Savingforcollege.com is a popular privately-run site for researching and comparing 529 college savings plans. They released their updated ratings this month, which represents their “opinion of the overall usefulness of a state’s 529 plan based on many considerations.” The judgement criteria include:

Savingforcollege.com is a popular privately-run site for researching and comparing 529 college savings plans. They released their updated ratings this month, which represents their “opinion of the overall usefulness of a state’s 529 plan based on many considerations.” The judgement criteria include:

- Performance. They selected similar “apples-to-apples” portfolios with 7 different asset allocations from each plan and rated them based on historical performance. Rankings are updated each quarter.

- Costs. Total average asset-based expense ratios among plans are compared, in addition to separately considering program manager fees, administrator fees, and annual account maintenance fees.

- Features. This includes other factors that affect participants, including the ability of the plan change their investment options quickly if called for; creditor protection under the sponsoring state’s laws; availability of FDIC-insured options; minimum and maximum contribution restrictions.

- Reliability. The appears to measure the likelihood of a good plan staying a good plan. Do they have experienced program managers? Does the plan have a good amount of assets? What is the quality of the documentation and reporting? How restrictive are the withdrawal and rollover processes?

Here is the full list of 5-Cap Ratings for each state, on a scale of 0 to 5 Caps. Note that there are separate ratings for in-state and out-of-state residents. The following plans received a 5-Cap Rating for in-state residents (alphabetical order):

- California: The ScholarShare College Savings Plan

- Colorado: Direct Portfolio College Savings Plan

- Colorado: Scholars Choice College Savings Program – Advisor Plan

- Illinois: Bright Start College Savings Program – Direct Plan

- Iowa: College Savings Iowa

- Maine: NextGen College Investing Plan – Direct Plan

- Maine: NextGen College Investing Plan – Advisor Plan

- Michigan: Michigan Education Savings Program

- Nebraska: Nebraska Education Savings Trust – Advisor Plan

- Nebraska: Nebraska Education Savings Trust – Direct Plan

- New York: New York’s College Savings Program – Direct Plan

- Ohio: Ohio CollegeAdvantage 529 Savings Plan

- Rhode Island: CollegeBoundfund – Direct Plan

- South Carolina: Future Scholar 529 College Savings Plan – Advisor Plan

- South Carolina: Future Scholar 529 College Savings Plan – Direct Plan

- Utah: Utah Educational Savings Plan (USEP)

- West Virginia: SMART529 WV Direct College Savings Plan

- Wisconsin: Edvest

Out of the 100+ different plans they rated, here are the 4 programs that attained the top 5-Cap Rating for out-of-state residents (alphabetical order):

- California: The ScholarShare College Savings Plan

- Maine NextGen College Investing Plan – Direct Plan

- New York’s College Savings Program – Direct Plan

- Ohio CollegeAdvantage 529 Savings Plan

Consistently top-rated plans. The last time I noted these rankings was 2012, and the following plans were 5-Cap rated back then and also now: California, New York, and Ohio.

I should point out that the SavingForCollege Top-rated 5-Cap plans are different than the Morningstar Top-rated Gold plans. In fact, there is no overlap at all! Two of my favorite Gold-rated plans, the Vanguard 529 Savings Plan (Nevada) and Utah Educational Savings Plan received 4.5 out of 5 Caps, although I am not exactly sure why.

However, in general the top 15 or so plans are pretty much the same for both. With that in mind, I see nothing wrong with most Morningstar Silver Plans and/or the 4.5 Cap SavingForCollege plans, if their investment options meet your needs. Here were my personal finalist 529 plans and asset allocations.

Finally, here is another resource about comparing the state-specific tax benefits that may be available to you.

We are currently planning a 4-week European trip with our young children (age 1 and 3). The most common reactions are “Cool. Wait, you’re not bringing the kids, are you?” followed by “You’re nuts.” At first, we didn’t think it could be done either. It does take a lot of additional planning for car seats, cribs, kid-friendly itineraries, and so on.

