LendingClub is supposed to provide me with an official response to my updated analysis of their loan performance numbers. Hopefully it will shed more light on how their advertised returns are calculated.

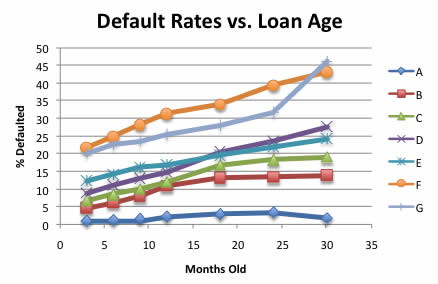

While I’m waiting for it, here is another chart I put together for prospective lenders using data from LendingClubStats.com, which pulls directly from LendingClub’s own statistics database. The full term for LC loans are 36 months (3 years). This chart organizes all loans by their age, allowing you to compare new loans and old loans on a more equal basis. Only officially defaulted loans are included, not late loans with payments up to 120 days late. The numbers are sorted by credit grades A through G.

I’ll let the numbers speak for themselves for now, and save my opinions for another time.

New Lender Incentives – Free $25 to $250 Bonus

If you are interested trying P2P lending with no risk, you can still use this special $25 lender sign-up link to get a free $25 to try it out with no future obligation. There is no credit check and you don’t even have to deposit anything. After you are approved, the $25 will show up in your account balance, and you can lend it out immediately.

If you’ve done your research and are willing to jump in with both feet, those that are willing to invest at least $2,500 at once and link a bank account can get a $100 bonus when you get a referral from an existing member. (Yes, you must actually invest $2,500 in loans.) Send me an e-mail if interested.

You can also view my personal LendingClub portfolio details here.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Their lack of follow-up on blogger questions/concerns is disturbing. I have sold all of my tradeable notes and am doing other things with the money while we all wait for some real answers. Great analysis… I’m tempted to call you ‘Fred93’ of LendingClub.

@F – They followed up, mostly to express their concern but I haven’t gotten any official response yet. (I haven’t checked my e-mail today while on the road.) I would also like some light shed, as I think it will help us all understand the process better. Meanwhile, this recent data makes me happy I’m mainly in A loans.

Fred93 had over $700,000 committed to Prosper loans. He had some REAL motivation to get on Prosper’s butt. 🙂 I’d be posting about LC every day if I had that kind of money committed!

I’m most interested to see how their notes from january 2009 forward end up performing in another year or so. If I remember right they shut down sometime in 2008 to do SEC filings and when they came back they had much more stringent requirements for obtaining a loan.

I’d also be interested to find out how successful their collections department has been. I’ve had a few loans default but never received a penny from collections. Has anyone had a loan default, go into collections and then received some of their money back?

I’ve got about $13k invested (been investing there since early 2008) but think I’m going to hold off putting any new money in until I see how things play out over time. Currently getting 9.4% and have 2 loans that have defaulted as well as 4 loans that are currently late and could default eventually.

Interesting. There has been a shift recently. I’m noticing a lot more less than stellar notes on offer and A category loans are harder to find. In addition, I just got my first late payment notice on one of my existing loans. It was a category C. Sticking with As from now on.

I am using both LC and Prosper at the moment… But I will not go below A or AA… After viewing the chart – it is probably a good decision. Thanks for the great info.

I don’t see how Prosper or Lending Club can run a viable business. I invested $1,000 with Prosper across about 15 different loans with an average interest rate of 12% in only the top two credit categories…and I won’t even break even because one loan defaulted.

I think LC/Prosper need to offer loans secured by something such as a car or home equity to get these default rates down.

I like my As thank you very much. 🙂

Mike –

I’m not sure your 15 loans are really enough to make any kind of blanket statements about the viability of prosper/lending club. With these sites I’d rather spread $1000 over 40 loans ($25/loans) so that one default doesn’t kill you. As with any investment diversifying is important. While I don’t think we’ll be seeing the 9.6% lending club currently advertises, I do think we’ll see rates higher than places like FNBO are offering now (1.25%). I also think we’re still in the middle of a huge recession with high unemployment numbers. I’d hope when the economy starts improving and jobless rates go down, we’ll start to see less and less defaulting.

