When looking at your investment returns, it’s important to calculate your return after the impact of taxes and expenses (management fees, commissions, bid/ask spreads). That number is what you really end up with, but it’s never shown on any year-end statements. ETF provider iShares put out a Managing Tax Challenges brochure that shows the average annualized tax cost for actively-managed mutual funds over the last 10 years. Via Abnormal Returns and Mebane Faber.

(Click to enlarge)

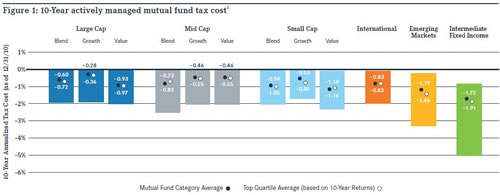

Many actively managed mutual fund managers have had difficulty delivering benchmark-beating, after-tax returns. Figure 1 shows the 10-year average tax cost for active funds and top quartile active funds. What’s striking is that in every case except for mid cap blend and small cap value, top quartile funds’ tax costs (as indicated with a white dot) were equal to or greater than those of the category average (black dot). Even worse, after taking taxes and fees into consideration, the average active fund underperformed its benchmark.

The takeaway is that expenses and tax-efficiency both matter greatly to the bottom line, and passively-managed ETFs are much more tax-efficient than actively-managed mutual funds, possibly enough to counter the performance benefit of active management. For one, being passively-managed on its own means lower turnover (less buying and selling) and thus less taxable events. Second, the ETF structure itself has inherent advantages over open-ended mutual funds. Neither of these traits are specific to iShares, by the way, although they do have some of the most popular index ETFs out there.

I should note that many Vanguard ETFs are simply different share classes of open-ended mutual funds (Example: VTI and VTSMX). Theoretically, this extends the tax-advantages of ETFs to the mutual fund shareholders, as described in Vanguard’s ETF brochure:

Tax advantage. Like other ETF providers, Vanguard can push low-cost-basis shares out of the portfolio through the in-kind redemption process. Our patented share-class system provides an additional benefit. To meet cash redemption requests from non-ETF shareholders, Vanguard can sell high-cost-basis securities to generate a capital loss. These losses offset any current taxable gains and, if not exhausted, can be carried forward to offset future capital gains—a recycling that is not likely within stand-alone ETFs. Theoretically, cash redemptions could trigger a gain instead of a loss; however, Vanguard’s deep tax-lot structure has allowed us to select high-costbasis shares in both good markets and bad, resulting in a high degree of tax efficiency.

As a result, in many cases if I can own Admiral shares of Vanguard index funds that have the same low expenses as the ETF version, I’d rather just own the mutual fund version for the sake of simplicity. For instance, I like making dollar-based transactions at net-asset value (NAV) instead of having to place a market order (potential loss due to bid/ask spread) and also worrying about NAV discount/premiums. It also keeps me from doing silly things like trying to time the market intraday.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

The key words of this entire post are: “…IF I can own ADMIRAL shares…” It’s a lot like saying: If I had the capacity to own a Ferrari, I’d rather own the automatic version than one with the lower-costing manual transmission, just for the sake of simplifying my everyday drive. I wouldn’t have to worry about getting the cheapest car insurance or doing silly things like haggling with the car salesman. Yes, I have to admit, we poor people worry and do silly things.

@Ron The Vanguard 500 Index Fund Admiral Shares (VFIAX) only has a $10,000 minimum. The Admiral shares used to be in the “Ferrari” category, but they recently came down to a level that most working folks can reach in a few years.

@Ron – Umm… okay, really not sure where all that came from? As Shannon noted, admiral shares of virtually all the index funds have a $10k minimum. That’s more like Honda CRV or Toyota Camry money, and besides, I drive a 10-year old Pontiac. 🙂 Otherwise, passive ETFs are perfectly acceptable. I currently hold VWO, VXUS, and TIP.

Is tax efficiency of important with tax-advantaged vehicles such as IRA’s, 401K’s, etc.? I’m a bit confused about this. Or does it affect returns regardless. We have a mix of active and passive funds (all in IRA’s) in Fidelity and Vanguard. Thanks for the discussion.

Charles: no, not relevant for tax-sheltered accounts.

@Charles – If all your investments are in tax-deferred accounts, then you don’t have to worry about tax-efficiency for the most part. High amounts of turnover may result in high transactional costs that may harm performance slightly, as even mutual funds have to pay for trades and deal with bid/ask spreads, especially if they are big and have to make large trades.

Thanks all. This is what I thought but wanted to make sure. Related but probably for another day (perhaps you have covered this) is the topic of the appropriate mix of tax-deferred (e.g. 401K), Roth, and regular (non-Roth) investments. I recently read that this kind of mix is useful in retirement as one can draw from different accounts to stay in lower tax brackets.

“What’s striking is that in every case except for mid cap blend and small cap value, top quartile funds’ tax costs (as indicated with a white dot) were equal to or greater than those of the category average (black dot).”

I think this is what one would expect since the top quartile funds would have made more money in the first place. As the top quartile funds exited their positions, one would expect that on average, they had larger gains, and hence higher taxes. This also explains why the best performing equity class (emerging markets) shows the highest tax cost. As profitable postions were sold, taxable gains were incurred.

I would be interested to see the data presented somewhat differently: after tax return to pretax return ratio.

My second post here, so please forgive me if I’ve misread the chart, but I think I am understanding it correctly.

I’m 33 and recently inherited about $350k and was wondering what to do with it from an investment perspective. I already have Roth and “regular” mutual fund accounts with Vanguard. I’m married, but don’t have any children yet (hopefully soon though).

Thanks for any input.