Here are a couple of quick Amazon promotions before I sign off for the weekend:

Here are a couple of quick Amazon promotions before I sign off for the weekend:

Amazon Warehouse Deals $10 off $50. Get $10 off a $50+ purchase at Amazon Warehouse with coupon code EARTH10. This is where Amazon sells their open-box and pre-owned products. Basically, stuff other people returned. I’ve bought a few things without issue.

Here’s a link to the Kitchen goods and Electronics sections. Offer expires at 11:59 p.m. (PT) 4/22/2017. Offer only applies to products sold by “Amazon Warehouse Deals.”

Amazon Student $15 off $40. Have a .edu e-mail address? Sign up for a free 6-month trial of Amazon Student and get a $15 off $40 coupon with the promo code PRIMESTUDENT. How to redeem the offer by 4/16:

1. Log in to your Amazon account.

2. Select at least $40 in products (but not digital content) sold by Amazon.com or Amazon Digital Services LLC, not sold by a third-party seller or other Amazon entity (look for “sold by Amazon.com” or “sold by Amazon Digital Services LLC” on the product detail page), and place the products in your Shopping Cart.

3. Enter the code “PRIMESTUDENT” at checkout in the “Add a gift card or promotion code” field.

4. The $15 discount will then be applied.

Amazon Prime Student gets you the free 2-day fast shipping, video streaming catalog, and other exclusive discounts. After the trial ends, you get 50% off the full Prime membership cost for four years or until you graduate, whichever comes first. If you qualify, it’s worth signing up.

Alexa $5 promo code with $25 gift card purchase. Get a $5 promo code if you order a $25 gift card through Alexa. Also, get another $5 promo code when you re-order a previous purchase via Alexa. You can use Alexa through Fire TV and other devices now.

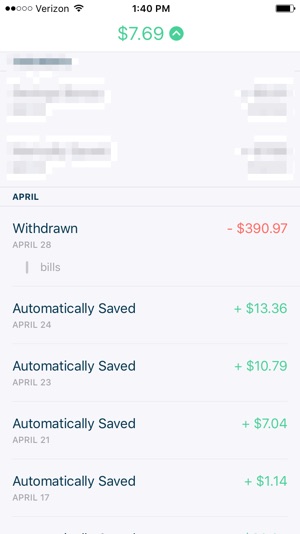

Financial chatbot Trim has a new feature called

Financial chatbot Trim has a new feature called

Update – This offer is now EXPIRED.

Update – This offer is now EXPIRED. If you don’t understand why having a fiduciary requirement matters in terms of financial advice, read this

If you don’t understand why having a fiduciary requirement matters in terms of financial advice, read this  Updated with new deal. If you are still looking for downloadable desktop tax software that doesn’t require your Social Security Number and financial details to be stored in the cloud, here’s a limited-time deal on H&R Block Tax Software 2016.

Updated with new deal. If you are still looking for downloadable desktop tax software that doesn’t require your Social Security Number and financial details to be stored in the cloud, here’s a limited-time deal on H&R Block Tax Software 2016.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)