If you have accumulated some savings bonds but don’t really enjoy logging into TreasuryDirect.gov all the time, here are some alternative methods to tracking your balances over time. Each has its own strengths and weaknesses, and the unofficial ones are the results of motivated DIY investors. As an example, I will track a Savings I Bond purchased in April 2013 for $10,000.

If you have accumulated some savings bonds but don’t really enjoy logging into TreasuryDirect.gov all the time, here are some alternative methods to tracking your balances over time. Each has its own strengths and weaknesses, and the unofficial ones are the results of motivated DIY investors. As an example, I will track a Savings I Bond purchased in April 2013 for $10,000.

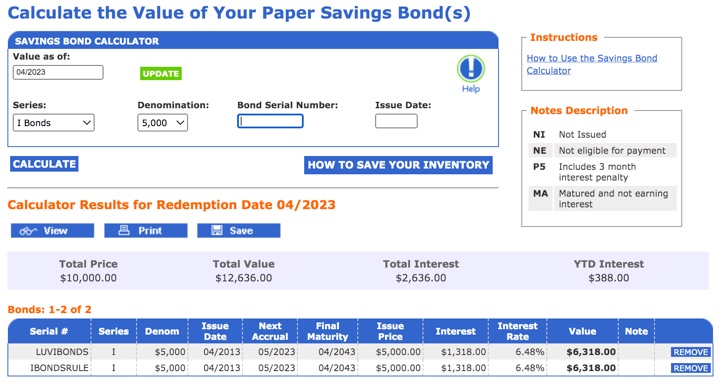

Official TreasuryDirect Savings Bond Calculator

Although this official calculator states that it is only meant for paper savings bonds, you can still use it indirectly to track electronic savings bonds (they have the same value as long as they are issued the same month). For example, let’s say you bought $10,000 of I Bonds issued in April 2013. While you can’t enter a $10,000 value directly, you can enter two $5,000 I Bonds. (Enter anything for serial number.) Thus, you’d see that as of April 2023, they are worth $12,636.

You can even save your entire inventory of specific I bonds if you follow the directions here. It feels a bit archaic (you’re basically saving a plain text .html file), but it works. You can even import the values into Google Sheets, according to this Bogleheads forum post.

Created by a user on the Bogleheads forums, this is a very handy and simple website that tracks the price of every savings bonds based on the issue date. For April 2013, simply click on that date and see the growth in value shown below. As of April 2023, you get the same $12,636 value and since the rate is known for the next 6 months as well, you can see the value all the way out to October 2023. This may lead to the easiest way to import the values into your own custom Google Sheet; check out Bogleheads forum post.

This site also allows you to look up the price history of savings bonds based on the issue date. For April 2013, there are the same ending values along with a chart comparing the value against CPI inflation. You can also quickly create a list of multiple savings bonds here, although it doesn’t appear to allow you to save it for later.

(I personally use these tools once in a while for research, but for tracking balances I simply log into TreasuryDirect.gov during my quarterly portfolio updates and manually enter the values into my Google Sheets page under the “Inflation-Protection Bonds” asset class. It’s only four times a year, and I like to log into the official retro website to make sure my money is still there.)

William Bernstein has a new article titled

William Bernstein has a new article titled  Inflation still 🚀 😬 Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.

Inflation still 🚀 😬 Savings I Bonds are a unique, low-risk investment backed by the US Treasury that pay out a variable interest rate linked to inflation. With a holding period from 12 months to 30 years, you could own them as an alternative to bank certificates of deposit (they are liquid after 12 months) or bonds in your portfolio.  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)