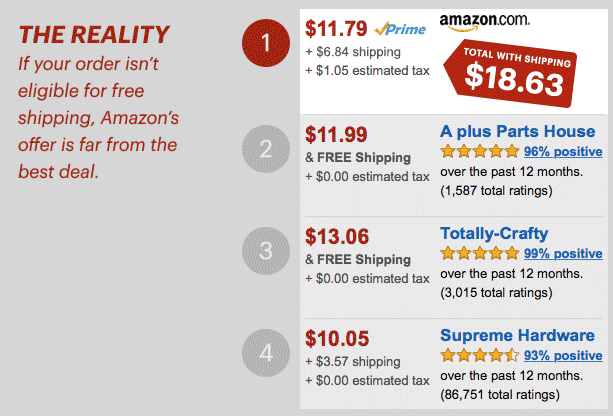

ProPublica has a new article Amazon Says It Puts Customers First. But Its Pricing Algorithm Doesn’t, which outlines how Amazon does not always list the lowest price including shipping as the first available option. Here’s an example they provide of how this works on some pruning shears if you don’t have Amazon Prime or reach the $49 Super Saver Shipping tier:

Amazon really, really wants everyone to buy Amazon Prime. They do all kinds of little nudges to get you to join. For example, their Super Saver Shipping option went from a few days to oftentimes weeks to get to me. Another way they promote Amazon Prime is by promoting merchants that join their Fulfilled by Amazon (FBA) program, because that means customers can buy more stuff with Prime. ProPublica points out that Amazon used to be more blunt about it with this former language:

Because most FBA listings are ranked without a shipping cost, you get an edge when competing!

Bottom line: If you don’t have Prime and don’t qualify for Super Saver Shipping, the default buying option will often not be the cheapest. By using the term “algorithm”, that suggests to me some sort of complicated scheme. What Amazon does is simple but perhaps deceptive: They assume that their Prime-eligible items will ship to you free, whether you have Prime or not. If you don’t have Prime and don’t reach the $49 tier for Super Saver Shipping, you should remember this rule across the entire site. Don’t click on the “Add to Cart” button without closer inspection. Amazon is simply adding yet another inconvenience for non-Prime shoppers. (I can’t wait for the new Top Gear, er… Grand Tour to start though!)

Following the news of the Yahoo hack of half a billion users (noted as the

Following the news of the Yahoo hack of half a billion users (noted as the  Marriott completed its acquisition of Starwood Hotels last week, and has already started the merging process for their loyalty rewards programs. Both programs will essentially be run separately for a while, but you can now match status and exchange points. The new name is Marriott International, although a full merger will not be completed until sometime in 2018. Here’s a quick summary of your options:

Marriott completed its acquisition of Starwood Hotels last week, and has already started the merging process for their loyalty rewards programs. Both programs will essentially be run separately for a while, but you can now match status and exchange points. The new name is Marriott International, although a full merger will not be completed until sometime in 2018. Here’s a quick summary of your options: There is a lot of focus on how to accumulate a big nest egg, but possibly even more complicated is how to spend it down. Vanguard Research has released a new whitepaper called

There is a lot of focus on how to accumulate a big nest egg, but possibly even more complicated is how to spend it down. Vanguard Research has released a new whitepaper called

Uber and Android Pay are running a

Uber and Android Pay are running a  As open enrollment season is around the corner, Morningstar offered up an

As open enrollment season is around the corner, Morningstar offered up an  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)