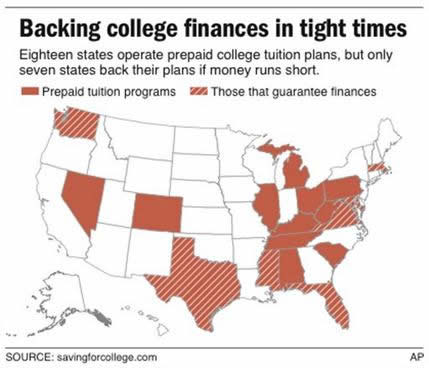

I have thought about signing up for a prepaid tuition plan, as I am leaning towards conservative investments for college savings. Lock-in tuition now, and don’t worry about future hikes. However, it appears that even though 18 states have pre-paid tuition plans, only seven of them actually guarantee them – Florida, Maryland, Massachusetts, Mississippi, Texas, Virginia and Washington. (The image below says six, but the article was corrected later to add Virginia.)

Currently, the plan hurting the most publicly is from Alabama, called the Prepaid Affordable College Tuition Plan (PACT). The plan’s asset value dropped from $899 million in September 2007 to $463 million at the end of January, nearly a 50% drop. Why? Because they invested over 70% of their assets in stocks, and also assumed a consistently high rate of return:

According to an actuarial report on the fund filed by the state in January 2008, the fund’s managers then assumed a rate of return of about 8 percent until 2013, and 8.5 percent after that. That report also found that the fund’s liabilities exceeded its assets by about $20 million.

According to fund documents, 42 percent of its assets, as of March 2008, were invested in large market capitalization domestic stocks, 9 percent in small market capitalization domestic stocks, 21 percent in international stocks, 26 percent in domestic fixed-income securities and 2 percent in cash.

48,000 families who were invested in the plan got letters earlier this month that the plan may have trouble meeting its future obligations. To make things worse, their brochures actually once stated that it was guaranteed by the state of Alabama, until later on it was found that wasn’t possible due to state law.

I don’t know about you, but isn’t a guaranteed return the entire point of prepaid tuition plans? I commit money now in order to know that I can afford tuition for my child in the future. I give up the chance for higher returns elsewhere. Otherwise, it’s like heads they win, tails you lose. High returns, they keep the difference. Low returns, they say “oops we got no money”.

Also reported to be in trouble are the programs in Tennessee, South Carolina, West Virginia and Washington. Finally, I also found this article which stated that although guaranteed, the Texas plan had a projected shortfall of $206 million.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

What is the point of a pre-paid college plan if it is not guaranteed? People should grab their pitchforks and rebel. 🙂

I think If you use the pre-paid tuition 529 plan then you have to use the funds on a college in that state specifically – also, it only covers tuition and room and board is usually ~50% of the price of college.

I would just use the standard 529 plan and invest the money myself then you can use it for tuition, room, and board and your kid can go to any college.

That’s why I do not advise anyone to invest in these 520 plans..Its another financial vehicle cooked up to inflate profits of financial institutions…

I like these plans given the necessarily short time period you are saving for college tuition and the high rate tuition inflation. PA’s (mine) even allows you to use it out-of-state (it just uses a certain inflation factor for whatever category of school attended). It is correct they don’t cover all expenses, so it only serves as a good vehicle up to the amount of expenses it does cover, additional savings needs to go elsewhere.

The only downside to these in my mind has always been the disclaimer that the money is guaranteed by the plan, not the state. People used to always assume the state would stand behind it anyway (kind of like the US standing behind Fannie Maes), but CA has shown that a state may not always have the money to do it.

It is interesting. People are not only guaranteed by the plan a certain return (the rising cost of tuition inflation) but have been sent statements that they’ve already earned “x” number of credits. Now “Unless the market turns around or there is an infusion of cash”, the pyramid will undoubtedly collapse and Madoff will go to jail (oops, just got my ponzi schemes crossed, guess I should rethink this whole pre-paid thing)

Is it possible to sue a state government for fraud? I don’t see how this would be legal if a private enterprise ran this scheme.

I was never crazy about pre-paid 529s — especially if your kids are too young to decide what college they’d like. But I did open a regular 529 – which has also tanked recently.

But just for the sake of argument, if I absolutely knew my kid would go to X College — I’m not sure I would have trusted these plans in the first place. I’ve often found that once you’ve paid for something, very few people will be interested in dealing with you. I know, this is higher education, but money is money. They already made their sale to you — your problems will be on the bottom of their “to do” list.

Prepaying for stuff like car insurance, house insurance, or things like that can save you money and you’re also done with them. Your covered, that’s it. But paying up front for services, even when you have a gift-card or certificate for some salon or some restaurant, you are put into an inferior position. Giftcards don’t let the user get additional rebates usually. Certificates at restaurant often not that straightforward (you can tip with the card, or some silly stuff like that). When you come in with new money, everyone seems to treat you better.

