The strategy of Buy & Hold Investing has a lot of followers (including me), and one of it’s touted benefits is that it is a simple way to invest. In the case of passive investors, it primarily involves picking and maintaining an asset allocation plan for the next 10-50 years of your life. No need to monitor stock prices or decipher financial statements. However, “simple” and “easy to execute” aren’t the same thing. For example, “spend less than you earn” is simple. “Always save for a rainy day” is simple. But how many people actually do this?

So why don’t I think it will be easy?

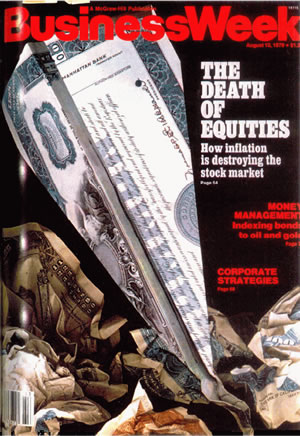

The picture above is the cover of the August 1979 issue of BusinessWeek magazine. In case you can’t make it out, the picture is of a stock certificate folded into a paper airplane that has crashed, surrounded by many other crumpled airplanes. (No Photoshop back then…)

The title of the cover story is “The death of equities: How inflation is destroying the stock market.” I haven’t been able to find the full text of the article noted, but I did find some snippets at TheFiendBear. He notes that the article “was published at a time when the Dow was languishing at 875 and had been trading in a see-saw fashion ever since topping out 6 1/2 years earlier in January of 1973. Inflation was a persistent nag on the economy and the Federal Reserve and US fiscal policies were held in low regard.”

Sound familiar? Now here are excerpts from the actual 1979 BusinessWeek article. Here is the summary:

The masses long ago switched from stocks to investments having higher yields and more protection from inflation. Now the pension funds–the market’s last hope–have won permission to quit stocks and bonds for real estate, futures, gold, and even diamonds. The death of equities looks like an almost permanent condition–reversable someday, but not soon.

Pension funds invested in diamonds? Wow. But stocks always beat bonds over long periods, right?

Until now, the flight of institutional money from the financial markets has been merely a trickle. But it could turn into a torrent if this year’s 60% increase in oil prices touches off a deep recession while pushing inflation sky-high. As it is, the nation’s financial markets and its capital flows have been grossly distorted by 13 years of inflation. Before inflation took hold in the late 1960s, the total return on stocks had averaged 9% a year for more than 40 years, while AAA bonds–infinitely safer–rarely paid more than 4%. Today the situation has reversed, with bonds yielding up to 11% and stocks averaging a return of less than 3% throughout the decade.

Still, I thought stocks were a great inflation hedge?

The one rule whose demise did the stock market in could be summed up thus: By buying stocks, investors could beat inflation. Stocks were a reasonable hedge when inflation was low. But they proved helpless against this awesome inflation of the past decade. “People no longer think of stocks as an inflation hedge, and based on experience, that’s a reasonable conclusion for them to have reached,” says Richard Cohn,an associate professor of finance at the University of Illinois. Indeed, since 1968, according to a study by Salomon of Salomon Bros., stocks have appreciated by a disappointing compound annual rate of 3.1%, while the consumer price index has surged by 6.5%. By contrast, gold grew by an incredible 19.4%, diamonds by 11.8%, and single-family housing by 9.6%.

This isn’t to bash BusinessWeek, they were certainly not alone. Of course, since 1979 the U.S. stock market has had an awesome run, and now we are back to many people putting 100% of their portfolios into equities. But I am pretty sure that some time within the next 20-40 years there will be a similar fearful atmosphere. Imagine bonds outperforming stocks by 8% per year, for 10 years. Imagine very smart people, pension funds, moving their money as well.

Imagine this article being written 40 years later (replace 1979 with 2019, late 1960s with late 2000s), after all these crazy Fed cuts, money injections, and high oil prices spike inflation. Just something to consider. Will you still be able to buy and hold? I’d like to envision myself being a pillar of steadiness in that storm. 😀

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I agree with the Buy & Hold strategy, especially when the stocks that are bought are essentially good companies — run by fundamentally good management.

HOWEVER,

I am seriously concerned with how certain economic pressures will affect the US stock markets in the future. Stock pricing is purely affected by supply/demand. Supply has to do with the number of shares outstanding on all of the markets (tradeable shares), while Demand for stocks has many factors. Here are some situations that might have MAJOR affects (or is that ‘effects’, i always confuse the two) on the markets:

1. The huge baby boom retirement. Pensions, just like the Social Security & Medicare funds are grossly underfunded. They were already underfunded before the huge escalation in medical costs over the past 10 years. As the Baby Boomers retire, these pension accounts will be drawing down their holdings as they make their distributions. I don’t have numbers to back up my theory but my guess is that most pension plans have already been closed off to new entrants (plan members), so that there’s no new funding…basically, most of the money in the plans now come from investments. These pensions will be making substantial distributions in the coming years so at some point, the pension well will run dry if there are no serious changes to our current retirement system. This will have a major effect on demand.

