The Vanguard 529 College Savings Plan (based in Nevada but open to all state residents) is one of the consistent Morningstar top-ranked 529 plans and one of my three personal finalists when choosing a plan for myself.

While poking around the site, I also came across this interactive map tool that helps you compare your in-state plan with the Vanguard/Nevada plan. Although created by Vanguard, it still offers a lot of useful information and I’m okay with then Vanguard plan being used as a benchmark.

Below is an example screenshot for Utah. Note that it will tell you if you have an in-state tax benefits, and also if that tax benefit is restricted to contributions to your in-state plan only. Where applicable, it also links to Vanguard’s 529 tax deduction calculator. Finally, if you click on “Full Comparison” you can dig even deeper.

As an example of why Vanguard is highly-regarded, I was recently notified that Vanguard once again lowered the expense ratios on many of their 529 investment options. This matches the same trend with their regular mutual funds and ETFs.

Effective May 3, 2016, the expense ratios for all Vanguard 529 Plan investment options went down, affirming Vanguard’s ongoing commitment to lowering costs for our clients. Now you’ll be saving even more. The cost of our age-based options decreased from 0.19% to 0.17%, which is 67% less than the industry average.* And the expense ratios of our individual portfolios dropped from a range of 0.19% to 0.49% to a range of 0.17% to 0.45%.

Here are some similar resources I’ve shared before: 50-state 529 tax benefit comparison (uses a common hypothetical family) and SavingForCollege tax benefit calculator.

This is becoming a recurring theme around here, but I came across an interesting tidbit in this

This is becoming a recurring theme around here, but I came across an interesting tidbit in this

In response to the flood of information constantly coming at us, there are daily e-mail round-ups that curate and summarize. A popular general news newsletter that I enjoy is

In response to the flood of information constantly coming at us, there are daily e-mail round-ups that curate and summarize. A popular general news newsletter that I enjoy is

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

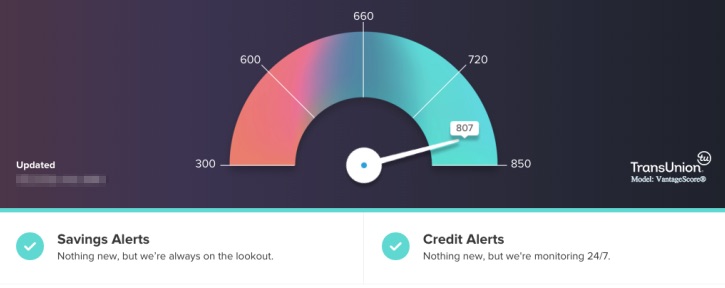

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)