As a follow-up to Vanguard founder Jack Bogle’s 2015 stock market prediction paper and related Morningstar article, here are a few selected slides from the presentation deck by Jack Bogle at the Bogleheads XIV conference in October 2015.

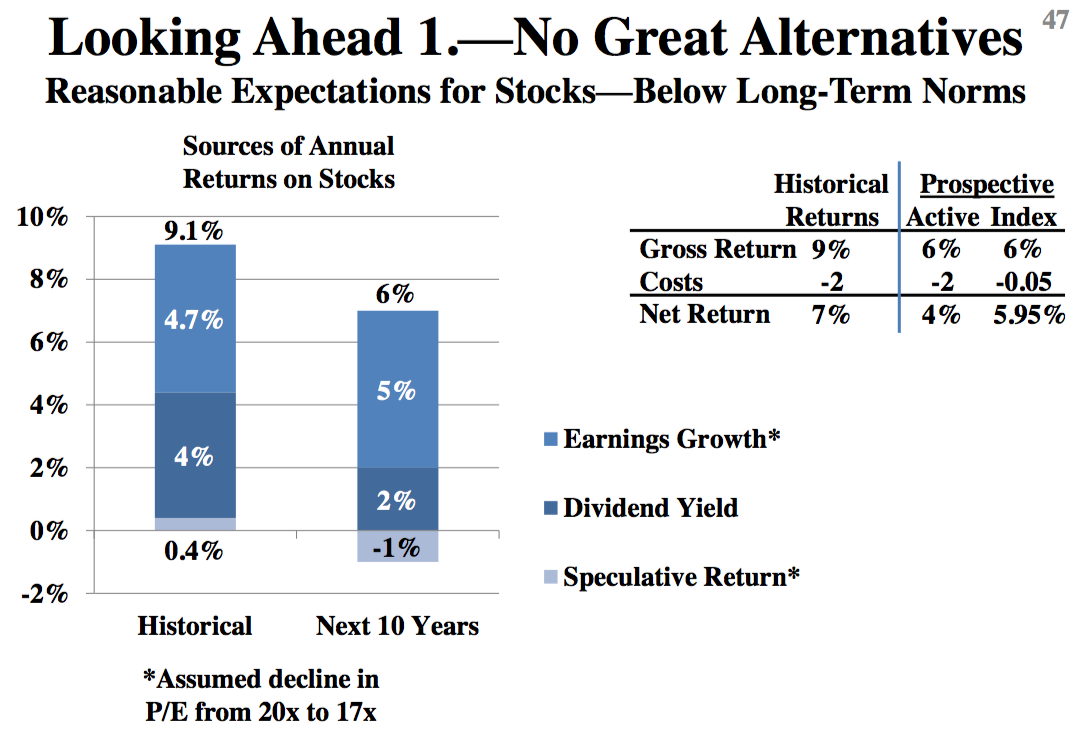

The formula for predicting future stock market returns is:

Future stock returns = Current dividend yield + Predicted earnings growth ± (Reversion to long-term average P/E ratio)

The formula for predicting future bond market returns is:

Future bond returns = Current yield to maturity

At 6% nominal for stocks and 3% nominal for bonds, both 10-year numbers are below long-term averages. However, the 10-year breakeven inflation rate based on TIPS and Treasury yields is roughly 1.5% as of now (late 2015). Using those inflation numbers would result in 4.5% real returns for stocks and 1.5% real returns for bonds, a brighter picture than that painted by other forecasts.

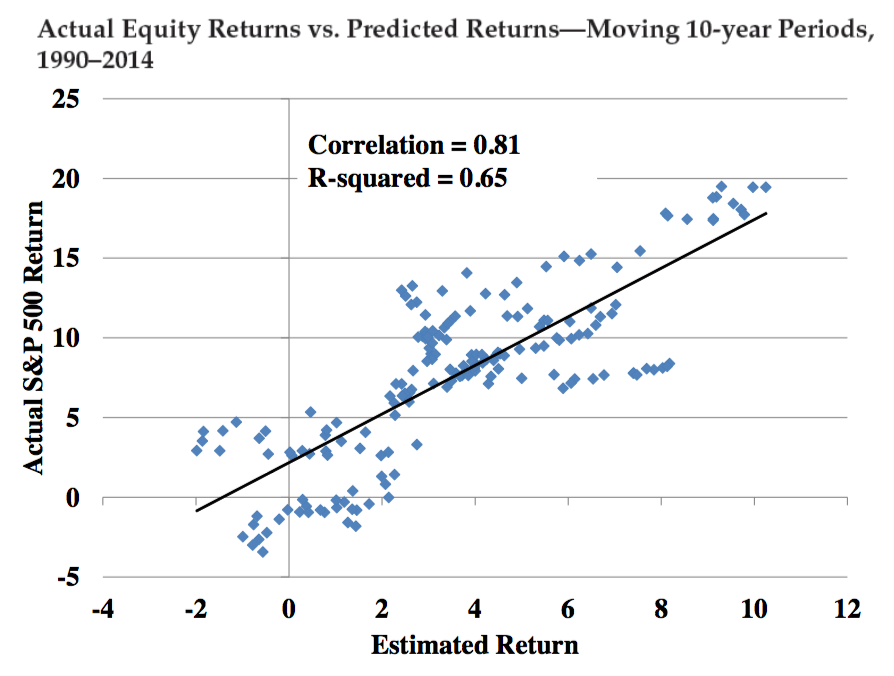

Admittedly it is not a large sample size, but here is a plot of how the 10-year predictions have done so far (1990-2014):

As noted previously, I like to keep track of these forecasts along with those provided by:

- Research Affiliates Expected Returns by Asset Class Tool

- Portfolio Solutions® 30-Year Market Forecast for 2015

- GMO 7-Year Asset Class Return Forecasts, December 2015

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Good article. The last chart seems off though. When comparing actual to estimated returns shouldn’t the scale be the same for both? I think if the scale were the same, the estimated returns would show more divergence from actual returns.

High risk / Low return / No place is safe.

Though I calculated that if the brilliant Iraq and Afghanistan illegal invasions never occurred and that money was divided up and distributed to tax payers who actually pay taxes it would have probably resulted in a check for about $35,000 per tax payer. Which would almost cover the cost to the non-criminal elite for living with zero percent interest rates for 8 years.

Jonathan,

Great article, I never invest in Bonds because they bring small interest rates. When I want to play on safe I invest in funds they are much better solution for safe investing, with higher numbers then bonds. I would rather be bit risky player, with average interest of 7% then safe player with interest of 3%.

I am not sure what you mean by saying “When I want to play on safe I invest in funds”. What do you mean by funds? It doesn’t make any sense.

Could you please share where are you allocating funds? Vti/bond?

You can find my most recent portfolio holdings here:

https://www.mymoneyblog.com/my-money