An article on the Vanguard Advisors Blog discussed the trade-offs involved in adjusting an investor’s savings rate and the risk level of their portfolio – Investor success: Measured in dollars, not (per)cents.

A portfolio’s value can grow through both capital contributions and return on capital, but only capital contributions can grow wealth reliably. Saving is our contribution to our own investment success and, importantly, unlike the investment returns we seek, its benefits are both more certain and within our control.

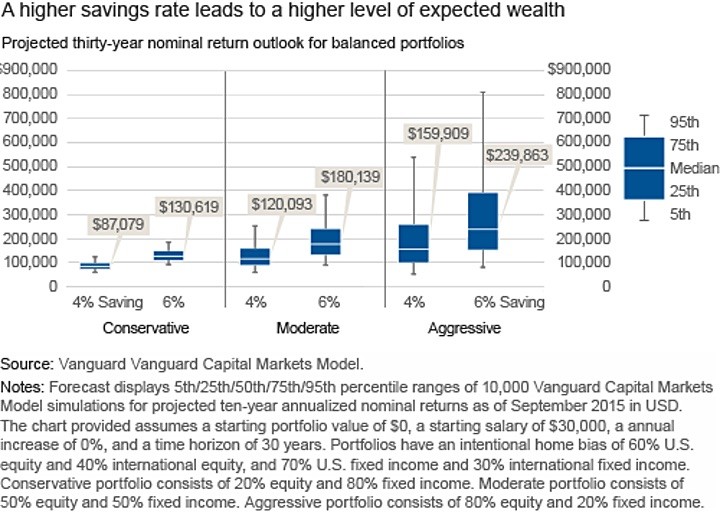

The chart below shows projected outcomes based on savings rate (4% or 6%) and portfolio risk level (conservative, moderate, or aggressive). You can see visually that the combination of 6% savings rate and moderate risk (50% stocks/50% bonds) has both a higher average outcome and fewer poor outcomes than the combination of 4% savings rate and aggressive risk (80% stocks/20% bonds)

Part of this should be expected – you’re saving 50% more in dollars when going from a 4% to 6% savings rate. But on an absolute level, perhaps that amount of dollars is something you can swing.

Vanguard did a similar study called Penny saved, Penny earned back in 2011 that compared three levers: savings rate, portfolio asset allocation, and also starting to save earlier. Take the following baseline scenario:

- Investor begins working at 25, but starts saving at age 35.

- 12% savings rate

- Moderate asset allocation (50% stocks and 50% bonds)

- Salary starts at $30,000 but increases with age

Now, here are three ways in which a worker could increase their final savings balance at retirement (age 65).

- Option #1. Invest more aggressively with an asset allocation of 80% stocks and 20% bonds, while keeping your 12% savings rate and starting age of 35.

- Option #2. Raise your savings rate to 15%, while keeping your starting age of 35 and 50/50 asset allocation.

- Option #3. Start saving at age 25 instead of 35. while keeping your 12% savings rate and and 50/50 asset allocation.

Which single option do you think has the most impact? The results are based the median balance found after running Monte Carlo computer simulations based on 10,000 possible future scenarios for each option.

| Scenario | Median Balance at age 65 | % Increase vs. Baseline |

| Baseline | $474,461 | – |

| Option #1 (Aggressive asset allocation) |

$577,133 | 22% |

| Option #2 (Raise savings rate) |

$593,077 | 25% |

| Option #3 (Start saving earlier) |

$718,437 | 51% |

Between the three “levers” you could pull, starting to save earlier wins by a significant margin, which is an important truth but minus a time machine today is the earliest we can start saving more. After that, a higher savings rate is a more reliable path to improving your odds for success. Investing with significantly more risk performs somewhat similarly on a median basis, but actual results will vary the most widely.

I suppose my version of this is that an investor should keep working hard to maximize their savings rate, but only work hard to find a “good” asset allocation once and then let it be. My definition of “good” asset allocation is one that considers your financial needs, your knowledge, and as a result is something that you can keep forever. Don’t look for the “perfect” asset allocation, as these can only be known after the fact and are constantly changing. Too often, they are based on data mining and recent performance. Look at any asset allocation with growing popularity, and the asset classes that make it hot have probably done well in the past decade. You can quote “long-term” numbers from long periods like 1970 to 2015, but these numbers are still strongly influenced by recent past performance.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I like this post a lot. I hadn’t seen those studies before, but they provide a helpful visual so people can understand the concepts. I think far too many people are concerned with finding the best performing asset allocation. However, their portfolio’s performance would benefit the most from a higher savings rate or just getting the ball rolling now. As far as investments go, time is your friend.

This reminds me of the “locus of control” psychology theory. Those who have an internal locus of control and focus on the things they can affect and change tend to do better in life than those who focus on the things they can’t control. Everyone can control their savings rate and take action to increase it. However, stock market returns are generally out of any individuals control. By focusing on your savings rate and letting the market do it’s thing, I believe you’ll have more financial peace. See Mr. Money Mustache’s article on this topic here: http://www.mrmoneymustache.com/2013/10/07/how-big-is-your-circle-of-control/

Also, Go Curry Cracker has an excellent post comparing a 25%, 50%, and 75% savings rate. Clearly the 75% savings rate destroys all the others, but it’s pretty amazing how quickly you can become financial independent, even with an uncooperative stock market:

http://www.gocurrycracker.com/financial-independence-how-long-will-it-take/

Check it out!

https://www.gsbank.com/savings-products/online-savings.html?prod=SAV