The current “full” retirement age for Social Security is 66, although you have the option to start taking benefits at a permanently reduced rate at age 62 (did you know that over 35% of people take this permanent ~25% cut in benefits!). The full retirement age for Social Security in the US is 67 years for workers born after 1960, but that is always subject to future change. Here’s a Wikipedia page comparing the current “standard” retirement ages in various countries.

The current “full” retirement age for Social Security is 66, although you have the option to start taking benefits at a permanently reduced rate at age 62 (did you know that over 35% of people take this permanent ~25% cut in benefits!). The full retirement age for Social Security in the US is 67 years for workers born after 1960, but that is always subject to future change. Here’s a Wikipedia page comparing the current “standard” retirement ages in various countries.

Why do I bring this up? Last month, Australia announced that it plans to increase its official retirement age to 70 by the year 2035. Here’s an AARP article about 14 countries — including Germany, Italy, Spain, Greece and Ireland — who are planning to increase their retirement ages to between 67 and 69 by 2050.

I’m in my mid-30s now, and unlike some I still expect Social Security to be around for a long time. But I also predict that the full retirement age for Social Security will be raised in a similar, and that I won’t get full benefits until age 70.

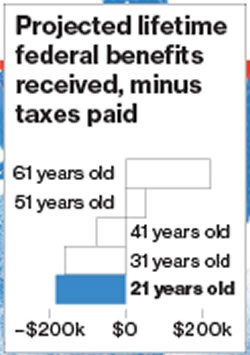

Check out how the math is working against younger workers, via Businessweek:

Also consider that 1 in 3 people born today are expected live to 100, so for the system to work they’ll likely be expected to work at least 50 of those years. That could be 50 years of 50-hour workweeks (especially if you include commuting) for 50 weeks of the year. Yikes. No wonder I like to learn about the principles behind financial freedom, so I can teach them to my kids!

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I too believe that social security will be there for me (I am 41), but possibly at a less generous payout than what those retiring now receive. This may take the form of increasing the age of full retirement gradually, lowering the cost of living adjustments or maybe even be an across the board reduction in benefits (much less likely). That only focuses on the outflow of SS. Most likely there will be pressure to increase taxes also to improve the income of the program as well. This might be accomplished by increasing the tax rate for SS in employees and employers, but also lifting or eliminating the cap on earnings that are now subjected to SS taxes. The most likely scenario will be some combination in reduction of expected benefits and increase in SS taxes to cover the projected shortfalls in the program.

As you stated this will have an outsized effect on those currently in their early 20’s. As such, more than ever reaching financial independence at a relatively young age will pay even more dividends ever. I personally struggled mightily with tug of war between desire to spend and save in my late 20’s and early 30’s. I finally decided at 33 devote myself to saving. A couple of years later I quit my job and took a year off to reflect. Then started working for myself (for less money than before, but at a much more relaxed pace). Within the next 2 year I plan to hang it up for good and should have financial independence considering my modest lifestyle. Its a great feeling to have this greater sense of control in your life and affairs. Though its not always easy, it is worth it. Best of luck in your journey.

I expect SS to be means tested eventually. That is, it’ll become yet another government program that rewards poor decision making. What I am observing personally is that more and more people are “retiring” earlier than 62 because their lifestyle choices have made them eligible for social security disability.

I think they should raise US SS in increments based on DOB/age.

50-55 = new SS 69

45-49 = new SS 72

40-44 = new 33 75

35-39 = new SS 78

30-34 = new SS 81

And on and on…

I believe this provides plenty of advance warning for people to save. And it should help cut the costs of the program.

That is way too severe and abrupt increase in age of eligibility for social security. First its much more severe than is needed to shore up the program. Secondly its grossly unfair, as it would nearly guarantee many would not draw a dime from it. If your aim is to completely dismantle social security and lose all political support for it, then this would certainly be effective in that aim. I believe that most would not wish such an outcome. The simple truth of the matter is that the finances of social security are not as bad as many would lead you to believe. A combination of adjustment to the cost of living formula and raising the cap on which income is subjected to payroll tax would completely close the funding gap and keep social security solvent for the foreseeable future.

