If comparing this blog to the restaurant world, I like to think of it as the stubborn Mom & Pop hole-in-the-wall with one location. It’s been around for a long time, but there are no second locations, no franchises, no frozen food line. It was never sold to a private equity firm or some publicly-traded corporation. It owns the building and the land underneath, so it can just keep on doing its own thing.

When I first saw the book Serious Eater: A Food Lover’s Perilous Quest for Pizza and Redemption, I had no idea who Ed Levine was. I originally thought that Serious Eats was a little food blog run by J. Kenji Lopez-Alt as a side gig outside of his day job, just as I started MyMoneyBlog.com. I don’t live in New York and had read a few posts like their viral posts like the In-N-Out Menu Survival Guide and now use their reversed-sear prime rib recipe every year.

The truth is actually very different, and I quickly became engrossed in the story behind Serious Eats.

- Instead of a young blogger working out of their tiny studio and a $10/month web-hosting package, Ed Levine was a former advertising executive in his 50s who started out immediately with a salary for himself, a salaried team, and an office space. This was possible due to a $500,000 loan from his older brother.

- Instead of running lean and looking for profitability quickly, Serious Eats never made a profit from 2006 to 2015. It grew in viewership and gross revenue, but my understanding is that even when it was eventually sold, the advertising revenue never exceeded the running costs (salaries, office space, other overhead).

Ed Levine was obsessed with food and the stores behind it. You can get a taste of his energetic personality in this 1997 NYT Times article “On an Odyssey With the Homer Of Rugelach” by Ruth Reichl.

Her story in the Times called me the “missionary of the delicious.” Ruth described what I did better than I ever could: “Mr. Levine is on a crusade to see that the people who make food get the recognition they deserve. He sees them as creative artists waging a losing battle against mechanization, and he cheers them on.”

Serious Eats was definitely a passion project. However, Mr. Levine never excelled at the financial side. In fact, this was his first true business venture.

But that was before I understood a fundamental truth about individual investors: just because someone has made enough money to invest in a speculative venture like Serious Eats doesn’t mean they won’t be upset if they lose it. That goes double if they are family. People who have made money usually didn’t make it with a casual attitude about money in general.

However, he did raise a million dollars of startup money from family and friends, so you have to give him that. He had the charisma and infectious optimism that convinced people to bet on him:

And just like the folks at a victory party, we really felt we were on a mission: to change and democratize the food culture through food media without dumbing it down or pandering. Maybe art and commerce could coexist peacefully. Maybe they could even complement each other. Maybe my belief that creating good content could and would lead to financial success wasn’t as ridiculous as the money guys seemed to think.

Serious Eats grew in popularity. If you are at all interested in food, you’ve probably heard of it.

Back at Serious Eats World HQ some of our posts were going viral. Kenji chronicled in words and pictures the “In-N-Out Burger Survival Guide,” in which he ate every single item on its twenty-eight-item secret menu. That one post attracted 3.5 million unique visitors in the first year it was up.

However, they never really stopped burning through money. They missed the boom time of website sales before the Great Financial Crisis of 2008. They later tried to sell to a variety of different buyers in 2010 to 2011, but that was a slow period in media acquisitions.

Ed Levine went back and begged and borrowed money from every source imaginable. He borrowed even more money from his older brother, eventually making the total owed somewhere over $600,000 (I lost count). He accumulated $650,000 in personal debt that was straining his marriage, as it was backed by the New York apartment jointly owned with his wife. His wife Vicki later took on a margin loan backed by her personal stock holdings. Multiple close friends lent him $100,000 each. In other words, he was risking all of his closest personal relationships.

In fact, the most harrowing details I’ve had to relive in writing this book have nothing to do with financial security, only the terrifying knowledge of how close I came to doing real damage to the relationship that made it all possible.

You could feel the desperation at this point. It’s all about timing, as if you’re selling an unprofitable growth business, you need buyers with loose money and an appetite for risk. (Look up the current status of WeWork.) Somehow, he finally sold Serious Eats to Fexy Media in 2015. The details are blurry, but it seems that the investors were mostly made whole and Levine was able to pay back all his debts with a small bit of profit. He’s now an employee, not the owner, but perhaps that is for the best.

But thankfully, it’s not quite so personal. Most everyone who works at Serious Eats these days thinks of it as a business first and then, perhaps, a calling. Some people who work at the company may just think of their job as a really good gig. I’m okay with that. Maybe that’s why Serious Eats is doing so much better as a business. Serious Eats is growing up. And that’s okay. So have I.

In the end, this amazing story was powered solely by the energy of Ed Levine (and the equally-amazing support of his wife Vicki). I feel like it really shouldn’t have worked out at all. The climax felt a bit like the ending of the movie The Gambler. You don’t know much about running a website (or any startup), you burn through over a million dollars of money, and your passion is eating and sharing about food. However, he made it out intact and helped establish other talented food writers like J. Kenji Lopez-Alt, Max Falkowitz, and Stella Parks.

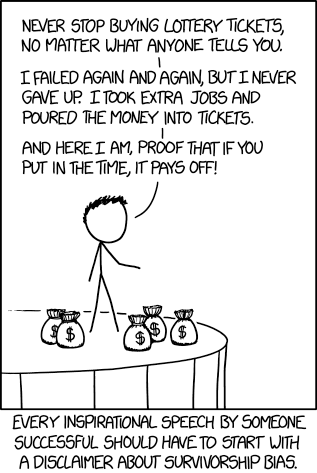

This reminded of these tweets about taking asymmetrical risks that have been stuck in my head:

Asymmetric opportunities:

Invest in startups

Start a company

Create a book, podcast, video

Create a (software) product

Go on many first dates

Go to a cocktail party

Read a Lindy book

Move to a big city

Buy Bitcoin

Tweet— Naval (@naval) October 24, 2018

A prudent risk is when there's no consequential downside.

