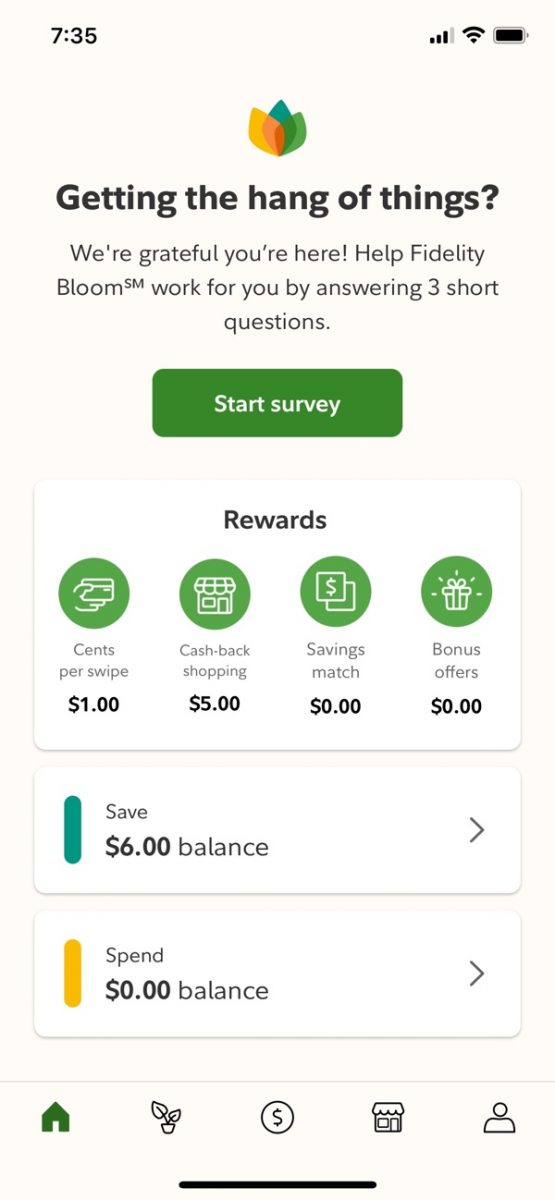

Update January 2024: If you have the Fidelity Bloom app, this is a reminder that the 10% annual savings match is reset and you can again get $30 for a $300 transfer into your Fidelity Bloom Save account. If you use the SPAXX option for cash sweep, you are also earning close to the equivalent of 5% APY (as of 1/3/24). Here is a screenshot of my 2023 rewards:

Full review:

Fidelity Bloom is a new(er) app from Fidelity Investments targeted at helping young adults become more financially aware and develop better savings habits. iOS and Android. Fidelity has included many “behavioral psychology” features from other fintech startup apps like a match on savings transfers, debit card cash back rewards, rounding-up purchases and saving the difference, and shopping portal cashback. The highlights:

- (No new user bonus at the moment. Was $100.)

- 10% annual savings match (up to $30). Get a 10% match on the first $300 saved into their Bloom Save account (up to a $30 match on $300 of new money deposited).

- 10 cents from Fidelity with every debit card purchase. Fidelity will automatically deposit a fixed 10 cents into the Fidelity Bloom Save account every time customers use the Fidelity Bloom debit card. Reminds me of the Citi Rewards+ credit card.

- Automatically round up purchases into savings. Customers can automatically round up purchases to the nearest dollar and have the difference moved to savings from their Fidelity Bloom Spend to their Fidelity Bloom Save account.

- Up to 25% cashback through shopping portal. Receive up to 25% cash back into your Fidelity Bloom Save account when you shop in-app with 1,100+ participating retailers.

Interest rate is competitive (up to ~5% as of 1/3/24 with SPAXX), but it’s a brokerage account. Is it a bank account? Is it a brokerage account? It’s a SIPC-insured brokerage account:

The Fidelity Bloom App is designed to help with your saving and spending behaviors through your Save and Spend accounts, which are brokerage accounts covered by SIPC insurance. They are not bank accounts and therefore are not covered by FDIC insurance.

You do get a routing number and account number for your two accounts, but the cash is held like their other non-retirement accounts. During the sign-up process, you can pick between one of three options for your core position:

- Fidelity® Interest-Bearing Option (FCASH)

- Fidelity Government Money Market Fund (SPAXX)

- Fidelity Treasury Money Market Fund (FZFXX)

Although I have confidence in Fidelity’s long-term experience and conservatism in running these money market mutual funds, the lack of FDIC coverage is something to note. The rates may change daily. View current rates here.

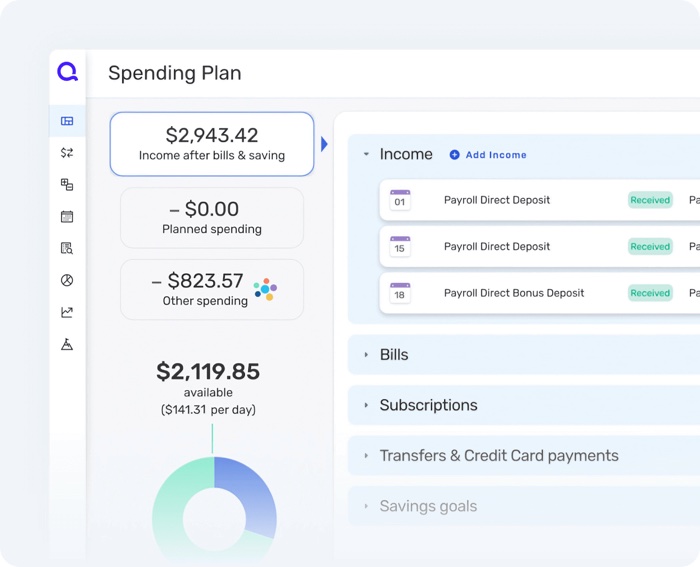

After you open via app, you can see the account balances at Fidelity.com but you’ll still need the app to change any settings. Here’s a screenshot from my app.

Fidelity recently shut down another of its experimental apps called “Fidelity Spire”, so we’ll see if this one catches on a bit better.

For posterity, here are the terms & conditions for the (expired) $100 limited-time offer:

This offer is valid for new or existing Fidelity Brokerage Services LLC (“Fidelity”) customers who make an initial total deposit of at least $50 (“Qualifying Deposit”) into their Fidelity Bloom Spend account or Fidelity Bloom Save account on or after August 13, 2023 through the Fidelity Bloom app. This offer is limited to one cash award per individual. For clarity, existing Bloom clients who have not yet made any deposits into either of their Fidelity Bloom Spend or Fidelity Bloom Save accounts can participate in this offer by making a Qualifying Deposit by August 27, 2023. Existing Fidelity customers who have previously made deposits into their Fidelity Bloom Spend or Save accounts, including individuals who have already participated in the Bloom $50 offer, are not eligible for this offer.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)