Unfair? People who are about 10 years away have notice to save a bit more. All other groups get a significant amount of time to change their plans, knowing they’ll need to work a bit longer.

Getting free cash at 65/67 is a bit outlandish in an age where most people are living well into their 70s. It wasn’t designed to support all the Boomers for a decade plus. But they’re all standing there with their hands out. As if it’s owed to them. They barely put anything in but they expect a big ROI.

I’m 40, been paying into SS for over 20 years. Do not have a single problem with them saying SS won’t be ready for me for another 35 years. If I want to retire early, I do so on my dime. And that’s just the way it is.

Why? Because some of us have to be responsible and fix the problems the previous generation(boomers) created. So while they lived it up off the work of their parents and pretty much ran it all into the ground, those of us still working (X and Millennials) will have to support them. But we can at least prepare for the inevitable: it won’t be there for us.

If you noticed in the chart embedded in the article, the expected return on taxes paid is negative for a 40 year old today even if SS stays the same as it is now. How is that expecting a big ROI while barely putting anything in. FICA taxes total 15.3% for employee and employer. Self employed people have to cover the entire amount. That is a substantial sum paid into SS over a working life time. As a result it is entirely fair to expect a return on that contribution to the system. Fortunately there is no need to impose draconian cuts in order to keep SS solvent, which was my main point in the comment. As to your suggestion that it would be wise to set aside additional money for retirement, I wholeheartedly agree. This does not mean that its inevitable that SS will not be there for us. Plan for the worse and hope for the best, that is a prudent course of action. Here’s hoping you the best.

Life expectancy, as per wikapedia, for a resident of the US is 79.8, why would anyone pay into something that they are not expected to ever be able to see for another possible 50 years of their lives based on what you proposed? Doesn’t seem well thought out, as this would be a direct revolt against the system, which will result at best in a total overhaul in how the program works and more likely the end of the pyramid scheme that is social security.

John mentioned pretty much everything I wanted to say when I read your post. If I have to wait till 80 to draw from SS, then I say privatize it and give me my money. I can do a lot better on my own and sleep better at night instead of planning things out on my own now thinking SS won’t be there when my generation gets to that age. The fact that people are living longer doesn’t mean the quality of life, or health for that matter, is great. I’ve seen 65year old patients whose medical history span more than a page. I’ve seen 80y.o people who’ve had one issue after another since turning 70. There’s a lady at my giant’s who i’m sure is older than 65 and looks so frail and yet she works. I have a feeling she’s working out of necessity. I certainly do not want to work till 80. I’ve been in the workforce since age 19 and been paying into it since that time. I saw a 23y.o patient just last week who was on SSI and in her case, my heart went out to her because it was a result of medical necessity. why should some who barely pay into SS get the freedom of drawing waay earlier when those who support are penalized. Imagine telling the 19y.o nurse now that they have to work till 80 before retiring. I mean the patient population these days is killing backs. Would you expect a 75y.o nurse to lift a 600lb 34y.o.

With the system you suggested, someone in my age group would probably have to withdraw at 90. More people are living longer but not everyone is living longer. At that age, the probability of never drawing or drawing for a few years only is high. If that ever becomes the case, Why would i want to pay into it for that long?

I actually believe that young people have a higher chance of dying earlier than their parents. Very few will live to 100 in the future because of all the bad lifestyles and chemicals ruining our health, also poor quality healthcare. An example of this is that so many people are claiming disability at an earlier age. Health care innovations can only do so much for people, and I think people wait until it’s too late to make healthier changes in their lifestyles.

Should ease the strain on the retirement side of SS, but the disability fund is gonna feel it hard.

Always my initial impression of moves like this is that it is designed to put the retirement age out of reach so that you die before you can collect, or if you make it to the retirement age you don’t collect for very long.

Interestingly enough, the SSA has analyzed this criticism and posted a response on their website: http://www.ssa.gov/history/lifeexpect.html.

I’ve seen that link as well. But the fact that life expectancy after 65 has increased 20-33% (men vs women) since 1940 is still one reason that SS is struggling. They aren’t trying to “screw” you, but living longer means the math just gets harder to work out without raising the retirement age.