Updated for 2022. This year, the deadline for federal tax filing is Monday, April 18th, 2022. If you file for an extension before midnight on that date passes, you can extend the time allowed to file your return by six months to October 17, 2022. It does not extend the time to pay any tax due. There are many legitimate reasons to ask for such an extension, and the extension is granted automatically without needing to provide a specific reason.

Updated for 2022. This year, the deadline for federal tax filing is Monday, April 18th, 2022. If you file for an extension before midnight on that date passes, you can extend the time allowed to file your return by six months to October 17, 2022. It does not extend the time to pay any tax due. There are many legitimate reasons to ask for such an extension, and the extension is granted automatically without needing to provide a specific reason.

The Failure to File Penalty is 5% of the unpaid taxes for each month (or part of the month) that the tax return is late (without extension). The Failure to Pay penalty is 90% less: 0.5% of your balance due for each month (or part of a month).

In addition, you can instantly e-file a federal and state tax extension (where available) for free. Advantages of using e-File include:

- You save the time and postage costs of paper mailings.

- You can estimate your tax liability using online software and/or calculators.

- You receive confirmation of receipt via e-mail or text, often within hours.

- The potential convenience of filing your state tax extension online at the same time.

TaxACT

This is how I usually do my extension because they include state as well. Tax prep software TaxACT.com allows you to e-File your Federal and State extension (where applicable) for free through them. You don’t need to actually use them to file your taxes later, although you certainly can.

This is how I usually do my extension because they include state as well. Tax prep software TaxACT.com allows you to e-File your Federal and State extension (where applicable) for free through them. You don’t need to actually use them to file your taxes later, although you certainly can.

Directions

First, register for free at TaxACT.com with your e-mail address and pick a password if you haven’t previously. Next, if you wish to perform a state tax extension, you must go to the “State” menu option on the left and add the appropriate state tax return. You don’t need to fill it out, just add it so they know what state you are filing for. If asked, just pick the “File Free” option, you shouldn’t need to enter any payment information. Some states don’t even require a separate filing, but TaxAct supports the electronic filing of extension forms for the following states:

- Arizona

- California

- District of Columbia

- Kentucky

- Louisiana

- Maryland

- Massachusetts

- New Jersey

- North Carolina

- Pennsylvania

- Tennessee

- Texas

To go directly to the extension form, click on the “Filing” tab on the left menu, and then the “File Extension” link right below it. You will be able to choose whether to file extension for Federal, State, or both. You will then be guided through the Form 4868 in a question-and-answer format. TaxACT will file the form electronically for you (or you can print and snail mail).

TaxACT also provides a tax liability estimator to help you determine if you need to make a payment with your extension. If you fill out more details in the main software, then the estimate will be improved. If you don’t think you’ll owe any taxes, you can just put down zero as your expected tax liability. If you wish to make a tax payment, you will be able to choose to pay with direct withdrawal from a bank account (account and routing numbers required) or pay with a credit card (IRS fees apply).

Afterward, you can confirm the status of your extension e-file by going to efstatus.taxact.com. They will even send you a confirmation via e-mail or text message. I got my confirmation less than 3 hours after submission.

TurboTax

TurboTax.com also allows you to file a Federal extension online for free after signing up for a free account. They are rather vague on state tax extensions, stating that they will only show the state extension option where available after you have completed the majority of your state return. (Doesn’t this kind of defeat the purpose?) After logging in, look for the big search box on the top right and type in the keyword “extend” to be directed to their extension section.

It will walk you through the information needed for Form 4868. Again, if you don’t think you’ll owe any taxes, you can just put down zero as your expected tax liability. If you wish to make a tax payment, you will be able to choose to pay with direct withdrawal from a bank account (account and routing numbers required) or pay with a credit card (IRS fees apply). The site states that you’ll get a confirmation from TurboTax within 48 hours.

H&R Block

The option to e-file in H&R Block is little hidden, and they say “A deposit may be required.” But if you already plan to use H&R Block, here’s how to find it. You must go to the dashboard/main filing page and look for this small link in the bottom right corner:

Free File Fillable Forms

As the name suggests, FreeFileFillableForms.com is another privately-run site (actually owned by Intuit, not the IRS) that allows you to fill out Federal IRS forms online, for free. They are basically the exact same paper forms that the IRS would provide you, with no additional guidance or assistance. State tax extensions are not included.

As the name suggests, FreeFileFillableForms.com is another privately-run site (actually owned by Intuit, not the IRS) that allows you to fill out Federal IRS forms online, for free. They are basically the exact same paper forms that the IRS would provide you, with no additional guidance or assistance. State tax extensions are not included.

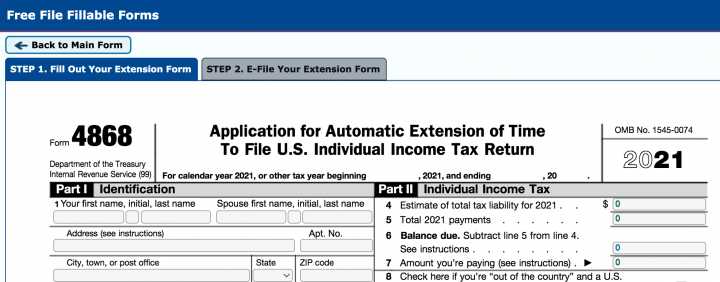

For some reason, they make you create a new account every year. After you’re signed in, on the top left of Form 1040 you should see an icon with the label “File an Extension”.

This will bring up Form 4868. Click around the form to fill the boxes out. As above, you’ll need to estimate your total tax liability, but since this is just an online version of the form so there is no guidance included. You can request your estimated tax payment to be withdrawn electronically by supplying your bank’s routing and account numbers. For identification purposes, you’ll need your adjusted gross income (AGI) from your previous year tax return.

Bottom line. There are many options to e-file your tax extension for free. Confirmation is usually provided within 48 hours, as opposed to having to worry about if your paper form got snail-mailed to the IRS successfully. Filing an extension only extends the time to file your return and does not extend the time to pay any tax due. To avoid late payment penalties and interest you must estimate what tax will be due and pay that when you file the extension. However, the penalty for late filing is many times higher than the penalty for late payment. If you are not 100% sure you can file in time, file for an extension.

As we head into the last few months of 2021, this is a reminder to check on your Healthcare and Dependent Care Flexible Spending Accounts (FSA). This

As we head into the last few months of 2021, this is a reminder to check on your Healthcare and Dependent Care Flexible Spending Accounts (FSA). This

The

The

It might be a little painful, but it may be worthwhile to check on your pre-tax IRAs during this dip. If you have been thinking of converting your “Traditional” IRAs over to Roth IRAs, your shrunken gains will lead to a smaller tax bill now, while your (hopefully) future gains from this point onward will be tax-free after 5 years and age 59.5.

It might be a little painful, but it may be worthwhile to check on your pre-tax IRAs during this dip. If you have been thinking of converting your “Traditional” IRAs over to Roth IRAs, your shrunken gains will lead to a smaller tax bill now, while your (hopefully) future gains from this point onward will be tax-free after 5 years and age 59.5.

Updated March 20th. The US Treasury has announced taxpayer relief for federal tax in response to COVID-19. Here is the

Updated March 20th. The US Treasury has announced taxpayer relief for federal tax in response to COVID-19. Here is the  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)