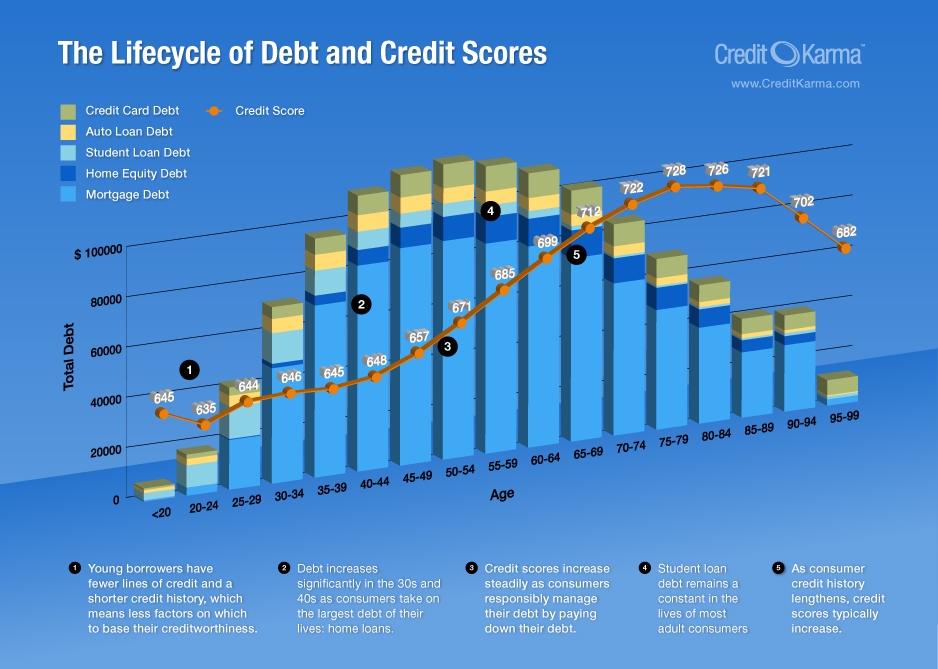

CreditKarma.com (which provides free credit scores) recently released an infographic “The Lifecycle of Debt and Credit Scores” that shows both the average credit score and the average amounts of different debt types by age bracket. I notice that mortgage debt jumps significantly from the 30-34 to the 35-39 bracket, and sadly doesn’t go back down to those levels until past age 80. I’m surprised by the amount of mortgage debt from the 65+ crowd.

It’s also a little sad to see credit card debt being held by someone 95-99, and I also wonder why average credit scores start to decrease again after age 80. Is it because of increased money problems from health issues, or something like a “you can’t take it with you” attitude?

(click to enlarge)

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Me, too. I have always operated with the mindset that the goal is to have the mortgage paid off before retirement. Maybe refis to free up cash for other things is behind that – I’d like to see the same snapshot for 10 years ago, 20 years ago, 30 and so forth.

Scarier still is that there are still some in their late 60s and early 70s dealing with student debt.

There is a big debt load in the boomer’s age range. Will we see a massive default by death wave in the next 20 years.

Average score for the 75-79 cohort is the highest of all at 728??? are consumer credit ratings agencies and lenders insane? Current avg life expectancy is max 3 years in this age and these are the people viewed as the best credit risk?

Once I heard a radio program where the individual was advocating being more in debt as you get older because when you die debt is not passed on so you may as well spend like crazy. Not exactly a POV that speaks to the goodness of people but also is perfectly correct.

RE: Dropping credit scores for the older – I’d imagine it has something to do with income levels. Credit scores are all about ability to repay, and in general, someone above 80 is going to have less resources than someone younger. Besides the unlikelyhood of still working, you’ve likely been drawing down on savings for 15 years.

Plus, frankly, you have a shorter time left to pay, which makes you a higher risk, particularly for unsecured debt.

My guess is that the declining credit scores at 80+ are at least partly not money-related. Towards the end of life for the elderly, I am betting it’s typical to miss payments due to hospitalization, dementia, or other health crises. My mother had a durable power of attorney for my grandmother, and she still had to jump through a lot of hoops with the banks and have good cash flow herself to keep my grandmother’s bills paid on time at the end of her life (no debt, just utilities and home care and such.) Merrill Lynch in particular was ridiculous and wanted new powers of attorney on their own forms even when my grandmother would no longer have been competent to give one due to pain and fatique from cancer.

@Hawks – your life expectancy numbers are incorrect. As of 2007, average life expectancy for someone age 71-72 is 12.3 years, down to 9.9 for 78-79, in the United States.

You appear to be talking about the average life expectancy at birth of 77.9, which takes into account all those who die younger. Once you have reached higher ages, your life expectancy goes up.

I suspect that the debt $ amounts are only for the % of people who have such debts.

I mean look at the student loan figures. Why would so many people in their 70’s have student loans of such high amounts to give an average that is even noticable?? Less than 2% of the population over age 65 has any student loan debt as of 2007.

Few people in retirement have mortgages. As of 2007 data only 11% of people 75 or older had a mortgage at all. I don’t believe that the average mortgage debt for people in their 70’s could be as high as the picture implies. So I assume the debt figure is the average amount owed by people who still have mortgages.

THe lower credit scores for the elderly could also be partially due to generational differences towards credit. Credit card use didn’t become so prevelant until the past few decades. In my grampas generation it really wasn’t as common to use credit so much, therefore people of that age would likely have less credit history.

Hawks said: “Will we see a massive default by death wave in the next 20 years.”

Debts get first claim on the estates. Most people have some value in their estate. At least enough to pay off a few thousand in credit card bills. Its more likley the debts of the boomers will eat into inheritances.

it may be a vastly different picture 10 years from now. Nowdays student loas are significantly larger than 20 years ago forcing people to put off adding mortgages for far longer period.

Very cool graphic!

I’m surprised by the mortgage debt in the 65+ crowd too, unless that’s due to refinancing.. I would expect the home equity to be higher. I know a lot of people in that age group who set the clock back on their mortgage to fund college for their kids. I don’t know what they’re going to do later in retirement…

As for the credit card debt in later years… I know many people in their 60’s with the attitude of, “I’m getting as many credit cards as I can and I’m going to max every one of them out. They can’t make me pay when I’m dead!”

It’s a sad commentary on our society, given that their parents viewed debt as a contract that needed to be repaid in full and in good faith. It was the honorable thing to do. Sadly, the 60’s generation seems to be all about themselves and getting theirs while they can.