LendingClub (LC) is a marketplace lender that offers unsecured personal loans and then sells investment notes backed by those loans. After defaults and fees, they advertise historical returns between 5% and 8%. As an incentive, LC recently started offering up to 100,000 United MileagePlus award miles to investors that bring in at least $2,500 in new money. Here I offer a quick analysis of the investor offer and point out that it is actually available to both new and existing investors, even though that may not be obvious from the website.

Highlights.

- Offer only valid for taxable Lending Club accounts. (IRAs are not eligible.)

- Only deposited and invested dollars are eligible for award miles.

- Lending Club Investor must have UA MileagePlus account activated before investing to qualify. New investors can link online. Existing investors must call or e-mail to manually link your accounts (see below).

- For existing investors to receive miles, an investor must transfer at least $2,500 of New Funds into an active eligible taxable account and invest the New Funds through the Lending Club platform within 90 days of the commencement of the then-current offer (each, an “Existing Investor Offer Period”).

- Offer is valid from October 1, 2016 to December 31, 2016 and Mileage Plus miles will only be awarded on new funds transferred and invested through Lending Club during this time period.

Selected quoted text from the landing page:

We’re excited to announce our partnership with United Airlines! Investing on Lending Club just got more rewarding. Right now, receive one United MileagePlus® award mile for every two dollars you invest through Lending Club up to 100,000 miles!

[…] Upon the transfer and investment of the first $2,500 of New Funds, a new investor will qualify to receive 1,250 miles. For every dollar of New Funds transferred and invested in excess of $2,500, a new investor will qualify to receive .5 miles, up to a maximum aggregate bonus of 100,000 miles per calendar year.

The maths. A minimum deposit of $2,500 earns 1,250 United miles. Every dollar above that $2,500 will earn 0.5 miles up to the 100,000 mile limit. If you value United miles at range of 1 cent to 2 cents a mile, 1,250 miles is worth $12.50 to $25. Thus, the bonus value ranges from a 0.5% to 1% bonus on top of the interest you’d already receive.

Existing investors participation details. I confirmed with two different LendingClub representatives that this offer is also available to previous/existing investors. You must first link your United MileagePlus account number with your account. You can contact them via e-mail at EarnMiles@lendingclub.com or phone at 888-596-3159 (7:00am–5:00pm PST, M–F). Provide them with your LC account ID and your UA MileagepPlus Number.

Bottom line. The bonus itself is not big enough to encourage you to invest if you weren’t otherwise interested. However, if you have already decided to invest with LendingClub, definitely don’t miss out on these free miles to boost your overall return. The value is roughly 0.5% to 1% to your investment amount, assuming you bring in at least $2,500 of new money. Link your accounts first before moving over the new money.

