![]() Here is an updated link to the Best Cash Rates for 2019. But with the growing popularity of “robo-advisors” that manage your retirement portfolio using automated software, what if there was a robo-advisor for rate chasing?

Here is an updated link to the Best Cash Rates for 2019. But with the growing popularity of “robo-advisors” that manage your retirement portfolio using automated software, what if there was a robo-advisor for rate chasing?

That’s the basic idea behind MaxMyInterest.com (Max). You set a Target Value you’d like to keep in your standard “brick-and-mortar” checking account. Max will then sweep any excess funds into whatever online savings bank has the highest yield. If their rates change, Max can move your money again. If your checking account balance gets low, Max will move money back into your checking account for you. The ole’ hub and spoke graphic:

If your balance exceeds the FDIC insurance limits of $250,000 per account type, Max will move the rest into the bank with the next-highest yield, and so on. T

What banks does it work with? They officially support checking accounts from the following big banks. Their application suggests that they may support other checking accounts. (The official list has also expanded a bit since their launch.)

- Bank of America

- Citibank

- First Republic Bank

- JPMorgan/Chase

- Wells Fargo

- Charles Schwab Bank

- US Bank

Max will use one of these five online banks as your spokes (others may be added in the future, but only these work right now):

- Ally Bank

- American Express

- Barclays

- Capital One 360

- GE Capital

You can have them open already, or you can only open a few, or you can use their “common application” to apply for all of them at once.

The cost? 0.02% per quarter, or 0.08% per year.

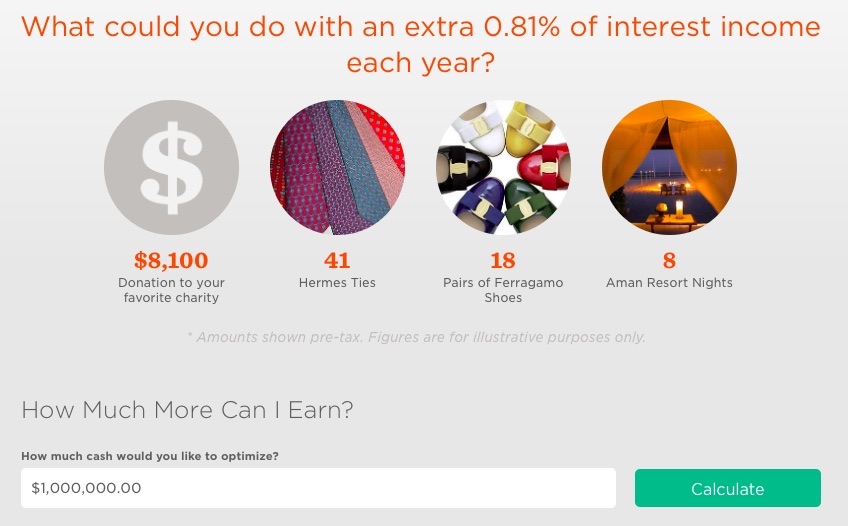

You can get an idea of their target audience from their marketing materials. I didn’t even know Hermes sold ties, let alone that they cost $200 a pop!

Recap. I certainly think the idea is a neat one. But considering the cost and restrictions to the specific five online banks, the greatest appeal of MaxMyInterest is probably to people with $250,000+ balances that want the maintain the safety FDIC-insurance without having to juggle multiple accounts on their own. For most people that don’t have that much sitting around in cash, simply picking a single online savings account with a good track record of offering high interest rates should be good enough.

