The URL is suspiciously generic and raised my scam radar, but Experian-owned FreeCreditScore.com has been revamped to offer a pretty good package – a free FICO score, full credit report, and free credit monitoring based on your Experian credit report data. (Continue to be wary of other less-credible sites.) Like most of its competitors, “free” means that you agree to let them market products to you based on your personal information. This post provides additional details regarding this service.

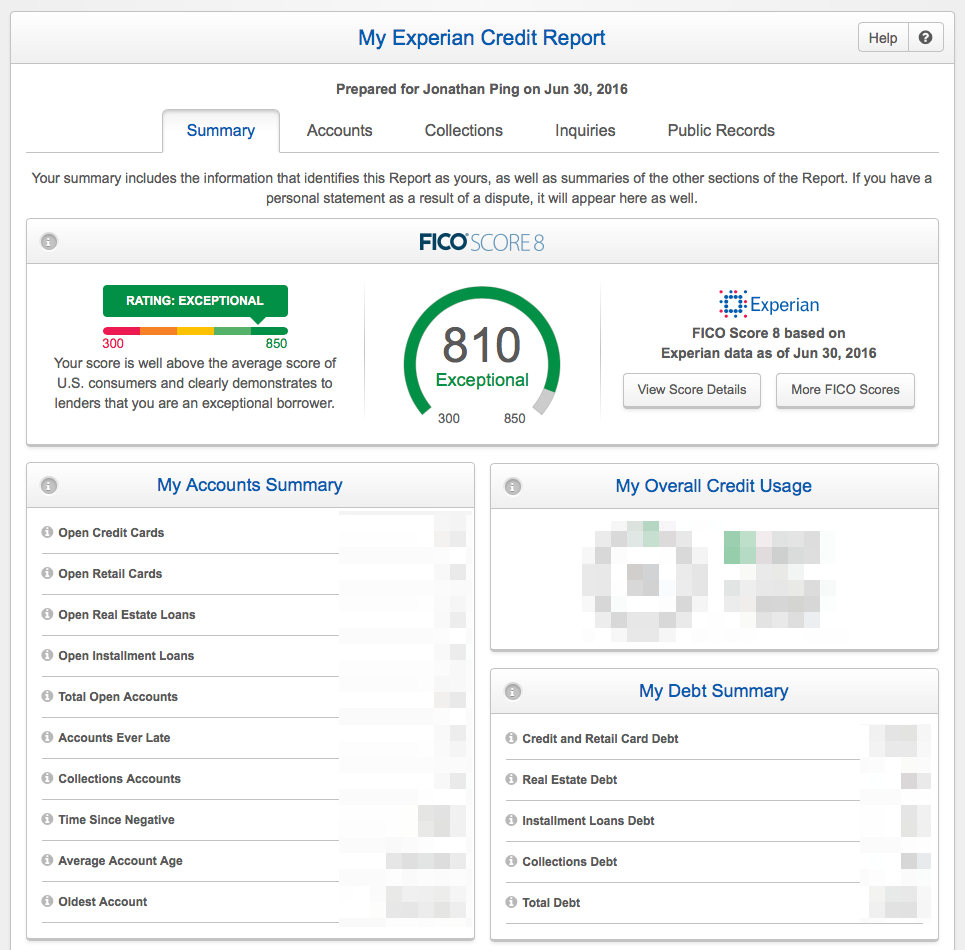

FICO Score details.

- FICO Score version: FICO Score 8, or FICO 08. This is the most widely used of the many FICO flavors. Score version is directly shown on the website.

- Credit bureau: Experian

- Update frequency: Every 30 days or when you log in, whichever is longer.

- Limitations: Available to everyone. No specific credit card required.