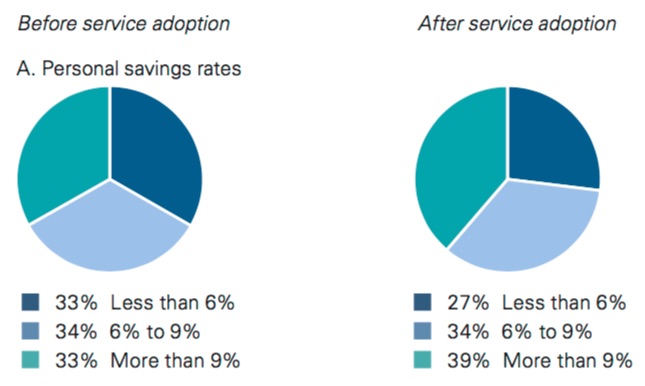

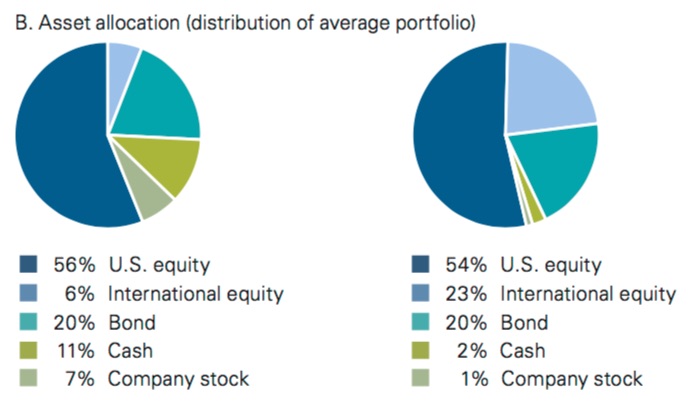

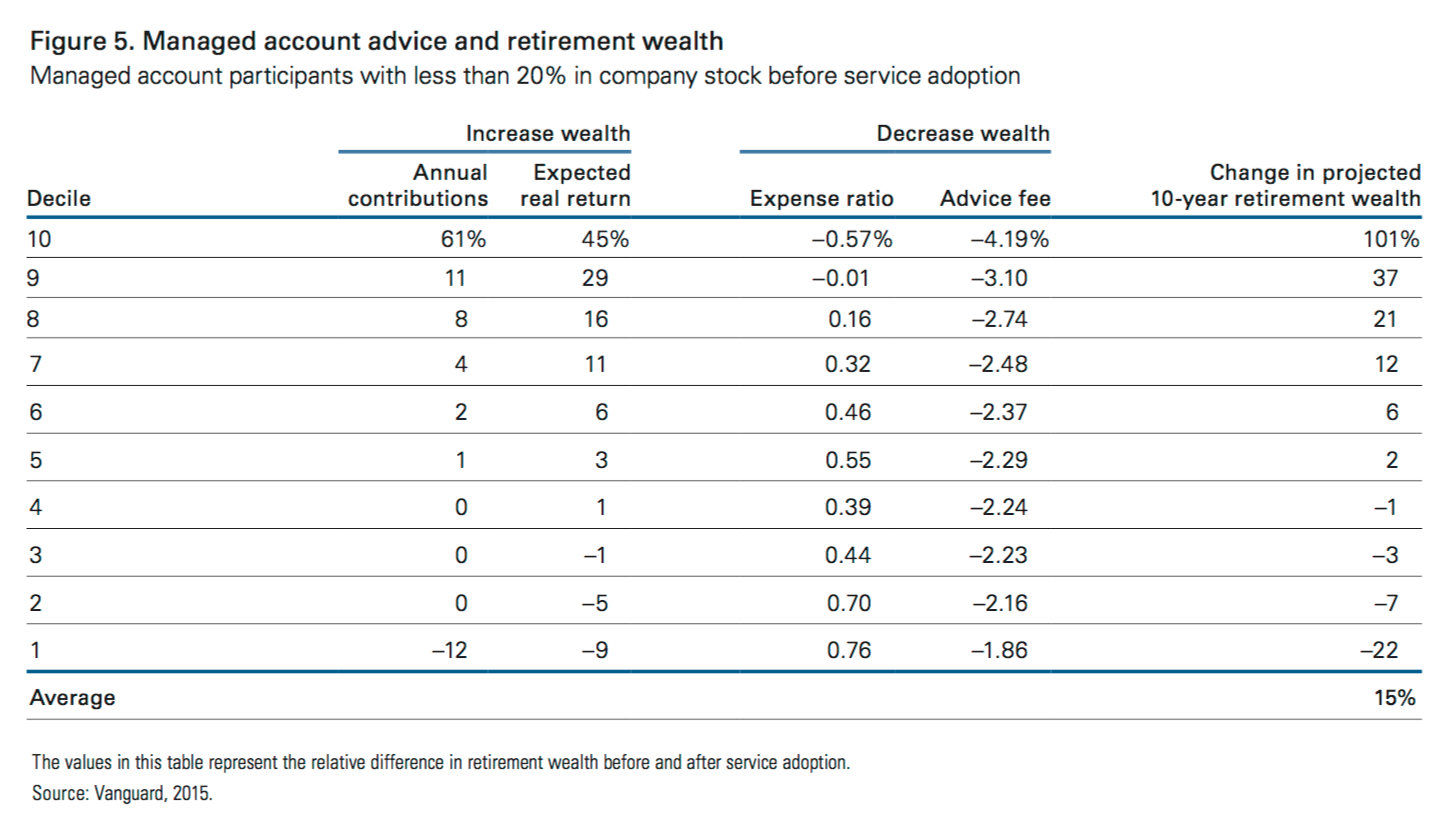

We are currently planning a 4-week European trip with our young children (age 1 and 3). The most common reactions are “Cool. Wait, you’re not bringing the kids, are you?” followed by “You’re nuts.” At first, we didn’t think it could be done either. It does take a lot of additional planning for car seats, cribs, kid-friendly itineraries, and so on.  Vanguard is the one of the biggest providers of defined contribution (DC) plans like 401(k) and 403(b) plans, with more than 3.9 million participants. An optional service they provide for these DC plans is managed account advice, where you pay them an asset-based fee and you cede all portfolio control to them. Vanguard Managed Account Program (VMAP) serves as a fiduciary that sets asset allocations, chooses investments, and monitors/rebalances portfolios on a continuing basis. Fees typically begin at 0.40% on the first $100,000 in assets under management.

Vanguard is the one of the biggest providers of defined contribution (DC) plans like 401(k) and 403(b) plans, with more than 3.9 million participants. An optional service they provide for these DC plans is managed account advice, where you pay them an asset-based fee and you cede all portfolio control to them. Vanguard Managed Account Program (VMAP) serves as a fiduciary that sets asset allocations, chooses investments, and monitors/rebalances portfolios on a continuing basis. Fees typically begin at 0.40% on the first $100,000 in assets under management.

