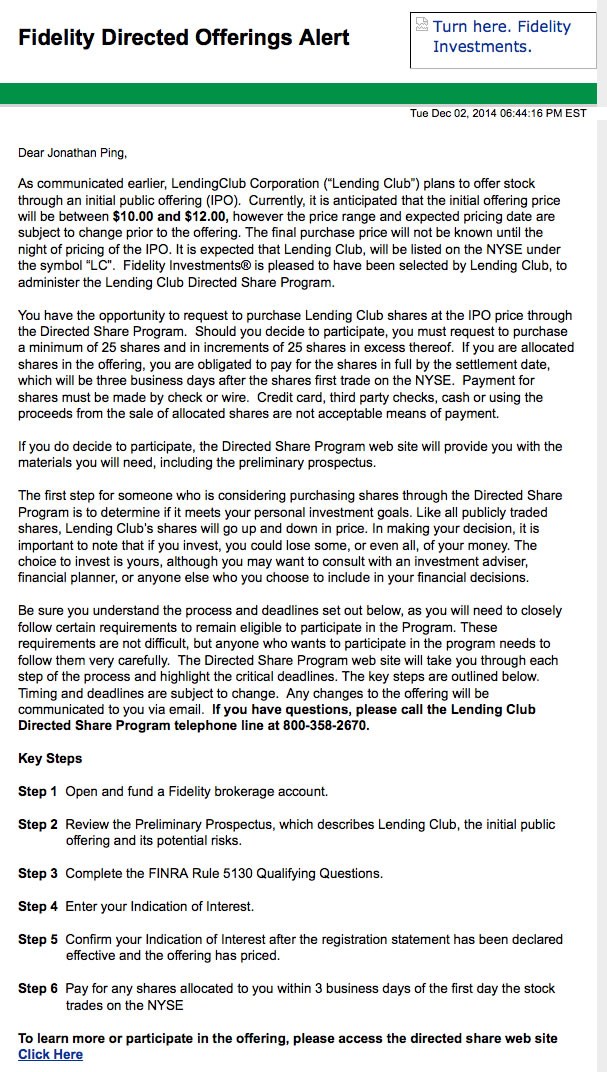

12/2/2014. Another e-mail arrived with the subject “LendingClub Corporation Directed Share Program” with more details. The estimated price range for the IPO was $10 to $12 a share. I would be able to commit to a minimum of 25 shares and a maximum of 350 shares in 25 share increments. So that would mean an estimated range of $250 to $4,200. Not serious money, but still an nice gesture towards their customers.

I was also able to review the Preliminary Prospectus, complete the qualification questionnaire, and confirmed my indication of interest. A lot of the prospectus had to do with the mechanics of LendingClub and how they make their money; I was already familiar with that. Is roughly $6 billion a fair valuation? Their revenue all depends on the future loan volume growth. If they can get more and more people with credit card debt to refinance into a lower-interest loan with LendingClub, they’ll be set. The demand for loans from Wall Street and institutional investors is definitely there.

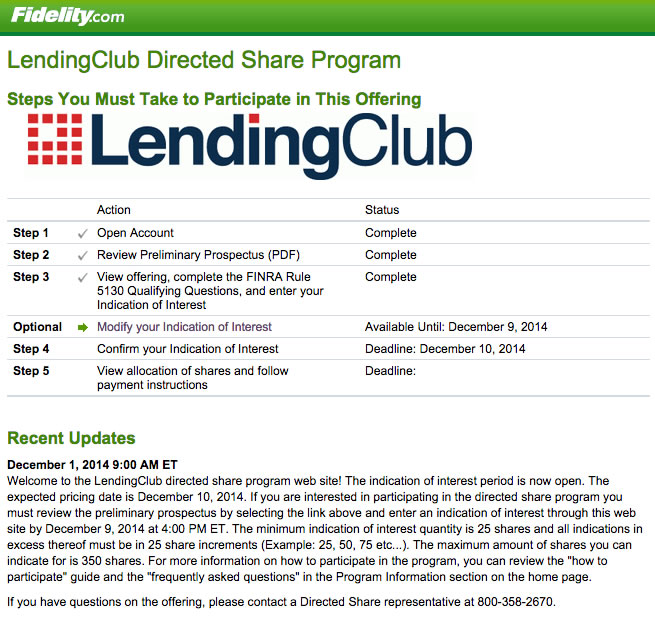

I indicated interest for maximum 350 shares. I don’t even know if I’ll even get that many. I funded my account already; this is essentially money that used to be invested in LendingClub loans. It looks like I’ll have to come back on December 10th to confirm everything and see if they updated the expected share price and share availability.

