I’ve written a little bit in the past about including small-value stocks to your investment portfolio. “Small” means companies with a relatively smaller market cap (total market value) – definitions vary from being the bottom 10% by capitalization or being worth less than $1 billion. “Value” stocks are those that tend to trade at a lower price relative to others when measured against markers like earnings, dividend yield, sales, or book value.

This NYTimes article on the portfolio of investment advisor and author Larry Swedroe included some concise examples of how significant this small-value premium has been in the past. For one, small-value stocks outperformed the S&P 500 by about 4% annually from 1927-2010.

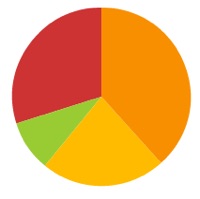

Put another way, by making a portfolio using small-value stocks and US Treasury bonds, you could have gotten similar performance to the S&P 500 with much lower risk. Specifically, you could have held 1/3rd small-value and 2/3rd Treasury bonds and had close to the same return as the S&P 500 over a 40-year period from 1970-2010. This chart summarizes:

Source: Buckingham Asset Management, New York Times

Will this “small-value premium” continue to persist? There are a few theories out there. One is behavioral, where small-value companies tend to be the more ignored and unpopular companies and thus are consistently underpriced. Another is based on the fact that small-value companies are simply riskier, and thus investors demand a higher return for holding them.

I happen to believe that there is something enduring about small-value stocks, but the size of my bet on that belief is relatively small – only about 5% of my target stock allocation. But I also know that you need to hold a very strong belief in whatever internal explanation you have for the outperformance. Otherwise, when small-value is the dumps for a while relative to the Current Hot Thing – and it will be, one day – you’ll sell and lose any potential edge.

(

(

Interest rates remain very low, which makes people more willing to take some risk for “just a little bit higher” interest rates. This has renewed interest in the financing arms of many automotive brands that offer “demand notes” which they use to fund the loans and leases they need to make to sell cars. (Can you imagine how much fewer new cars would be sold without financing?)

Interest rates remain very low, which makes people more willing to take some risk for “just a little bit higher” interest rates. This has renewed interest in the financing arms of many automotive brands that offer “demand notes” which they use to fund the loans and leases they need to make to sell cars. (Can you imagine how much fewer new cars would be sold without financing?) In my

In my

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)