So with that philosophy in mind, I would take the funds that would buy pre-paid tuition today and instead invest it as well as possible. Somehow (through my suspicious nature), I feel we will be better treated coming in with money in fist.

You are good. You have taken the words right out of my brain. I couldn’t say it as good as you can. Great comment.

At least in Virginia, the guarantee for the pre-paid plan (VPEP) is not a real guarantee. Each year’s budget gets voted on by the General Assembly to cover any shortfall. They treat pre-paid tuition just like any other contractual obligation of the state. To date they have never voted to not fund the pre-paid plans, but the next couple of years could force them to. I imagine that other states are similar.

To me, the pre-paid 529s are just another “derivative” product that Wall Street came up with. The reality is that more you have in 529s, less you will get for the need-based aid, and this especially true for many private colleges. If you think that 529s are the investment for your kids’ future which is hardly guaranteed, why not investing in your kids’ today? If, with your help, your kids can excel at every stage of their high school life, they will get merit-based scholarship which most of the colleges offer. This could not cause a problem of not being able to use up all the funds in your 529s unless you or your turn down the scholarship…

Just one thing to say…CASH is KING!

I was worried about Illinois’ prepaid college plan. As of February 28, 2009 the fiscal year-to-date drop was 26% and monthly was about 5%. I think it is a manageable shortfall that the legislature can cover if necessary.

Is there anyone out there who has used a state prepaid 529 plan and liked it? I’m an Illinois resident and am thinking about participating in our state’s plan.

I am young enough (31) that I benefited from Florida prepaid. My father had it for 3 of the 5 children (the other two were already in school). Because I had merit scholarships anyway (the only one to have those, though, they’re very competitive and not so easy to get, especially when most parents are “helping” their kids through school, it sort of tips the scales a bit), I had a check that I put towards all other expenses.

We’ve taken a contract out for my eldest daughter’s tuition, it was back in 2002. At that point, it covered a year of dormitory and 4 years of tuition for about $14,000. We paid about $200 a month for 55 months. It was “guaranteed”. At the time she was 1 year old and we could’ve opted to do some ridiculously low payment until she was in college (17 years later) of around $35/month. We decided to save a little in finance charges and pay it off in five years. She is the only one (of 5) provided for, so far. Just 3 years later, when our first set of twins came along, the plan was up to almost $400/month, and times two, we didn’t feel we could suck it up and delayed. Now Florida has tuition differential plans, local fee plans, dormitory plans, etc. And it does apply to any accredited school, in-state or out-of-state. If the plan is applied to an out of state school, the beneficiary will receive the amount that would’ve been paid to a Florida school, and admittedly, Florida Colleges and Universities are incredibly inexpensive. The grandparents (if residents) can set up a plan for their grandchildren, and we liked the guarantee. Still, we figure we’ll supplement with another 529 plan, but if nothing else, we feel eased by the fact that our child has several paid-for options in Florida, no matter what our future financial situation, and if we can do more than that, i.e. a plan to cover private schools, out of state, etc. than that’s bonus. Nice to have, but not strictly necessary.

THEN that’s bonus. Sorry. Those typos always bug me!

I am on the fence on this and don’t know what to do. We opened a plan for our son early this year under the Texas Tuition Promise Fund. I really want to close it, but keep thinking I should ride this out since my son is only 2 and we still have a long time before he goes off to college. The thing is, our plan is only “guaranteed” if he’s either…

a. three years away from graduating

b. accepted to a college

c. enrolled in school already..

If the plan goes kaput before either of these things, we’ll only get back what we’ve put in, “minus any administrative fees or other losses due to the market”. That last bit is what is really freaking me out. But the 7% a year increase also has me worried since by the time he goes to school it means we’ll pay some CRAZY amount!!

I have to say I am disappointed so far with the Md 529. Setting it up was difficult with a lot of dead links. For example you’d click on a link for more information and get a page not found. Clicking back or clicking on get more info links during the registration process would delete ALL information you already put in. And there are stupid things like they show you detail info for the various funds you can invest in only at the very beginning. Tens of minutes and several pages later you are asked to indicate what funds you want to invest in, but they provide no information about the funds on that page, just the names of the funds, so if you didn’t jot it down, you have back all they way to the beginning to get the fund detail and guess what? This deletes your whole application and you have to start all over again. I must have filled out the whole application 5 times over.

The initial amount was never deducted from my checking so I need to call them to figure out what is going on.

I’m doing this to get the tax break and will keep the investment to absolute amount required to get max tax benefit but no more than that. I don’t trust the adminstration of it. It is clear the quality of the product is what you’d expect a government bureacracy to produce. T Rowe is underwriting but I’m guessing they do not do the adminstration of it unfortunately. I’m sure it is safe but be careful of administrative goofs.

If this didn’t have a state tax benefit associated with it, it would be broke the first day.