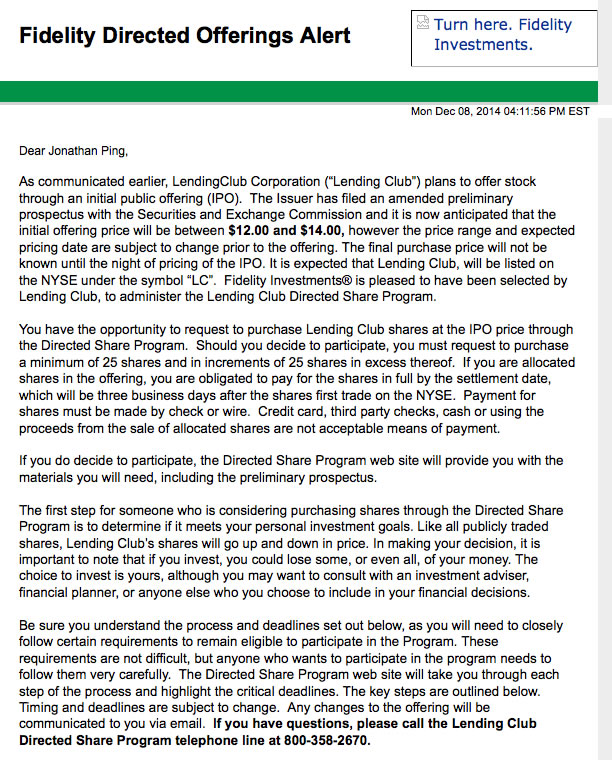

12/8/2014. I received an update that the estimated range was increased to between $12 and $14. Seems like there is some decent buzz around this IPO.

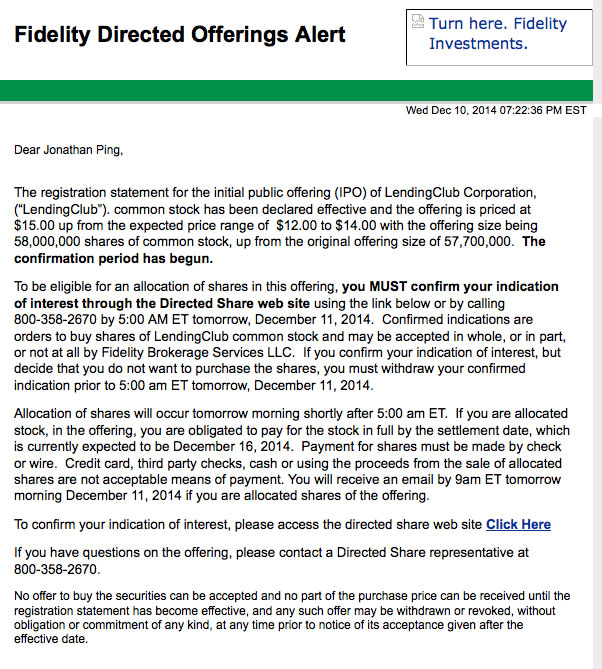

12/10/14. Another e-mail tells me that the confirmation period has begun. The price has increased to $15 a share, and I need to make final confirmation of my interest. $15 a share is 25% higher than the initial top range estimate of $12. This gave me the feeling that they are just pulling numbers out of the air (which they probably are). That’s the thing about growth stocks. It all depends on the future, and even slight adjustments to a forecast can change the share price significantly. Given that I was only hoping for a 25% “pop” in the first place and wasn’t sure that LendingClub was $5.4 billion company, I decided to scale back my commitment to 100 shares. Remember, most tech IPOs don’t do that well.

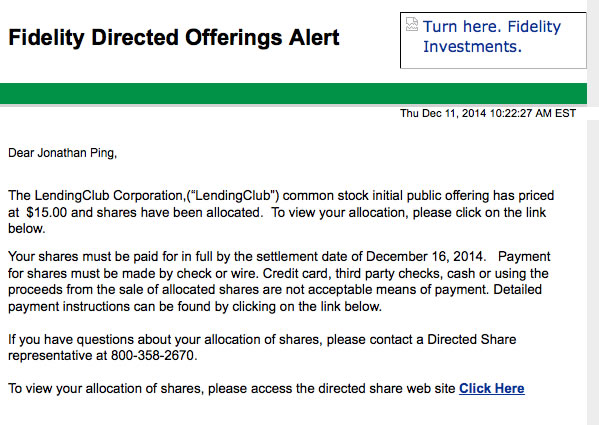

12/11/14. I received my “LendingClub Corporation Directed Share Program Notification of Allocation”, where I learned that I had gotten my 100 shares. Based on reports, people who asked for the max 350 shares ended up getting 250 shares.

I quickly looked to see what the market price was, and saw that it had gone as high as $25.44 and was currently around $23. That would make LendingClub a $8.5 billion company! After about 30 seconds of thought, I decided that would take the 50%+ instant gain and get off the ride. I am more comfortable with value investments rather than growth. Anything trading at 40 times projected revenue (not profit, revenues, LC is losing money so far this year) is not my cup of tea.

