![]()

2022 Year-End Update. Each year, I have a side goal of earning the equivalent of the maximum annual IRA contribution limit ($6,000 for 2022) using the profits from various finance promotions alone. In 2021, I reached $5,592 in bonuses and $2,500+ in extra interest. If you had put $6,000 into your IRA every year for the recent 10 year period (2013-2022) and invested in a simple Target Date retirement fund, you would have turned small, weekly deals into a $87,000+ nest egg.

That’s worth repeating: An extra 87 grand has been the real-world result of regularly investing $500 a month for 10 years! A couple could double these numbers.

Ground rules: Real-world results for one real person only. Following with My Money Blog tradition, this will track my personal, real-world results. It would be quite easy to list a bunch of random promotions that add up to $6,000, but these will be promotions that I personally sign up for and complete the requirements (even though I’ve already opened so many bank accounts, credit cards, and brokerage accounts over the years). I will track my individual results only, although my partner does also participate on a more selective basis. Nearly all of them have been documented in real-time in the Deals and Offers category, Top 10 credit cards list, and brokerage bonus list.

Note: I am also excluding the $900 bonus from Chase Ink Business Cash card, since it is meant for small businesses.

2022 bonuses and promotions list. The 💵 symbol means I have received and/or cashed out the bonus successfully. The ⌛ symbol means the promo is still in progress.

- SoFi Checking $275 Direct Deposit Bonus (still live) 💵

- Current fintech app $50 Bonus (still live) 💵

- Amazon “Pay With Points” offers from American Express, Discover, Chase, Citibank (check if targeted) 💵

- Schwab Brokerage $101 Starter Kit Promo (still live) 💵

- Lafayette Federal Credit Union $100 Bonus (expired) 💵

- Capital One Venture X $200 AirBnB Credit + $100 Global Entry (offer changed but still $600+ first year value) 💵

- Gemini $150 Bitcoin bonus (expired) 💵

- Chase Aeroplan Credit Card 100k Bonus + $100 Global Entry (offer changed but still $600+ first year value) 💵

- CIT Bank Free Year of Amazon Prime (expired) 💵

- M1 Spend Checking Account $100 bonus (expired) 💵

- Marcus Bank $100 Deposit Bonus (live again until 2/15) 💵

- Citi Premier Credit Card 60,000 points worth $600 in gift cards or travel like airfare booked via their travel portal + $100 Global Entry (offer changed, still $500+ value) 💵

- Axos Invest Brokerage $150 bonus (still live, now $200) 💵

- Axos Bank $100 bonus (still live) 💵

- SoFi Personal Loan $600 bonus (still live, now $300) 💵

- Fidelity Bloom App $86 bonus (still live) 💵

- Target Deal Days 2022: 5% Off $500 in Gift Cards (expired) 💵

- Amazon Prime Day 2022: $10 stampcard, $12.50 gift card promo (expired) 💵

- Plynk brokerage app $50 Learn & Earn bonus (expired) 💵

- CreditUnion 1 $500 checking account promo (expired) 💵

- Amazon “Pay With Points” offers (see above; got another $40 of easy savings during October Prime Day) 💵

- PNC Bank up to $400 bonus (still live) ⌛

- Bank of America 2% More Rewards Day (expired) 💵

- Amazon $10 Venmo, Amazon Black Friday/Cyber Monday GC promos (expired) 💵

- SkyOne FCU $400 Checking bonus (expired) ⌛

- Target $10 off $100 Apple GC (expired) 💵

- Plynk Invest $100 for new/existing users (still live) 💵

- Wings Financial $200 Checking bonus (expired) ⌛

- Equifax Data Breach Settlement $21.06 (expired) 💵

- Capital One Venture X: $300 Travel Portal Credit (still live) 💵

Bonuses that required significant assets to max out (but not necessarily participate)

- Public ACAT transfer bonus (Up to $10k) (still live, lowered bonus tiers) 💵

- SoFi up to $1,000 deposit bonus (expired) 💵

- Ally Bank up to $500 deposit bonus (expired) ⌛

2022 final results. The total tally for bonuses not requiring significant assets was $6,259 total for 2022, which was 104% of the $6,000 annual IRA contribution limit for 2022. This excludes the three bonuses (Public, SoFi, and Ally) that paid out bigger bonuses for larger asset transfers or cash deposits. I acknowledge not everyone has enough assets to max those out, but they were certainly an efficient use of time if you did. If you add in the $3,500 that I received from those bonuses, the total would be $9,759.

Additional background stuff. This is a personal challenge/game that I like to play. I enjoy trying out new apps and services. I look for the best payoff/effort ratio for my situation; your choices won’t look like my choices. In addition, some things I will skip simply because I’ve already done them. For those new to this hobby, I would first grab the low-hanging fruit like the Chase Sapphire Preferred or the Chase Sapphire Reserve and build up a nice stash of flexible Ultimate Rewards points. After that, I would recommend looking at the Citi Premier (ThankYou points), Capital Venture X (Capital One Miles), and American Express Gold (AmEX Membership Rewards points) to jumpstart your points stashes.

These numbers included fixed bonuses for short-term asset transfers, but ignore higher interest rates overall from buying US Treasury bonds or savings bonds. They also ignore ongoing credit card purchase rewards like 2% to 2.6% cash back on all credit purchases (or airline miles or hotel points) and 5% cash back on specific categories or 1% or better cash back on rent.

This is an enjoyable and profitable hobby for me, but I don’t like to waste my time either. I look for a solid return based on the time commitment required. I tend to avoid speculative bets, bonuses that are hard to convert to real value, and anything that requires driving to stores where things may or may not be in stock. The deals that I post usually last at least a few days, but it’s a bit like value investing where you have to be ready to get off your butt and take decisive action when an opportunity shows up, because they won’t last forever.

Here’s my 2022 Year-End income update for my

Here’s my 2022 Year-End income update for my

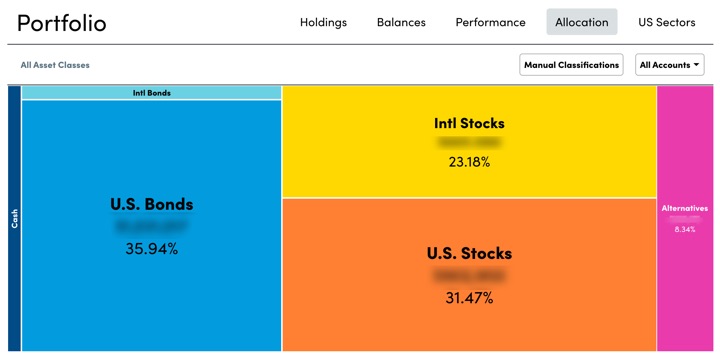

Here’s my quarterly update on my current investment holdings as of the end of 2022, including our 401k/403b/IRAs and taxable brokerage accounts but excluding real estate and side portfolio of self-directed investments. Following the concept of

Here’s my quarterly update on my current investment holdings as of the end of 2022, including our 401k/403b/IRAs and taxable brokerage accounts but excluding real estate and side portfolio of self-directed investments. Following the concept of

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)