One of the recurring themes of personal finance is that while the concepts are often simple, execution can be quite difficult. A couple of excellent posts from Mr. Money Mustache and The Military Guide (both also mention the Early Retirement Extreme book) provide another example when answering the question “How many years until I can retire?”

Let me summarize. A simple definition of financial independence is creating enough income from your investments to pay for your expenses. Assuming a “safe” withdrawal rate of 4%, this means your portfolio must be 25 times your expenses. So if you spend $30,000 a year, you’ll need $750,000. (If you want “safer” withdrawal rate of 3%, that increases it 33 times expenses.)

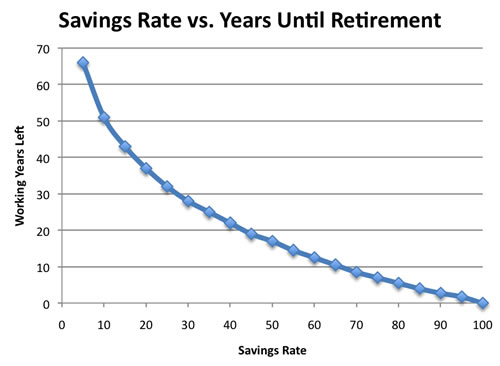

Given the rough assumptions of starting with nothing and earning a 5% inflation-adjusted (real) return on investments every year, you can simplify things even further. (5% real return looks plausible based on the past, but I know it’s harder to see it now.) It works out that the only thing that matters is your personal savings rate:

After-tax numbers work better since expenses are usually after-tax. MMM provides a table, which I in turn converted into a single curve:

Notes:

- The harsh truth is that if you want to retire before Social Security steps in, you’re going to have to save a lot more than 10%.

- The curve is steepest at lower savings rates. That means increasing your savings rate from 10% to 20% shaves off more time working (14 years!!!) than increasing from 20% to 30% (still 8 years!), and so on.

- Retiring in 20 years requires roughly a 40% saving rate. Retiring in 10 years requires a 65% savings rate.

If you’re new to the financial independence community, the idea of saving 40% or more of your income may be incomprehensible. Hopefully you will realize that it is possible, if you wish to pursue it. I have come to the conclusion that some people will happily work for 30 years in exchange for the ability to drive a new BMW every 3 years. Others (gasp!) just like their jobs that much. All that’s fine as long as that’s a conscious decision.

To increase your saving rate, you must either increase income or decrease expenses. While decreasing expenses is actually the more accessible option for most families, it will likely remain unpopular forever. That doesn’t mean you can’t do it, because many people are quietly doing exactly that. Try – you may surprise yourself.

I am also a strong proponent of increasing income. In the end, in our household we did a combination. Both of us earn an solid income after a combination of tuition-based postgraduate education and “DIY education”, but we only live on the lower income. Armed with a 60%+ saving rate, we are on track to achieve financial freedom according to this definition within another 5 years, although we may take a different path by working part-time for a longer period.

I must admit, even though I have known this “truth” for many years, I don’t actively talk about it because we do earn much higher incomes than average. However, that doesn’t change how the numbers work. I applaud all those bloggers and journalists that don’t patronize you and push the idea of higher savings rates, like this article in The Atlantic by Megan McArdle:

If you’re like, well, almost everybody, you’re not saving enough. 15% of each paycheck into the 401(k) is the bare minimum you can get away with, not some aspirational level you can maybe hope to hit someday when you don’t have all these problems.

I mean, obviously if one out of two workers in your household just lost their job, or has been stricken with some horrid cancer requiring all sorts of ancillary expenses, then it’s okay to cut back on the retirement savings for a bit. But let’s be honest: that doesn’t describe most of us in those years when we don’t save enough.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I just bumped up my contribution level from 10 to 11 percent. I didn’t get a raise but we changed health care plans to a less costly option which reduced our out-of-pocket costs, so I applied a portion of that to retirement. Every raise will see me add another 1 percent. I’d been planning on being further along but the last three years have seen no raises which has been frustrating to say the least!

I might be missing something but there seems to be many caveats to using this approach. First,if you are using gross income as “current income” then “current spending” would have to include all taxes as well for savings%+spending%=1. This is a false assumption for what you need for retirement since you dont pay Soc Sec and your retirement tax rates are totally diff since you’re usually in a lower bracket. If current income is after tax, then the savings rate is misleading as well since now its a post tax percent while all of the 401k contributions as done as a percent of gross.

Secondly, I dont see where what you currently have saved is part of this equation though maybe the assumption is always this is a starting value so not sure how this works for mid-career folks. Wade Pfau has some charts that take into account savings so far if you google “Getting on track for a sustainable retirement.”

Also, the 4% has a lot of fine print to it (and it mostly meant for a 30 yr retirement; 3% was for a 40 yr retirement so early retirees have risk in either), but that is a well worn issue. Though I dont know where that assumption part fits in the large print equation shown.

This may be a useful rule of thumb to start, but you will have to more number crunching to make sure your target is really in sight.

I agree–boosting income through creative means is often an overlooked piece of the saving puzzle. Even a little bit will make a big difference over many years.