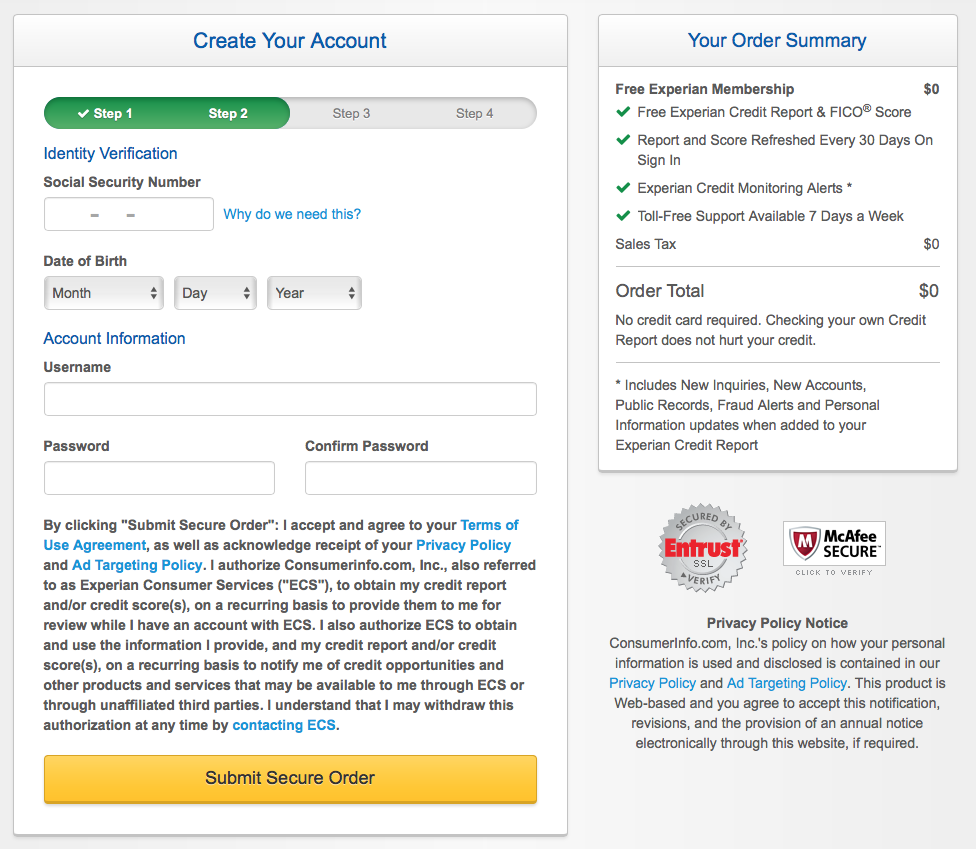

How to get your score. Here’s a preview of the application and approval process:

- You must provide personal information, including Social Security Number. Name, address, etc. This is required for any service that checks your credit score.

- You must agree to their Privacy Policy and Ad Targeting Policy. Basically, they will give your free access to your credit score and other credit information, and they will also collect personal information to market products and other services to you. Your information may also be shared with their affiliates.

- Identity verification questions. They will ask you some multiple choice questions based on your Experian credit report data in order to verify your identity. If you don’t pass this quiz, I would go over to AnnualCreditReport.com and get a copy of your report to scan for errors.

- Set your personal security questions. At this point, you are approved. You just need to set up the standard security questions like “Who was your 2nd grade teacher?”

What kind of information do you get? The score model is FICO Score 8, based on your Experian credit report. This is the same score model and credit bureau offered by American Express and CreditScoreCard by Discover, and is within a few points for me (the check dates are slightly off). The other two major bureaus are TransUnion and Equifax.

The major difference is that FreeCreditScore.com offers your full Experian credit report and ongoing credit monitoring of your Experian credit data. This includes any new credit inquiries, new accounts, pubic records, fraud alerts, and other personal information updates to your Experian credit report.

How often is it updated? As often as every 30 days, but only if you log in to the website. Many sites operate this way, as it reduces their costs of grabbing your score if you are no longer interested. Also, they want you to log in so that they can show you advertisements.

Screenshots. Here’s a look at my sign-up process and account page:

Bottom line. Experian owns FreeCreditScore.com and has jumped in fully into the “free score for showing you ads” business model. As they aren’t a credit card issuer, they can feel free to open it up to everyone. They offer the full Experian package of free FICO score, full credit report, and free credit monitoring based on your Experian credit report data. Most other Experian-based providers only offer one out of these three.

There are a lot of options out there now, but if you wanted to cover the other two bureaus efficiently, consider that CreditKarma.com offers free weekly updates of both your TransUnion and Equifax credit report factors in one site. You also get free weekly non-FICO credit scores and free automatic, daily TransUnion credit monitoring.

Related: Here are major credit card issuers with free FICO programs:

Earlier this year, JetBlue wanted to merge with Virgin America, but Alaska Airlines ended up winning the bidding war. Now they are just fighting over potential customers, which means some interesting things for us!

Earlier this year, JetBlue wanted to merge with Virgin America, but Alaska Airlines ended up winning the bidding war. Now they are just fighting over potential customers, which means some interesting things for us!

A few of you are waiting for me to talk about Brexit. Part of me is honored that you care about my opinion. The other part of me is appalled that you care about my opinion. Why would you listen to me?!? 😉 Here goes:

A few of you are waiting for me to talk about Brexit. Part of me is honored that you care about my opinion. The other part of me is appalled that you care about my opinion. Why would you listen to me?!? 😉 Here goes: Sam’s Club must be tired of Costco getting all this free publicity from them

Sam’s Club must be tired of Costco getting all this free publicity from them  Have you been unsuccessfully searching Netflix for a 72-minute documentary about index funds? Well, your wait is finally over. Game of Thrones, watch your back! 🙂

Have you been unsuccessfully searching Netflix for a 72-minute documentary about index funds? Well, your wait is finally over. Game of Thrones, watch your back! 🙂 The short version: Apple settled an e-Book antitrust lawsuit for $400 million. Click

The short version: Apple settled an e-Book antitrust lawsuit for $400 million. Click

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.

Here are some helpful resources on owning only bonds of the highest credit quality as part of your portfolio asset allocation.  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)