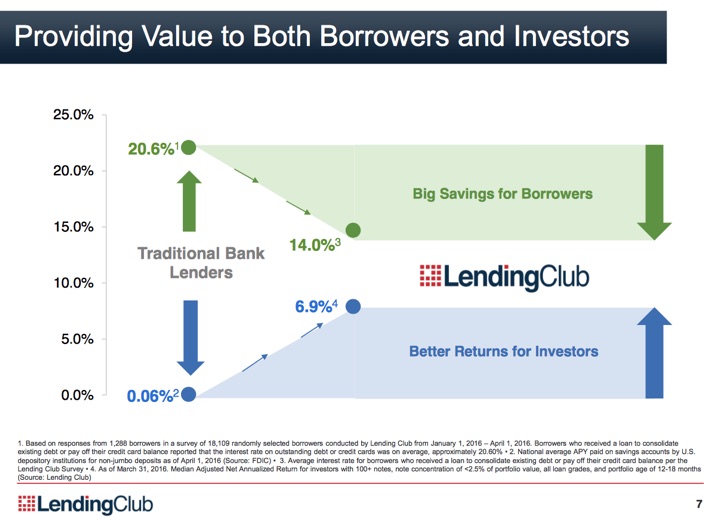

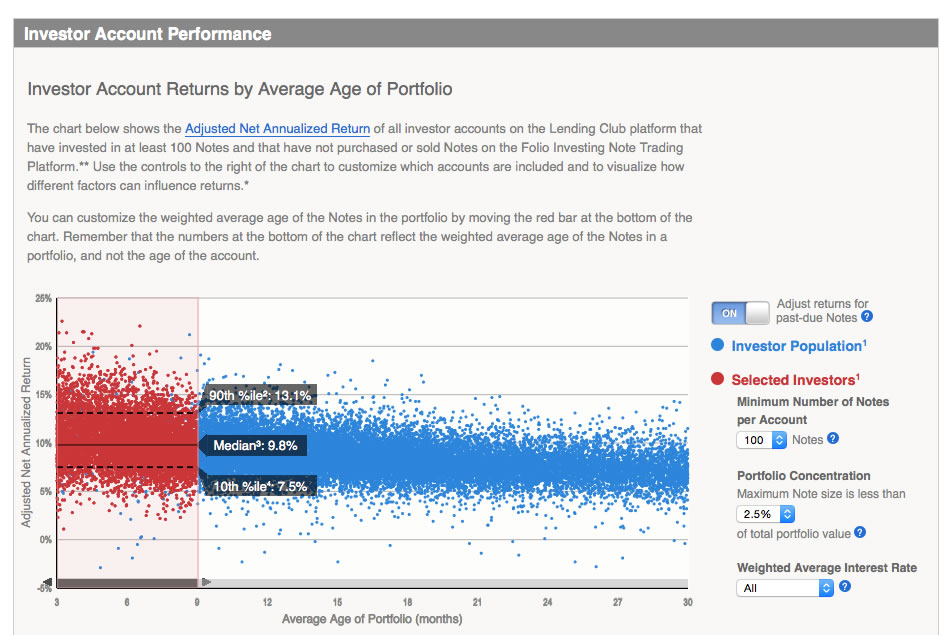

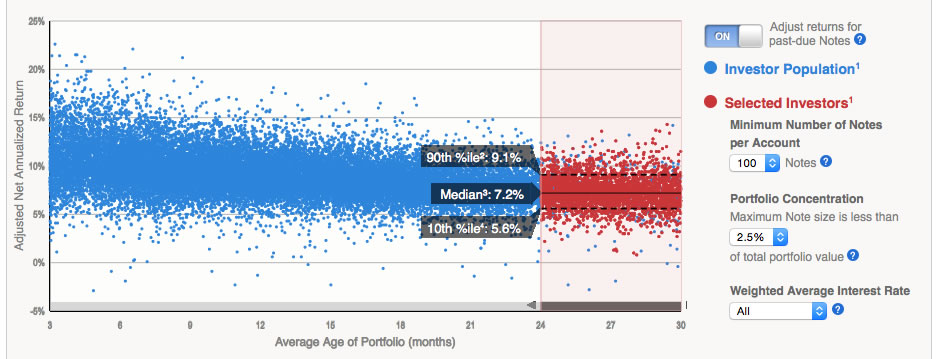

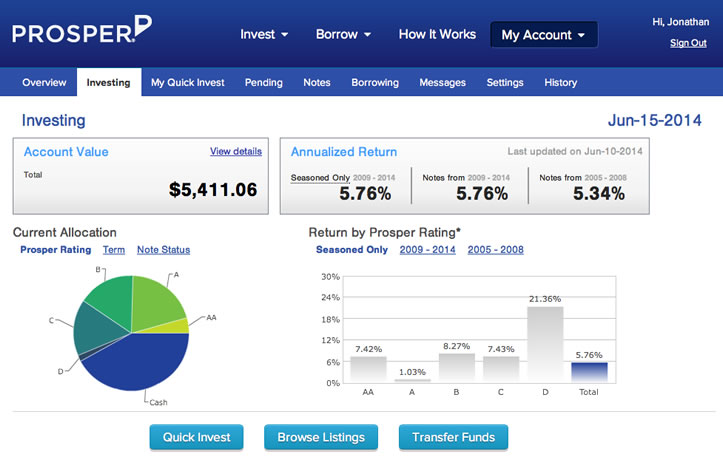

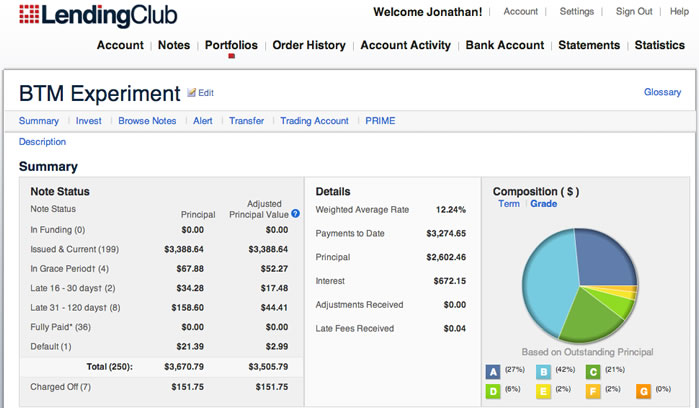

As an existing investor myself, I’ve written my share of opinions on LendingClub. I’ll just say two things: Have realistic expectations and diversify. Their advertised historical returns of between 5% and 8% are more realistic than you may have seen elsewhere. As they also note, 99.8% of investors who invest in 100+ Notes of relatively equal size have seen positive returns. It is not coincidence that 100 notes x $25 each = $2,500.