A foolish risk is when the worst-case outcome cannot be tolerated.

Not every prudent risk is worth taking, but every foolish risk should be avoided.

— Daniel Vassallo (@dvassallo) October 22, 2019

Maybe you can try to make the risk asymmetric, but in the end there is no easy formula. I could not have taken the risks that Ed Levine did with Serious Eats. It would have been a foolish risk for me, as I could never tolerate the financial risk nor the relationship risks. However, when I read about others it seems they are compelled to take such big risks, and somehow it their boldness it can all work out. Of course, I suppose there wouldn’t have been a book about Serious Eats to read if it didn’t.

I hope that everyone had a boring Labor Day weekend! I say that because boredom is a magical thing, especially when left untreated with a computer/TV/smartphone screen. I had a lovely quiet afternoon where I sorted out a big box of old electronics, and my mental wanderings inspired me to make some important changes in my daily schedule.

I hope that everyone had a boring Labor Day weekend! I say that because boredom is a magical thing, especially when left untreated with a computer/TV/smartphone screen. I had a lovely quiet afternoon where I sorted out a big box of old electronics, and my mental wanderings inspired me to make some important changes in my daily schedule.

There is an ongoing debate about personal finance education in school. It sounds like a good idea, but

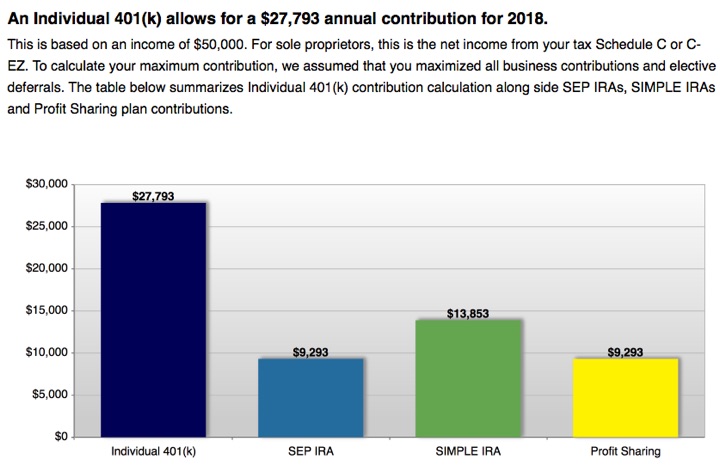

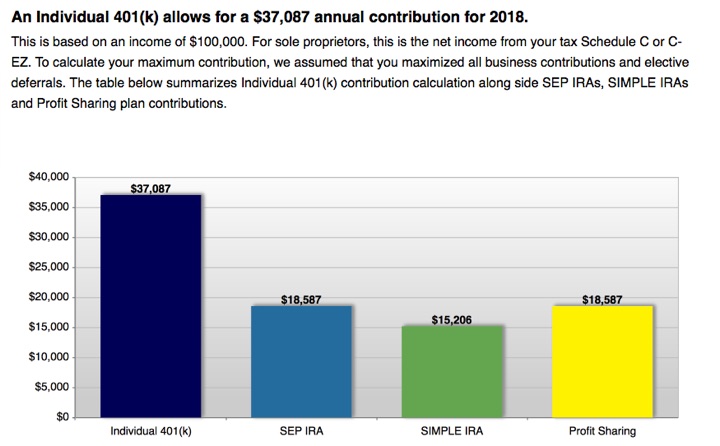

There is an ongoing debate about personal finance education in school. It sounds like a good idea, but  Each December, I run the numbers to see how much more I can contribute to my Self-Employed 401k plan, aka Solo 401k or Individual 401k.

Each December, I run the numbers to see how much more I can contribute to my Self-Employed 401k plan, aka Solo 401k or Individual 401k.

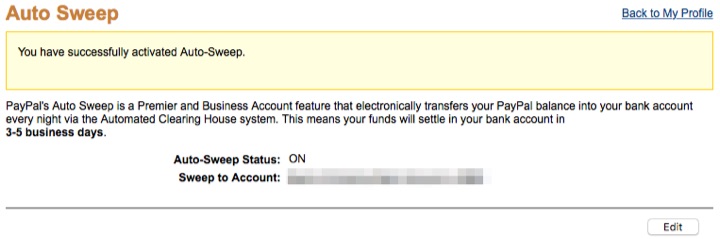

If you use PayPal to accept credit cards for your small business (eBay, Etsy, e-store, freelance, etc), you may not want to keep your money sitting at PayPal (especially if you are earning higher interest in your bank account). There is a feature called Auto Sweep that checks daily and automatically “sweeps” any money that arrives in your PayPal account into your bank account overnight.

If you use PayPal to accept credit cards for your small business (eBay, Etsy, e-store, freelance, etc), you may not want to keep your money sitting at PayPal (especially if you are earning higher interest in your bank account). There is a feature called Auto Sweep that checks daily and automatically “sweeps” any money that arrives in your PayPal account into your bank account overnight.

While reading the

While reading the  Charles Munger is probably best known as the Vice Chairman of Berkshire Hathaway and partner of Warren Buffett. The University of Michigan Ross School of Business recently shared a

Charles Munger is probably best known as the Vice Chairman of Berkshire Hathaway and partner of Warren Buffett. The University of Michigan Ross School of Business recently shared a  I’m a sucker for people turning their unique interests into a profitable small business, especially a quirky one-person business (like this person who

I’m a sucker for people turning their unique interests into a profitable small business, especially a quirky one-person business (like this person who

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)