Charlie Munger and his principle of inversion tells us that sometimes the easiest way to achieve something is to flip it and consider the best ways to accomplish exactly what you are trying to avoid. Accordingly, check out this slide deck about Avoiding Financial Disasters by Barry Ritholtz (full 1-hour video presentation here).

If you would like to destroy your wealth, here are the top 10 ways to do so:

This may sound overly simple, but nearly every single wealthy person who has gone broke has used one of these methods. Obviously some of these are harder to avoid than others, but most are clearly identifiable and avoidable. Give them a wide berth. For example, if you had most of your net worth in shares of Silicon Valley Bank or Signature Bank, you may have made big gains for a while, but in the end be left with nothing. You should only have to get rich once.

Also see: How To Make Your Life Completely Miserable

(Top photo credit to Jp Valery on Unsplash)

Here’s my 2022 Year-End income update for my

Here’s my 2022 Year-End income update for my

Here’s my quarterly update on my current investment holdings as of the end of 2022, including our 401k/403b/IRAs and taxable brokerage accounts but excluding real estate and side portfolio of self-directed investments. Following the concept of

Here’s my quarterly update on my current investment holdings as of the end of 2022, including our 401k/403b/IRAs and taxable brokerage accounts but excluding real estate and side portfolio of self-directed investments. Following the concept of

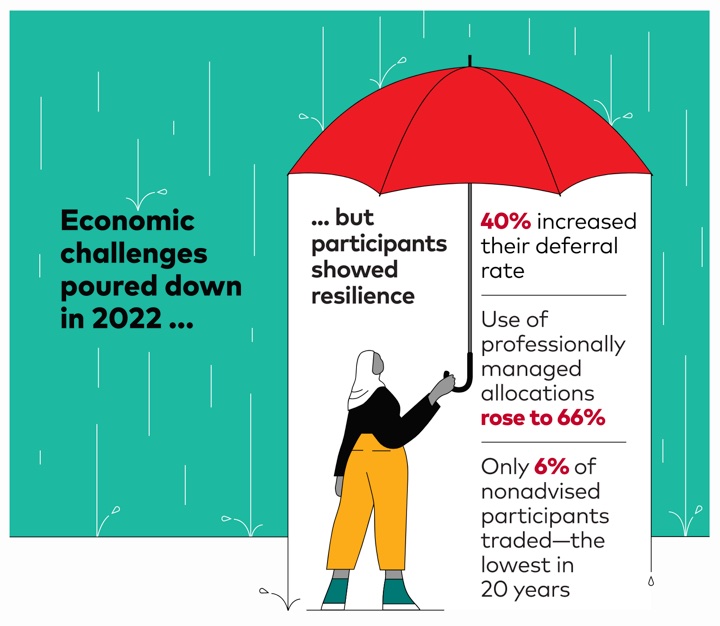

The beginning of the year is also a good time to check on the new annual contribution limits for retirement and benefit accounts, many of which are indexed to inflation. Our income has been quite variable these last few years, so I regularly adjust our paycheck deferral percentages based on expected income for the year. I still try to max things out if I can, or at least stay on pace to do so. This

The beginning of the year is also a good time to check on the new annual contribution limits for retirement and benefit accounts, many of which are indexed to inflation. Our income has been quite variable these last few years, so I regularly adjust our paycheck deferral percentages based on expected income for the year. I still try to max things out if I can, or at least stay on pace to do so. This

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)