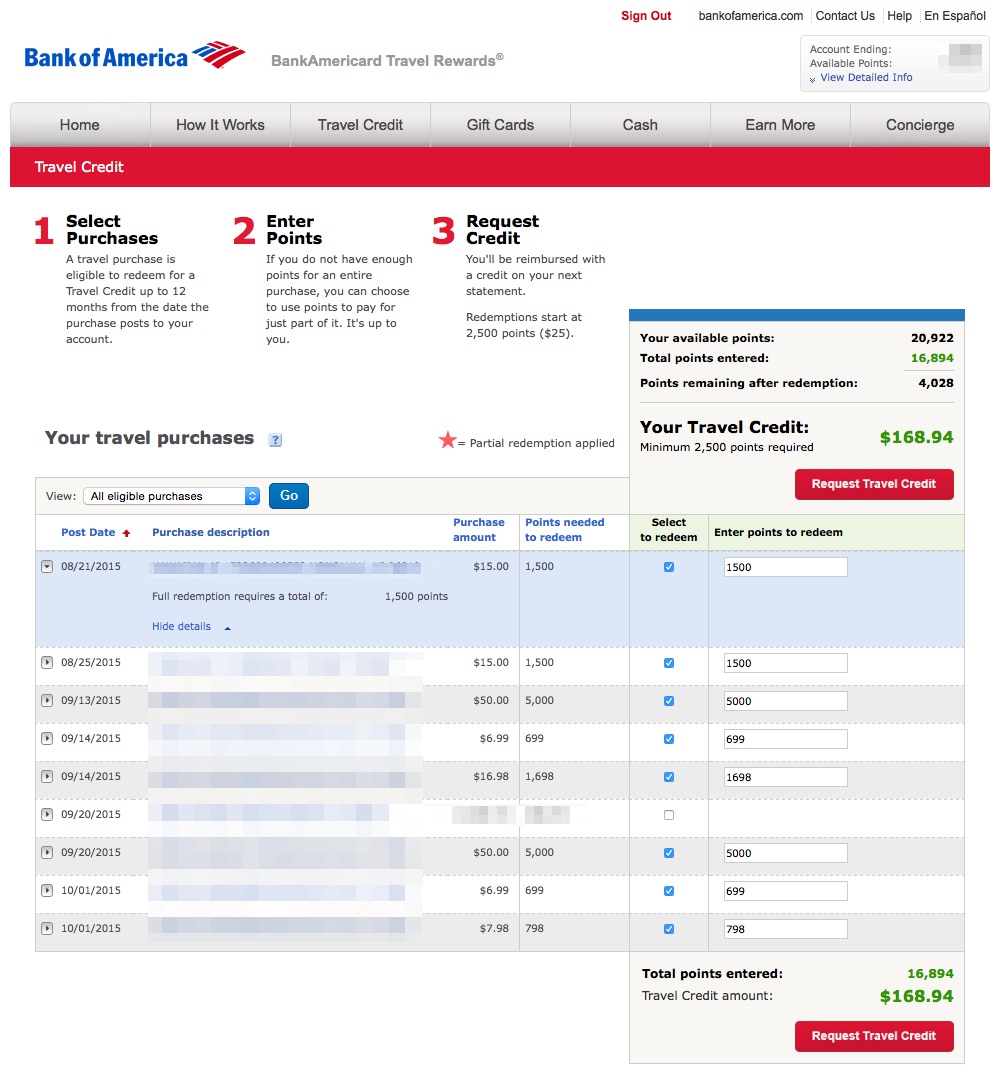

Bank of America runs a program called

Bank of America runs a program called

Here’s an update on one of my

Here’s an update on one of my

Inside a post about what economists think about buying vs. renting a house,

Inside a post about what economists think about buying vs. renting a house,  Mid-Feburary is the time of year when writers everywhere tie their subject matter to Valentine’s Day. Here’s how mine came about. I was reading

Mid-Feburary is the time of year when writers everywhere tie their subject matter to Valentine’s Day. Here’s how mine came about. I was reading  Most travel cards offer an ongoing sign-up bonus, but it’s even better when you snag them during a bump-up – this time it is the Marriott Rewards® Premier Credit Card from Chase. Check out the highlights below, and remember that it is free and takes just a minute to add an authorized user:

Most travel cards offer an ongoing sign-up bonus, but it’s even better when you snag them during a bump-up – this time it is the Marriott Rewards® Premier Credit Card from Chase. Check out the highlights below, and remember that it is free and takes just a minute to add an authorized user:

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)