Our World in Data has a very in-depth page on Causes of Death from around the world. Then they asked: Does the news reflect what we die from? What if they compared what we read in the news and the raw data? Here is a chart that compares actual death stats against Google search data and the mentions of causes of death in both the New York Times and The Guardian newspapers (click to enlarge):

Two-thirds of us will die from either heart disease, cancer, diabetes, or kidney disease. Meanwhile, over 70% of the causes of death you’ll read about in the news are either murder, suicide, or terrorism.

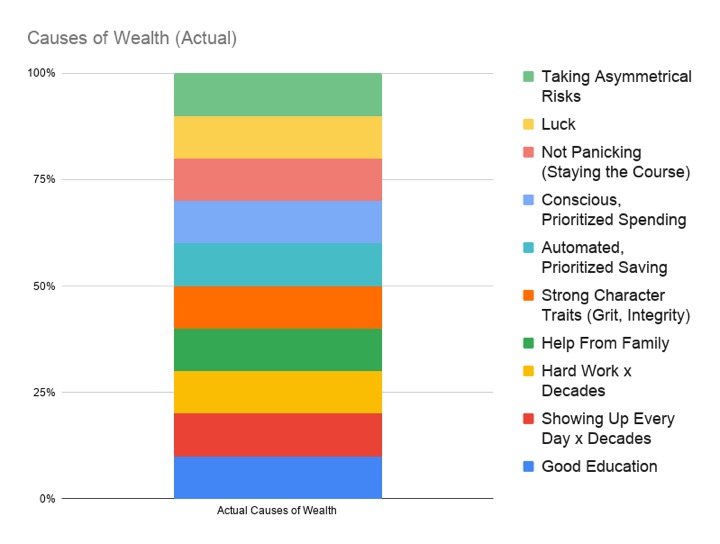

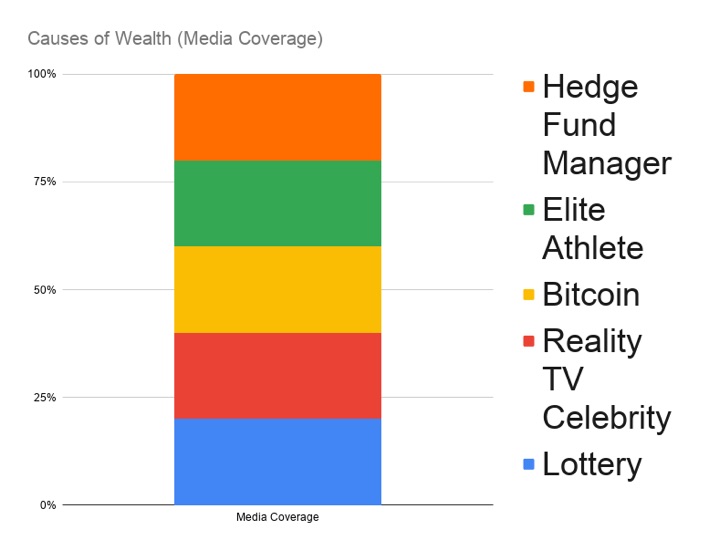

What about the disconnect between reality and what we read in the news about becoming wealthy? Here’s my quick take using a Google Spreadsheet (obviously not exact or based on actual data):

Most people probably realize that the news does not exactly reflect the real world. However, we can still unconsciously develop a “bias for single events”, even with financial topics. There’s also “social media bias” where what you see is only the highly-edited positive clips of their life. You see their #bestlife, but what you don’t see are their credit card debt, the downpayment from the Bank of Mom and Dad, or anxiety attacks about money.

I feel like I’ve been reading a lot of backlash against the “latte factor”. I agree buying a Starbucks latte every day will not directly lead to poverty, and forgoing it will not make you independently wealthy. However, sometimes a concrete example is more powerful than a vague position like “just prioritize your spending” (which I believe, but sort of like “spend less than you earn”).

I feel like I’ve been reading a lot of backlash against the “latte factor”. I agree buying a Starbucks latte every day will not directly lead to poverty, and forgoing it will not make you independently wealthy. However, sometimes a concrete example is more powerful than a vague position like “just prioritize your spending” (which I believe, but sort of like “spend less than you earn”). In the post

In the post

Cashing in your frequent flier miles for a free flight can be hit or miss, especially around a holiday. Which airlines are the most generous with making seats available? Each year, consulting firm IdeaWorks tries to run a fair comparison of all the major airlines to keep them honest. This

Cashing in your frequent flier miles for a free flight can be hit or miss, especially around a holiday. Which airlines are the most generous with making seats available? Each year, consulting firm IdeaWorks tries to run a fair comparison of all the major airlines to keep them honest. This

Updated with alternative method. My relative lack of travel these days means that I am constantly keeping miles and points from expiring. Here’s the

Updated with alternative method. My relative lack of travel these days means that I am constantly keeping miles and points from expiring. Here’s the

Despite the fresh packaging, we should remember that the “FIRE” concept (Financially Independent, Retire Early) is anything but a new concept. Even I can’t help being a little intrigued by the clickbait title “This Secret Trick Let This Couple Retire at 38”. Such an article could have been written about the

Despite the fresh packaging, we should remember that the “FIRE” concept (Financially Independent, Retire Early) is anything but a new concept. Even I can’t help being a little intrigued by the clickbait title “This Secret Trick Let This Couple Retire at 38”. Such an article could have been written about the  After finishing

After finishing

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)