Updated 2019 with more websites. “People would care more about privacy if they knew how exposed they already are online,” says Geoffrey A. Fowler in his WSJ article Your Data Is Way More Exposed Than You Realize.

I hear this all the time: “I have nothing to hide.” The truth is, pretty much everybody does something online they have reason to keep private.

I would have to agree. These days, it just takes a few clicks to find out your age, current and past addresses, phone numbers, and the names of your parents, siblings, children, cousins, and in-laws (and thus all of their information). Try entering your own name and city into one of the first few websites on this list:

- Peoplefinders.com – Public access to your current and past addresses, phone numbers, relatives and associates. Opt out at www.peoplefinders.com/manage.

- InstantCheckMate.com – Public access to your current and past addresses, phone numbers, relatives and associates. Opt out at www.instantcheckmate.com/opt-out.

- FamilyTreeNow.com – Public access to your current and past addresses, phone numbers, relatives and associates. Opt out at www.familytreenow.com/optout.

- TruePeopleSearch.com – Public access to your current and past addresses, phone numbers, relatives and associates. Opt out at www.truepeoplesearch.com/removal.

- MyHeritage.com – Must e-mail them at privacy@myheritage.com to remove information.

- Geni.com – Must e-mail them at privacy@geni.com to opt out.

- Spokeo.com – Public/paid access to birth month, email, current and past addresses, phone numbers, relatives, social networks and court records. Opt out at spokeo.com/optout.

- Acxiom is a data broker that uses information to target ads and marketing. I found some unique data on there, although supposedly it’s not public (just up for sale). Opt out at acxiom.com/optout.

Opt out. For most of these websites, there is an opt-out option hidden in either their “Terms & Conditions” or “Privacy Policy” pages. Even though many of these sites appears to be clones of each other, you must opt out of each of them individually. The only “good” news is that where available, my opt out requests were fulfilled and I can’t find those records even a year later. It’s like stomping a cockroach but knowing there are more that you just can’t see.

Here are some related resources:

Facebook and Google serve as bottomless vacuums of your personal data. These tools help show you exactly what they keep.

- StalkScan.com – Not public. Just links to specific parts of your own Facebook profile. Find out everything that Facebook stores about you, even if it’s hard to find otherwise.

- Google Maps Timeline – Google may be tracking your location all day long and keeping records forever. Not public. You can log in and request your data to be deleted.

- Google My Activity – Google may be tracking every search and your web browsing history and keeping records. Not public. You can log in and request your data to be deleted.

Free Consumer Reports. You can also get a copy of your data stored at official consumer reporting agencies via the Fair Credit Reporting Act (FCRA).

If you have researched retirement at all (early or otherwise), you’ve probably ran across various retirement calculators online. You input how much money you have (or plan to have), your asset allocation, and it spits out some numbers. This

If you have researched retirement at all (early or otherwise), you’ve probably ran across various retirement calculators online. You input how much money you have (or plan to have), your asset allocation, and it spits out some numbers. This

Thinking about 529 plans and like playing around with interactive calculators? This

Thinking about 529 plans and like playing around with interactive calculators? This

There are some (mostly young) skeptics, but Social Security should remain a major pillar of your future retirement income. For over 60% of current retirees aged 65+,

There are some (mostly young) skeptics, but Social Security should remain a major pillar of your future retirement income. For over 60% of current retirees aged 65+,

Thinking about moving your cash to a different bank account with a higher interest rate? It’s been a while, but the short-term rates on

Thinking about moving your cash to a different bank account with a higher interest rate? It’s been a while, but the short-term rates on

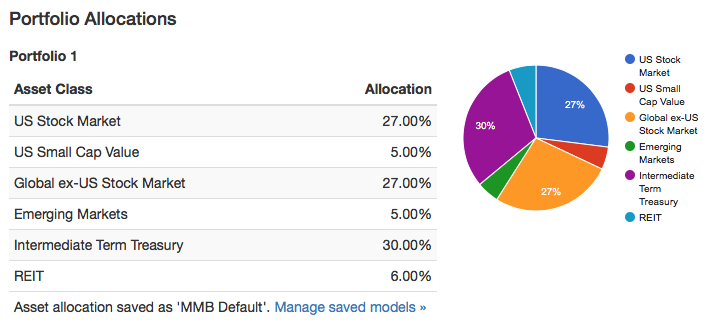

Here’s another neat (and free!) portfolio analysis tool –

Here’s another neat (and free!) portfolio analysis tool –

I just noticed that PortfolioCharts.com has updated their

I just noticed that PortfolioCharts.com has updated their

Updated. Automated portfolio management services like

Updated. Automated portfolio management services like

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)