A broader point though: I think the word ‘retirement’ needs to be retired. I’ve transitioned from high-pressure, time-demanding ‘career’ jobs to part-time work for nonprofits with a mission I care about. Sure, the hourly pay is less, but the work is still challenging and rewarding. I earn some money (avoiding that uneasy feeling the goes along with relying solely on drawing down one’s nest egg), I have the opportunity to keep learning and building a network, and help to improve my community (I hope!). I plan to continue like this as long as I’m physically and mentally able. When people ask if I’m retired, I don’t quite know how to answer. It doesn’t feel that way!

To me, the era of retirement–meaning engaging in no paid employment–is over, and that’s a good thing. Paid work doing something challenging and that you care about has many important benefits, of which stretching your nest egg may actually be the least important with respect to happiness.

That Atlantic article is fantastic.

One interesting point is how much income is often downplayed by more “frugal” types. I always liken personal finance to dieting. Sure, you can do great with the dieting, but exercising makes it a WHOLE lot easier to lose weight. One or the other is not more important. I believe in increasing income AND cutting expenses. Which is something I am thankful my parents really talked to me about when choosing a career. (I ended up with what I liked the best but that paid the most money). Ironically, this is also a perk to living in California. We have spent a lot of effort whittling down our mortgage, but by doing so have elminated the expensive part of living here. But the jobs still pay well, whether you have a giant mortgage or rent payment, or a paid off home.

Anyway, the general financial advice to save 15% retirement or 20% as a whole, never struck me as very ambitious. Before kids we both worked and banked one income. My dad has had trouble finding work since about age 50, though he’d be happy to work forever. But, he’s been saving half his (very large) paycheck for many years. Expenses low, income high = win-win.

Good points and it’s nice to see some acknowledgement that just saving the minimum is not a complete answer. I save at about 35% right now, and mostly worry about putting cash to work when it can’t go into my 401k or IRA. It’s hard to complain about such a ‘problem’, but it’s not really easy either.

“I mean, obviously if one out of two workers in your household just lost their job, or has been stricken with some horrid cancer requiring all sorts of ancillary expenses, then it’s okay to cut back on the retirement savings for a bit. ”

For what it’s worth, getting stricken with some horrid cancer generally implies that one of two workers in your household just stopped working. Possibly both of two workers.

Just in case that changes anybody’s financial plan at all.

For all the talk on this subject, the bottom line is that you need have at least $1.5 million in savings, a way to deal with the avarice US healthcare industry and no debt and preferable no children. There, that’s the whole thing. Anything else…..well….you’re the slave you’ve always been.

There are a number of ways to accumulate the necessary funds: insider trading, corrupt politician, head of a union, lobbyist, war criminal and write a book about it, TV talking head, among others. America still offers many options to achieve your goals.

The big Johnathan is the returns part, I have found that the returns are getting lower and lower with time so that is the hard part. What is the avg returns you are seeing over the last few years. How are you making that 65% work for you? What is your strategy for putting every dollar saved to work.

I was sad to see Jacob from Early Retirement Extreme hang it up and return to the workforce! Because he was one of the few who were living the early retirement lifestyle and made it seem achievable (if not a stretch for the rest of us). But I’ve always liked the idea (if possible) of saving 50% of your after tax income. If you are able, for every year you work, you buy a year off… not factoring for interest!

@Kurt: totally agree with you. Before starting to read these comments that same thought popped up in my head, that “retirement” is undefined here. If you are happy with what you do, what is “retirement” for you, not doing what you like anymore?

I’m a little late on checking my referring links but yep, Jacob’s ERE was the inspiration for The-Military-Guide.com’s savings chart. After that all I had to do was spend a couple hours crunching numbers and formatting HTML tables…

From a military perspective, the 10-20 years is right in the sweet spot for someone who chooses to leave the service after a couple of service obligations– or someone who stays on active duty until they qualify for a military pension.

A military inflation-fighting pension (and cheap healthcare) makes the process much easier. But note that gutting it out to a military retirement is not necessary. Cutting back to part time or saving all of a spouse’s income will also greatly accelerate the progress.

Not sure how accurate this chart can be. I’m 25 and between retirement and cash savings I’m at about 44.5% after taxes. According to the chart, I’d have less than 20 years left, however I’m not so sure that’s even close. I’ll probably be stuck working well into my 60s.

The charts are derived from the Trinity Study math of accumulating 25x your expenses, and that 25x number is also the result of the future value of a series of payments. Instead of this graph, I lay out the math and a couple of charts at http://the-military-guide.com/2011/01/03/how-many-years-does-it-take-to-become-financially-independent-2/ .

It’s counter-intuitive because initially your savings rate is more significant, and the exponential compounding of the investment returns seems to take a long time to kick in. It works very fast if you can achieve Jason-like savings of 80% of your income. If you save 40-50% of your income then it takes closer to that 20-year number. Around year 18-19 your investment portfolio will start making almost as much money as you do.

You can also check how you would have done against 100+ years of investment returns at FIRECalc.com.

If you enjoy what you’re doing then I’d never retire, either. But if work gets in the way of family and quality of life and all the other things you want to do outside of the corporate environment, then financial independence is a great starting point for making choices on what else you’d like to do!

I found this very interesting. I wonder if anyone else derived the equation for the curve. I came up with this: N = Log b (-1/(P/A*(i – 1)) , where the base (b) is (1+i). It’s a solution based on the general annuity equation P = A*( (1+i)^N-1)/(I * (1+i)^N). For I = .05, the curve fit equation is N = -20.5 ln(Savings Rate %) + 3E-14 (R^2 = 1)

P.S. I’m not a financial expert, just an old engineer