Consumer Reports (CR) has released a multi-part Special Report on Auto Insurance, included in their September 2015 print issue but also available online without a subscription (at least for now). They analyzed over 2 billion quotes from over 700 companies across 33,419 zip codes. Here are some highlights of what they found.

Consumer Reports (CR) has released a multi-part Special Report on Auto Insurance, included in their September 2015 print issue but also available online without a subscription (at least for now). They analyzed over 2 billion quotes from over 700 companies across 33,419 zip codes. Here are some highlights of what they found.

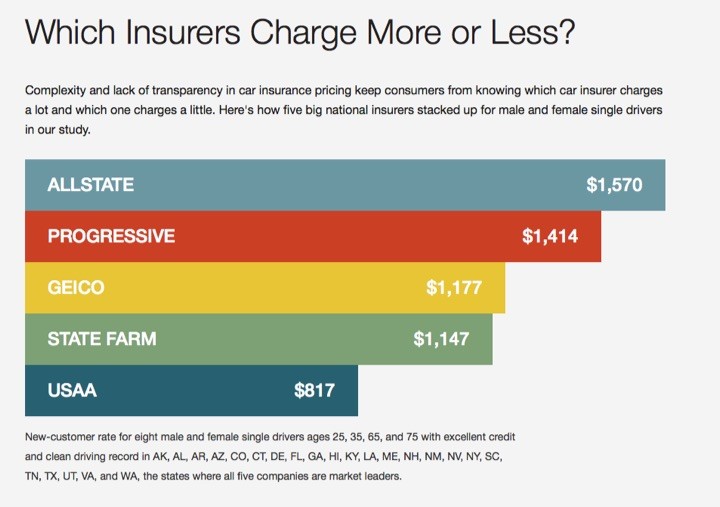

First, here’s a big picture view of which major car insurers are more expensive on average.

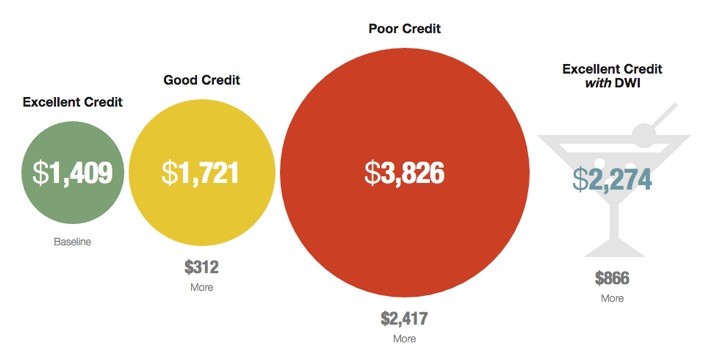

The biggest individual factor in your premium may be your credit score. Clicking on your state on this 50-state interactive map will give you an idea of the effect of having a “poor” or merely “good” credit score as opposed to an “excellent” one. California, Hawaii, and Massachusetts are the only states that prohibit insurers from using credit scores to set prices.

Often, having a poor credit score with clean driving record is more expensive than having an excellent credit with a DUI/DWI! Here’s a screenshot for Florida:

Another important factor is your loyalty and tendency to comparison shop other items like cable TV. You often think “Loyalty Discount”, but often there is a “Loyalty Penalty”. If you don’t shop your auto insurance, some companies don’t see something to be rewarded; they see a sucker. In my limited experience, the companies with the lowest quotes to entice you from another company are also the ones to hike up the rates every year afterward. Here’s what CR found:

Geico Casualty gave us whiplash with its $3,267 loyalty penalty in New Jersey and its $888 discount just across the state line in New York for longtime customers. State Farm Mutual consistently provided discounts of a couple of dollars up to a few hundred dollars; Allstate Fire and Casualty and Allstate Property & Casualty tended to prefer penalties.

As noted in a previous post, Big Data knows if you’re comparison shopping or not. Such “price optimization” occurs when they find out you could have saved money somewhere else like broadband internet, but didn’t. Not a price-sensitive shopper? You may get the higher rates. Even states that officially ban the practice don’t really have any foolproof way to know if it’s happening. Here’s what CR found:

Amica Mutual and State Farm told us they don’t use price optimization. Representatives from Allstate, Geico, Progressive, and USAA declined to discuss price optimization.

Here’s the general conclusion:

What we found is that behind the rate quotes is a pricing process that judges you less on driving habits and increasingly on socioeconomic factors. These include your credit history, whether you use department-store or bank credit cards, and even your TV provider. Those measures are then used in confidential and often confounding scoring algorithms.

What can a consumer do about all this? Consumer Reports wants you to write to your state’s insurance commissioner, and they have a petition template ready for you. David Merkel of The Aleph Blog says you should simply fight back the market-based way: comparison shop your personal insurance lines every 3 years.