2. The world is flat. The SEC is already taking steps to make trading in the US more accessible to people located outside the US. They MUST do this because it’s much easier now to take money out of the US market to dabble in foreign investments, so the competition has increased significantly and US is competing for money that is now being spread around the world. This is playing out right now, and this is another factor that reduces the demand.

3. People aren’t saving enough on their own. I hear all the time that the majority of Americans work for a small business. As an auditor who audits small companies, and also as a tax preparer, one thing i see repeatedly is that people aren’t saving for retirement. As Jonathan said, “‘simple’ and ‘easy to execute’ aren’t the same thing”. If we polled the owners of 10,000 small business spread out geographically across the U.S., i bet less than 50% of the businesses could claim that at least 50% of their employees contribute at least 5% of their salary to a retirement plan. If this is true, then less than 2,500 of the workforce of 10,000 polled is saving even 5%, not that 5% would even be enough. This is another significant demand pressure.

So, if there aren’t enough people putting money into stocks for their retirement and for general investing, where will the demand for the stocks come from? Shrinking supply? Foreign investment in the US? Who knows…

Phoenix, you’re right that there is a lot of uncertainty ahead, just as there was in 1979… I think that’s part of the point. Have you read Jeremy Siegel’s projection that if baby boomers were all to liquidate their stock assets the stock market would decline by 51%?

But every coin has two sides and if demand reduces and supply remains the same that will drive prices down which, if you remember basic economics, will drive demand back up until the two are in equilibrium.

I don’t think it will be the mass hysteria that some predict with the baby boomers because they haven’t saved enough and the only solution is that they will have to work longer. Ultimately, real stock prices are not driven by how many outstanding shares there are but by the health of the economy. And it is better for the economy if we have more workers contributing towards our productivity as a nation.

My entire view on the thing is that right now, things are low and they will stay low for a while. Seeing as I am young(er) this is a great thing for me. If I can buy as much as possible while the market is down, I will be in really good shape 30 years from now which will be perfect timing.

I’m with Jesse. I’m actually secretly hoping for high inflation in the next decade. Why? I just bought a house with a fixed rate mortgage, which is gold in a high inflation environment. Conversely since I’m just starting, I have relatively little in my retirement accounts. So if in the coming decade we have high inflation and low/negative stock returns, that’s just perfect for me so I can buy as much as I can while the market is low.

Gotta say Rick and Jesse have the right perspective. The Millenial generation is just now getting into the workforce. This means it will be about 10 years before the full effect of their retirement purchases start to take hold. So if you can purchase equities, now is the time. As the boomers leave they will move to very stable investments like bonds. This will cause the bond market to boom (meaning up to 9%). The movement out of stocks will create a decrease of demand and thus a lowering of price.

This happens when you have a large generatoin followed by a smaller one (boomers to Xers). Now, what happened in the 70’s was the WWII generation began retiring the generation after them (called the silent generation) was very small. The Boomers were just entering the work force in mass and were not contributing to the purchase of equities. So we got a gap. Looks like we may be headed there again with the boomers followed by the Xers followed by a large generation; the millenials.

I don’t think the market is going to crash but it will probably level off for some time. Once the millenials are all out of college is when it will probably take off again. That being said we can be getting everything cheap for the next 5-10 years.

Actually it could be argued that a similar article appeared on the WSJ on March 26 ” Stocks Tarnished by a lost Decade”

http://online.wsj.com/article/SB120649226977964203.html

This author believes that the above article from WSJ actually marks a bottom in stocks.

http://seekingalpha.com/article/70508-spy-the-case-for-a-bottom-being-in-place

Like Rick and Jesse, I’m actually a little excited by the coming years. I’ve upped the contribution to my Roth IRA ahead of my original schedule (next year should hit my goal of maximum contribution), just to take advantage of the current climate.

While execution, of course, remains an issue for many, I find that it helps to look out for companies with solid fundamentals. I look at where they put their investments (no financial companies investing in CDOs for me!) and decide whether or not the companies are likely to survive the downturn. And I like index funds. They may not offer sexy returns, but they are normally fairly solid.

This is truly a great time to be a homebuyer, as long as you remember to lock in the mortage at the prevailing fixed rate.

If, as many pundits predict, we are headed for a period of mega-inflation, you will be able to pay off your entire mortgage with soon-to-be worthless dollar bills.

Not a bad trade, a few hundred thosand pieces of meaningless paper in exchange for a house which has tangible value.

I never understood the ‘Buy & Hold’ strategy. I am new to stocks.

So how does one realize a profit? It would be terrible to see a stock which we bought cheaper, to shoot up to stratosphere, and settle back to old levels or even lower.

I initially planned to hold “V” forever (got in at $55.5) – now thinking of selling at $70… then buy more when it inevitably drops down.

If it doesnt drop down, then buy more at $72+ – would have lost only $2, but ‘locked’ my $15 profit. And even it drops to $60, I would have lost -$12, but only from my profit of $15.

But if it does drop down to say $60, buy more, as I now have realized “$15” profit (sold at $70).

(assuming i am always gonna pay short term capital gains)

“John Says:

April 10th, 2008 at 3:26 pm

This is truly a great time to be a homebuyer, as long as you remember to lock in the mortage at the prevailing fixed rate.