I sold my 100 shares a $23 for roughly an $800 gain. Here’s my transaction screenshot:

The whole process was entertaining and educational. I still think that Lending Club has a lot potential, but apparently so do a lot of people. Congratulations to the others who committed to more shares and are looking at even bigger gains. Will you keep them or have you already sold them to lock in a profit?

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Me too…interested to see how it goes…

I am doing this too, purely for the novelty of participating in an IPO.

I actually don’t really like the investment. The majority of their revenue is a front end origination fee on each loan – and these fees seem quite high (1%-5%) and might be a barrier to them to really taking on a substantially higher portion of consumer credit card debt. I originally thought a much more substantial part of their business was from their nickeling and diming with 1% fees on all payments.

I also have a pessimistic feeling since they are sharing the IPO with Joe Nobody investors. Hopefully this doesn’t mean they’re short on institutional demand.

All that said, I have no idea what this stock will actually do, so let’s spin the roulette wheel on a couple of K!!

I signed up with their program, but didn’t receive any follow up emails where it notifies that the prospectus is out. Wierd.. I even looked in my spam folder.

I would contact them by phone if you are still interested. You have until December 9th. The phone number should be on one of the screenshots above.

I believe more of their business now goes to other lenders versus the average joe investor. I have been disappointed in the quality of borrowers, lack of borrower information, and low rates paid based on my perceived risk.

Hi Jonathan,

Thanks so much for your blog! Been reading it for many years now.

I recently moved to California, from a state that didn’t allow me to have an LC account. I’m therefore looking to open up an account. I read your previous posts on LC, but had a few questions:

1. I’m assuming that if LC goes belly-up, all our money is lost. Is that correct?

2. Is filing taxes on LC gains, or would you recommend opening an IRA?

3. Do you have any referral links?

Thanks!

Aj

Hey Jonathan how many shares are you in for? I’m probably going to do a couple hundred!

the price just jumped again to $15….still in?

If LC is not making loans to oil companies, this might not be on the same sinking ship as a lot of the other banks who lent a lot to oil interests soon to go belly up! it might be insulated from any of the fallout amongst financials that might ensue.

Yes, but only for 100 shares. We’ll see what happens. 🙂

Jonathan – were you allocated any shares? I was in for the max (350) but I have yet to receive an email stating that I was allocated anything.

Not sure what is going on, I did all the steps and so far the website is not allowing me to confirm shares, nor view allocated shares. Anyone have confirmation yet?

Just look into your Fidelity portfolio, the email link is still broken for me.

I did get my requested 100 shares. I sold all of the them at $23 after I got the e-mail from Fidelity (hours after actual trading had begun). I think LendingClub has a lot of potential but I already know that I don’t like being an individual growth stock investor. Dividend stocks maybe, but not growth stocks.

I had reserved 75 shares. I put $1500 into my fidelity account. When they got transferred, it just took the money out of my account. As of 11:39 EST I have a gain of $588 on my shares

I asked for 350, got 250. Dumped them at $24+change shortly after trading started. I realize this may poison me at Fidelity for getting into IPOs in the future, but that’s not something I care about anyway.

Nothing against Lending Club, but I simply am not qualified to evaluate their business at a level where I’d want to be investing in their stock and I’ve been reducing my portfolio in both Lending Club and Prosper. They were fun for a bit, but I’ve moved on.

FWIW, this is my 3rd participation in a directed share program. I was lucky enough to be invited into the VA Linux and Red Hat programs back when they went public in the tech bubble. I’m in a much different place financially today than then, so it was much easier to make the decision to pull the trigger.

That makes me feel a little better…I thought about asking for the full amount and while I do have some cash to throw around, I don’t have tons of it. I probably could have felt pretty secure with about 150 shares. I didn’t notice it had started trading until 30 minutes after it started and noticed it dropped a bit and was continuing dropping. I thought about dumping and buying back, but then it started to recover.

I’ve been moving money out of Lending Club for a few months now…Seeing all the loans being “Debt Consolidation” and that no one elaborates the reason for why they want the money gives me a pause to lending to them. (I asked LendingClub about that and they said something about privacy or something) Plus seeing 22 out of 100 loans go bad really hits the bottom line. I put about $700 into them in early 2008 and only having a 3.64% return is not great.

I asked for 350 and got 250. Trying to decide if I take a quick profit minus taxes of course or hold.

Thoughts?

I’m thinking about holding…my taxes next year are going to be less (I’m self employed and some of my big sales this year aren’t going to happen next year). Look at Facebook, I was going to spend $700-$1000 on the open and when the price jumped and then dropped I would have been way down. I didn’t do it because I couldn’t get money to my account fast enough. If I had bought and held at $35 (or whatever it was), I would have doubled my money now.

