Update April 2024: SoFi made a few notable changes recently, both positive and negative:

- The SoFi Unlimited 2% Credit Card will now offer 10% boost on their rewards with direct deposit into SoFi Checking or Savings. This would work out to 2.2% cash back rewards points on everyday purchases, 3.3% cash back rewards points on SoFi Travel purchases, and 27.5% cash back rewards points on SoFi Stadium purchases.

- There is a new inactivity fee of $25 per account for every 6 months of login inactivity.

- The outgoing ACAT transfer fee was increased to $100. Previously $75.

- The SoFi 2% IRA match promo is scheduled to end soon; it runs until 4/15/24.

The rest of the offers:

SoFi (“Social Finance”) is an all-in-one finance app that expanded from students loans into banking, stocks, crypto, credit cards, and more. Here are some of their other offers; New users can receive a separate opening bonus for each separate part of SoFi (Money, Invest, Loans, etc).

- SoFi Checking Referral Offer: Up to $325 new user bonus. Open a new SoFi Money account and add at least $10 to your account within 5 days, and get $25. Then get up to $300 additional bonus with qualifying direct deposit. Plus up to 4.60% APY.

- SoFi Invest Referral Offer: $25 new user bonus. Brokerage account. Open an Active Investing account with $10 or more, and you’ll get $25 in stock.

- SoFi Invest Alternate Offer: Claw Game. Feeling lucky? Compare a guaranteed $25 above against having a 0.028% chance of a $1,000 bonus. (That is less than 1 in 1000 odds.)

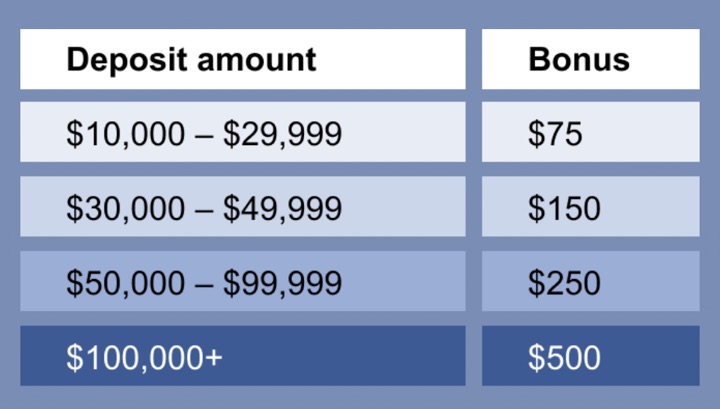

- SoFi Invest Asset Transfer Offer: Up to $5,000 Bonus. Transfer over your existing assets from another broker and SoFi will pay you a bonus. From $50 bonus for transferring $5,000 in assets all the way up to $5,000 bonus for $2 million in assets.

- SoFi Student Loan Refi: $300 bonus. Warning: Do your research before refinancing your Federal student loans to a private lender.

- SoFi Doctors and Dentists Student Loan Refi: $1,000 bonus. Special low rates just for doctors and dentists.

- SoFi Private Student Loan: $100 bonus.

- SoFi Personal Loans Referral Offer: Fixed $300 bonus. Fixed $300 bonus, 90 days after successful funding. The loan has no fees and you can pay it back in full after 90 days (you can pay it down to $50 before then to accrue minimal interest).

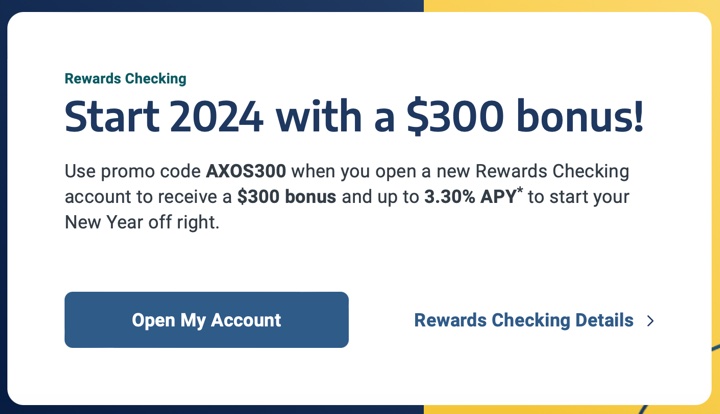

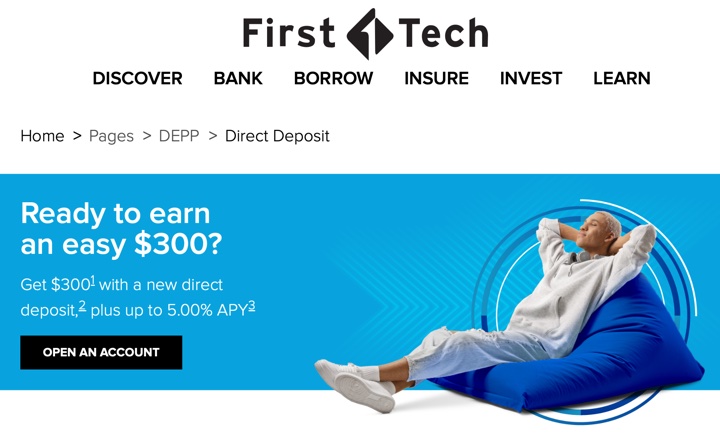

Deal is back again through 3/30. Get a

Deal is back again through 3/30. Get a

Activation reminder for 2024 2nd Quarter. The credit cards below offer 5% cash back and up on specific categories that rotate each quarter. It takes a little extra attention, but it can add up to hundreds of dollars in additional rewards per year without changing your spending habits. You can also buy gift cards at places with 5% back now but spend the gift cards later. (* You can buy gift cards from lots of different places at grocery and drug stores…) New cardmembers may also get an upfront sign-up bonus.

Activation reminder for 2024 2nd Quarter. The credit cards below offer 5% cash back and up on specific categories that rotate each quarter. It takes a little extra attention, but it can add up to hundreds of dollars in additional rewards per year without changing your spending habits. You can also buy gift cards at places with 5% back now but spend the gift cards later. (* You can buy gift cards from lots of different places at grocery and drug stores…) New cardmembers may also get an upfront sign-up bonus. Chase Freedom Flex Card

Chase Freedom Flex Card Discover it Card

Discover it Card Citi Custom Cash Card.

Citi Custom Cash Card. American Express Blue Cash Preferred Card

American Express Blue Cash Preferred Card

Updated March 2024. Do you have small business income or work as an independent contractor? Freelance, Uber/Lyft, Amazon, eBay, Etsy, Airbnb? A small business credit card separates your personal and business expenses and can build up your business credit profile. If you are not a corporation or LLC, you can apply as a sole proprietorship, with your name as the business name and your Social Security number as the Tax ID number. These are the top 10 credit card offers that I would personally apply for right now (or have already). Recent changes:

Updated March 2024. Do you have small business income or work as an independent contractor? Freelance, Uber/Lyft, Amazon, eBay, Etsy, Airbnb? A small business credit card separates your personal and business expenses and can build up your business credit profile. If you are not a corporation or LLC, you can apply as a sole proprietorship, with your name as the business name and your Social Security number as the Tax ID number. These are the top 10 credit card offers that I would personally apply for right now (or have already). Recent changes:

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)