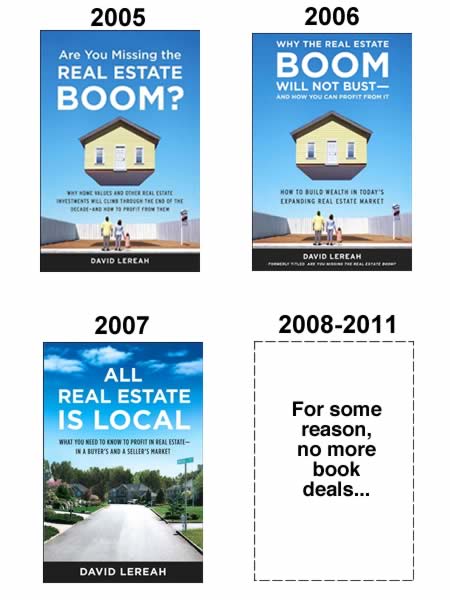

I ran across this funny image on Imgur and just had to recreate it with a bit more detail. All of these books are by the same author, David Lareah, along with the publishing dates of each book. (The first two books are essentially the same book with different titles.)

Hover your mouse cursor over each book cover below to see the full titles, the progression is both funny and sad. Or, you can click on each book cover to see the corresponding Amazon book page. Comparing old and new reviews for the books can also be a nice lesson in investor psychology.

Now, which popular books of today will be the jokes of tomorrow?

WaPo has a story about a college student who makes

WaPo has a story about a college student who makes

I’m catching on some personal finance magazine reading and find myself again rolling my eyes at their respective “Best Mutual Funds” lists. I’ve had subscriptions to all the major magazine for about 5 years now. Here’s how I translate them through my jaded eyes:

I’m catching on some personal finance magazine reading and find myself again rolling my eyes at their respective “Best Mutual Funds” lists. I’ve had subscriptions to all the major magazine for about 5 years now. Here’s how I translate them through my jaded eyes:

I was going through some old financial files and came across an old E-Trade statement which was my first brokerage account and found my first shares of stocks ever purchased in August of 2001. This was after the dot-com bubble burst, and I was still in grad school. I had managed to save up $1,000 and promptly invested it after pretty much zero research:

I was going through some old financial files and came across an old E-Trade statement which was my first brokerage account and found my first shares of stocks ever purchased in August of 2001. This was after the dot-com bubble burst, and I was still in grad school. I had managed to save up $1,000 and promptly invested it after pretty much zero research:  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)