This post is for the fortunate folks who may possibly exceed the often-quoted $500,000 limits for SIPC insurance ($250,000 for cash). The way this insurance works wasn’t necessarily obvious to me, and although it is often compared to the FDIC insurance of banks, there are many important differences.

This post is for the fortunate folks who may possibly exceed the often-quoted $500,000 limits for SIPC insurance ($250,000 for cash). The way this insurance works wasn’t necessarily obvious to me, and although it is often compared to the FDIC insurance of banks, there are many important differences.

While catching up on some reading, it was refreshing to see Bill Gates offer a more positive spin with his Top 6 Good-News Stories of 2015. One of them was that the College Board announced free, high-quality SAT practice at

While catching up on some reading, it was refreshing to see Bill Gates offer a more positive spin with his Top 6 Good-News Stories of 2015. One of them was that the College Board announced free, high-quality SAT practice at  I’ve never really identified with comedians. I’m not funny, and I always avoid large crowds. But after reading the fascinating notes at

I’ve never really identified with comedians. I’m not funny, and I always avoid large crowds. But after reading the fascinating notes at  Did you as a small business pay another person or unincorporated business more than $600 total in the last year? You may have to provide them a 1099-MISC form.

Did you as a small business pay another person or unincorporated business more than $600 total in the last year? You may have to provide them a 1099-MISC form.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)