If, as many pundits predict, we are headed for a period of mega-inflation, you will be able to pay off your entire mortgage with soon-to-be worthless”

John, now is a truly terrible time to buy a house. Housing values will continue to decrease over the next several years, in many areas by double digits, leaving your new home worthless (negitive equity) for several years after that. And those worthless dollars of yours may be very dear to you if your salary does not keep pace with inflation as many have not in the last decade, and that’s if you manage to keep your job. I suppose if it gets really bad the government will just bail you out anyway, but I wouldn’t stake my future on it.

I hate to say it, but I actually wouldn’t mind having my mortgage be nullified with some high inflation either. I just have to keep believing that businesses (and thus stocks) will create value above inflation.

I agree with buy and hold but think this can’t be like ron popil and set it and forget it. I thik you have to take an active role occasionally as markets are going to be changing a lot in the future.

On another note, have you ever heard of couchsurfing? its a good way to save money when you do your big trip. meet locals and not pay for accomadation. check it out. I also reviewed it on my website in case you ever stop by..

“Ram”,

The idea of buy and hold is that you can’t time the market, but that stocks in general go up. I too hold “V”, but who knows if it will go up or down. You say you will sell at $70. But maybe it will never reach $70. (Consider BX, which many people thought would also shoot up, but has instead lost nearly 50% of its value). Then you say you will buy more when it goes down. Maybe it does reach $70, and never looks back. You will then miss out on a lot of gains.

The prevailing strategy is to buy diversified index funds and hold them for 40 years or so until retirement. Most people expect the stock market in general to gain 6-8% annually in the long term future. That is what buy-and-hold is all about.

I’m sure I’ll be quite morose to see nothing happening with our portfolio over the next few years, but we’ll continue to add to our 401k plans in diversified value and international funds and hope that they eventually get their day again. A house purchase is in our future within the next two years as well.

“joelkton”:

You have to remember that not everyone lives in California or Florida. In many places in this country housing prices are stable, or are only dropping very slightly. It may not be the best time to buy in California, but in many places, it’s just fine to buy a house now.

Adding on to Rick’s comments, there are real estate markets that appear to be somewhat recession-agnostic. For example, in a market that I have to believe is NOT unique throughout the entire country, there is a realtor blogging that waterfront single family homes have appreciated approximately 17% per year for the last 5 years. While I might not have guessed 85% over the last 5 years, I might have guessed 40% to 50%. This market is the Lake of the Ozarks in Missouri. Now, I don’t know anything about other regional destinations, but, at least at LOTO, I don’t see much effect of a declining housing market. And, it is hard for me to believe that the LOTO market is a unique anomaly in the U.S.. (In the interest of full disclosure, my family owns property at LOTO, but just for personal use).

Geez – you stole the exact post I was going to write on the same article!! Oh well – I’ll just write it anyways.. 🙂

With respect to the high inflation / fixed mortgage rate dream scenario – keep in mind this will mean reduced house prices.

Mike

I have been investing since before 1979.

“Investor sentiment” is now about as negative towards stocks as i have ever seen it.

However the fundamentals are not nearly as bad as in 1980-1981, or even 1987.

Blood is in the streets and fear is rampant. It is always best to buy when it feels like the hardest thing to do. If you wait until it feels safe to buy, the prices will be much higher. My advice now: “buy,buy,buy”.

That’s the beauty of buy and hold, it weathers the storm of decades. Pension funds, mutual funds, hedge funds, will always be chasing the market. If you spent 40 hours a week with your face to a stock ticker, you’d shift funds around too.

The beauty of diversification is you never have to worry about what’s popular. A bit in bonds, real estate, commodities, hedge funds, domestic stocks, international stocks and everything in between allows you to ride any wave. As bonds get more popular, the proportion of your portfolio will grow. Sell of the growth and redistribute into the segment that has lagged. Whatever segment is lagging would be selling at a discount, like domestic equities and real estate right now.

Great lookback article, I love these.

Buy & Hold no longer works, because even “blue chips” can plummet. As an engineer, you can leverage some of those skills to do a little analytical work. I suggest:

1. Read Rule#1 by Phil Town and learn how to do both the analysis, evaluation, and the on-line MACD using Yahoo or MSDN.

2. If you are a reader, also read the Intelligent Investor by Ben Graham, mentor of Warren Buffet – #1 investor in the world. The change – according to Buffet – is that today you need to evaluate management and watch what the institutions are doing.

3. Listen to Jim Cramer, if you have access to cable. You will learn a lot by listening, but don’t drink his KoolAid. He has access to knowledge that the rest of us don’t have. I like ot think of him as being the Rush Limbaugh of investing. Opinionated, not necessarily correct, but always a source of new information.

4. Max out your 401K

5. Max out a Roth IRA

6. Do an automatic paycheck deduction of 10% – 20% into a conservative growth or value mutual fund that includes a distribution twice a year.

7. If you can achieve 15% growth per year, the principle will double about every 5 years. So, if you start with just $125K today, in 15 years you will have $1M… and adjust accordingly.

Good Luck.