Kevin –

Comparing these loans to savings accounts (FNBO, etc.) is not a useful comparison, the asset classes are too different. For starters, savings accounts are about as risk free as you can get (FDIC insured), and are completely liquid. I think a more apt comparison would be “junk” bonds, high yields, but with a real risk of default.

I had a loan go into default. It was that way for about 6 months then the status changed to “charge off”. So their advertised 2% default rate could be correct in the sense of how many active loans are in a default status as defined by them. Not defaultED past tesnse that an average person would think on.

I’ve had pretty good luck… I’m a small time investor on LC since I wasn’t sure how well the return rates would hold up long term. Out of my 8 loans, 3 are A-grade, 4 are B-grade and 1 is C-grade and none so far have been late or defaulted. I found that if you look at each note profile they will show you the borrower’s credit score over time – the C-grade borrower on my list shows a steadily declining credit score so I expect eventually they may default. At least they’ve paid for a year, so I won’t lose everything but I don’t think I’ll choose another C-grade loan in the future!

Tim –

I wasn’t trying to compare investing in lending club to investing in FNBO. They’re definitely different vehicles. I merely was making the point that I expect the return I’ll get on my 3 year investment in lending club notes to be better than if I had just kept the money in cash over the same period. Much in the way I expect my money invested in the stock market will give me better returns over 20 years than if I had just left it in cash.

Well, in all honesty… You seem to be quoting that LendingClubStats.com “pulls directly from LendingClub’s own statistics database”, but that doesn’t seem to be the case as noted in their disclaimer (below).

“Disclaimer: LendingClubStats.com is not in any way affiliated with LendingClub.com. Comments posted on this site are the opinions of the individuals who post them and this site is in no way responsible for the content of these comments. While we try hard to make sure the data shown on this site is up to date and accurate, it is not real time and may contain inaccuracies.”

Bottom line, it may be right and it may not be… Who knows…

Oops… Submitted too early…

Another thing this doesn’t seem to take into account is the “Due Diligence” process.

Nice work!

One question, how is it that the default rate for A Loans when down during the age of 24-30 months? I would have assumed that the default percentage is cummualtive, no?

@Aggie LC allows you to download stats without being affilated with them.

I’ve been a member since February 2009 (started with 1K now I have 12K, all $25 and $50 notes). I can tell you right off the bat that Lending Clubs default stats are grossly under actual rates. I only invest in A, B, C and sometimes D (mostly B) and never invest in start-ups or medical expense related applications. Theoretically I should be around 12% assuming no defaults. However, I’m at 6% and very unhappy I’ve had my money tied up in Lending Club for this long to get what amounts to a Muni bond interest rate.

The interest rates they offer are way way too low. There’s a reason other than greed for banks charging 18%+ for credit cards. The world is full of dead beats.

I’d stick with A loans and expect a 6%-7% return.

I invested in 40 $25 notes 6 months ago (A,B,C). 2 are on the way to default, leaving my rate of return around zero.

I won’t re-invest. Too many deadbeats out there. I’m glad these people will enjoy their new “house remodel project”, and “debt payoff” at my expense.

These are unsecured debts with mild consequences for the delinquent borrower. Nothing lending club can do to them except call them. Maybe if there were some collateral involved, or some public accountability and consequences involved for the defaulted, I would reconsider further investment. Until then, I’m out.

Currently 4.4% of my loans have already been charged off. Another 3.1% are 30-120 days late or already in default. Its very rare for a loan this late to not eventually default. I have a mix of notes, with mostly B rated loans. I have been with LC for two years.

Basically, double or triple LC’s posted default rates to approximate reality.

My ‘return’ has dropped steadily since day one. I’m currently at 7.5% which I suppose I should be thankful for. But how low will it eventually go?

It’s important to remember that default rates don’t directly tell you your return. You could theoretically have a 100% default rate on the loans you made and still make a lot of money (if they all defaulted on month 35, for example). So a 40% default rate might sound scary, but it doesn’t mean you still wouldn’t make good money from such loans.