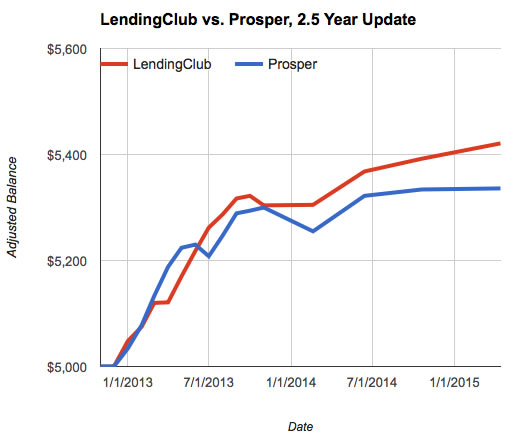

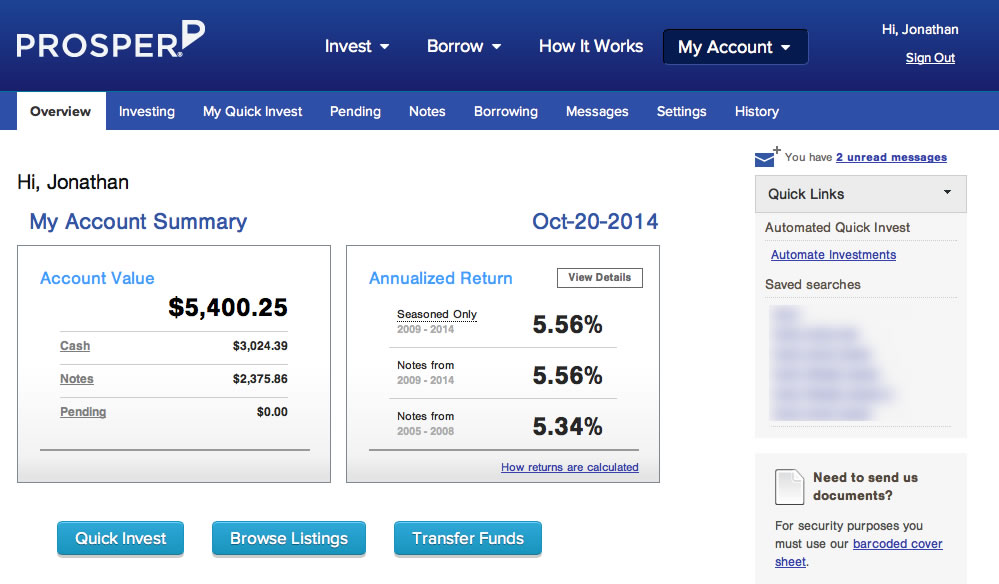

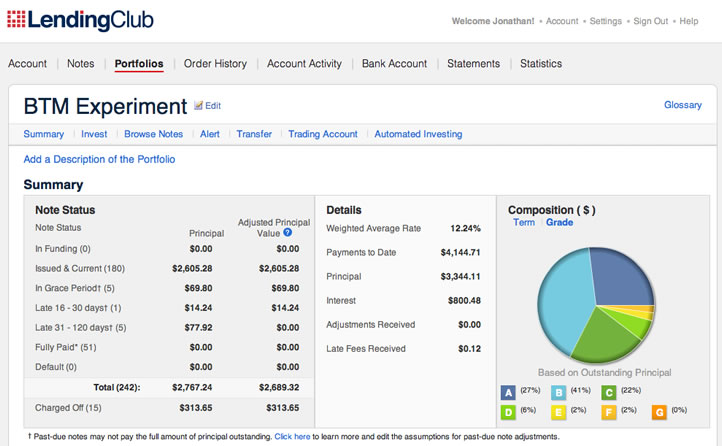

In November 2012, I invested $10,000 into person-to-person loans split evenly between

In November 2012, I invested $10,000 into person-to-person loans split evenly between

After posting the 1-year update (

After posting the 1-year update (

Yesterday, I posted a

Yesterday, I posted a  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)