Same with me. Asked for 350, got 250. I do not plan to dump them because Fidelity is my primary brokerage. I don’t want to sour the relationship and lose future opportunities.

I agree it’s quite hard to evaluate their business since there is really no one else to directly compare them to. But I plan to hold on to the shares because a) they are the biggest player with first mover’s advantage, b) the regulatory hurdles are pretty big, so it will be quite hard for a newcomer to disrupt the market, c) I believe they have plenty of untapped opportunities, e.g. expansion into auto loans, student loans, etc.

Why do you think it would impact your relationship with Fidelity? Yes they had to set up an individual account which cost something but maintaining it does too. They earned two commissions and now presumably have no on-going costs. I’m just not sure why Fidelity would consider it detrimental to them.

I asked for 350 and ended up getting 250. Sold 150 earlier at 23 and change. Will hold the 100 and see what happens. Fidelity is not my primary brokerage. Wish I would have received the full 350 allotment!

I’ve got 4 brokerage accounts…and would like to get it down to 2.

Had to get a scottrade account to get some company stock with a company I used to work for (Bought it $1.37, sitting at $3.68 a year and a half later…and I got burned on that one…only was able to buy into 22% of the stock had allocated because too many people wanted it…still got 537 shares though)

Any thoughts on moving these to another account?

I have a question about investing in P2P loans in general. What are the chances that an individual investor will lose money? What are the risks? It seems like both of these considerations are probably different than investing in mutual funds. Is there any data on this or a good article explaining the pros and cons of investing in P2P loans?

I am hanging in there with my purchase and feel like it is a good sign with the market down 200 currently today (12/12/14) and LC holding in the mid 24’s…

I asked for 350 and got 250 as well. It’s difficult for me to evaluate LC’s prospects so my plan was to sell into an expected IPO pop. Got the allocation notice and quickly funded the account.

Scatterbrain that I am, I completely missed that I could sell the shares. Luckily I read MMB! Albeit a bit late – after market close. I set an alarm to be ready to sell today shortly after market open. As Lady Luck would have it, my tardiness earned another few percent – yay!

Not sure why so many comments here express concern about Fidelity blacklisting people for selling shortly after IPO. Is this a thing? What did I miss?

Part of the reason I didn’t sell…

Short-term capital gains do not benefit from any special tax rate – they are taxed at the same rate as your ordinary income. For 2014, ordinary tax rates range from 10 percent to 39.6 percent, depending on your total taxable income.

For 2014, the long-term capital gains tax rates are 0, 15, and 20 percent for most taxpayers

Jonathan, I’m equally confused and disappointed by your promotion of this (or any other) IPO.

When you educate your readers on the merits of index funds as the most efficient investment vehicle and a fully-diversified, buy-and-hold, “don’t try to beat the market because in the long run you can’t” strategy, I am a fellow disciple and in wholehearted agreement.

But when you feature your small investment and experimentation in LendingClub or other investment vehicles that are not true to the investing approach you usually endorse (and mostly follow), you undercut your far more important message and appear hypocritical.

The harmful role that emotion and greed play (read any John Bogle article, for more on this) for most investors is evident in the number and frothy, but misplaced, exuberance of so many of the comments to this post.

I’m a loyal reader and occasional commenter who has benefited from many ideas you’ve shared (Discover IT card, Mint.com, GEICO car insurance). But you do your readers a disservice by pouring blood into the shark tank as your LC posts have done. We’d be better served if–like John Bogle–you instead were to inform and educate on why stock picking and market timing are a fool’s game and how a patient, fully diversified investing strategy using low-cost index funds or ETFs is the only appropriate long-term choice for the frugal investor.

I’m not sure if people might be “better served”… perhaps, but this my blog and I think it works because I am human. Check out this WSJ article on “Funny Money” accounts:

http://www.wsj.com/news/articles/SB10001424052702304330904579137410675036086

No less than Burton Malkiel and (ahem) Jack Bogle admit to not 100% passive indexing:

I think I made it quite clear this was a small, speculative gamble. The Lending Club IPO was fun, educational, and my initial investment was under 0.25% of assets. 🙂

It’s also worth pointing out that participation was in a directed share program, not open trading. There’s a *huge* difference, Cooper’s Dad.

It’s worth spending some time reading up on how IPOs work, particularly how the principals try to build in some “pop” for the institutionals that pick up the shares in bulk at the IPO price, then flip them onto the open market for a quick gain. Participating in a directed share program allows individuals to particpate and benefit from that same “pop”.

Ironically, while I participated in Red Hat’s IPO via the directed share program, I worked for a company that got acquired by Red Hat not long after the IPO and I suddenly became a shareholder again and have been for the last 15 years.