Bid it out. Bid it out. Bid it out. What do you have to lose? If loyalty means something to the insurer, they will likely win the bid. If it doesn’t, they will likely lose. Either way you will win. If you have an agent, they will note that you are price-sensitive. The agent will become more of an ally, even if it doesn’t seem that way.

[…] You don’t need transparency, or more regulation. You don’t get transparency in the pricing of many items. You do need to bid out your business every now and then. You are your own best defender in matters like this. Take your opportunity and bid out your policies.

I tend to agree with Mr. Merkel. However, I am still a long-time customer with State Farm. I’m happy to see that State Farm was found to consistently providing loyalty discounts and claims not to engage in price optimization. I shopped around for auto quotes in 2013 and GEICO was cheaper by about $372 a year. However, I had to balance that with the knowledge that GEICO will probably hike my premiums every year and also I’ve had excellent claim service from State Farm. Perhaps it is time for another comparison shop.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I agree that it’s a good idea to consider other points besides the bottom line premium quote, particularly claims service. When I’ve shopped around for insurance in the past I’ve looked at ratings of claims service from Consumer Reports and JD Power. Based on those ratings I didn’t even request quotes from several companies. I look for at least average ratings for auto insurance and above-average for homeowners insurance.

Does anyone else know of good sources for insurance claim service ratings? It’s nearing time for me to shop around for new quotes.

I’m sure I will be the first of many to sing the praises of USAA in the comments, but the one thing the above Consumer Reports numbers appear to NOT capture for USAA are the annual insurance premium rebates.

As USAA is a member-owned company, USAA rebates excess premiums paid annually. I’ve found that the amount USAA rebates as to my auto insurance premium is approximately 10% of my annual premium. Add that onto the top of the above spread in rates, and USAA becomes even more competitive. I have found however that USAA is generally not competitive on things such as auto loans, mortgages, or credit card rewards – for those things I shop around and have found similar-eligibility credit unions (such as Navy Federal for auto loans/mortgages) to be way more competitive.

Although I do miss the rebates, they don’t tend to help that much. I thought the price looked off, but to make sure, I called. USAA is $800/year (2 vehicles) more expensive than GEICO for me. I like USAA, but not enough to pay the extra $$$. It looks like they need a bigger sample size, because 16 quotes may not be representative enough.

We comparo shop on home insurance and auto insurance every year. USAA has us for now on our home – price gap was $800 for the same coverages. Auto insurance, Wawanesa has devoured the competition for 15 years. Nobody has been able to get close on them. Our Farmers’ agent (for rental properties) asks every year, runs the numbers and can’t come close on our main home or cars. You’d think bundling would help but it doesn’t with USAA, etc.

As your life situation changes you may start to consider how you think of your auto insurance from ‘that thing i must have’ to ‘something that really protects/serves me’. Most insurance will quote you a standard plan based on coverage limits and deductibles but you may be better served getting a quote that is more full featured to help you when bad happens.

For instance, you have two car seats in a minivan. Will your daily rental limits allow for a similar vehicle to get your family to/from daycare, or will the $25/day limit only allow for a compact car? Do you want to personally cover the additional $25/day for each day it is being repaired or negotiating the total loss & repurchase to upgrade to the minivan? Or, should your insurance truly cover your needs and therefore get quotes on that level of coverage? At this point in my life, I’m going for the latter.

When you started out with “something that really protects/serves me” I thought you were going to mention how the absolute downside could be millions of dollars in hospital bills you’re responsible for if an accident is your fault. Instead you mention the ticky tack 25$ per day fee you could be on the hook for. While I’m not saying you should ignore that, I don’t really need insurance for an amount that small, I need it for that crazy event that could ruin my finances.

Car insurance is ESPECIALLY dependent on where you live, which is something that this post doesn’t really cover. I realize the report is meant to reach a broad audience by publishing data for a very large geographical reason. for background, let me start by saying I am in Utah.

For my home insurance, I use Amica based on their stellar claims reviews and great service. In the event of a large disaster (I wouldn’t make a home insurance claim otherwise), I don’t want to deal with the haggles of a hesitating insurance company. However, their car insurance quotes for me were over $1500 more per year than Geico (2 inexpensive sedans, 2 drivers 20-30). When I told the agent that I paid less than $500 annually for GREAT coverage with Heidi, they didn’t believe me. I even emailed them a copy of my bill.

For my particular case, I have alternated between esurance and Geico although I get quotes from all the big carriers once every 18 months or so. They cannot come to within $300 of my current quotes. Locally, Bear River Mutual in Utah also provides competitive rates as well.

In closing, just wanted to emphasize that where you live also has a large factor on your rates.

This is only a rough guide – you need to shop.

for example this chart says geico is cheaper than progressive but I live in florida and for my good credit score,

progressive charges me half of what geico used to

If you bundle car, home and umbrella insurance would you still comparison shop knowing that home insurance is difficult to obtain?

Why is home insurance tough to get? Never had an issue.

Hey, thanks for the mention… and glad I could be helpful to you.