This post provides updated information and instructions regarding the free FICO score that is available to Citibank credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to Citibank credit card holders.

Background. While their plans were announced in late 2014, Citi started offering free FICO scores to select cardholders in January 2015.

FICO Score details.

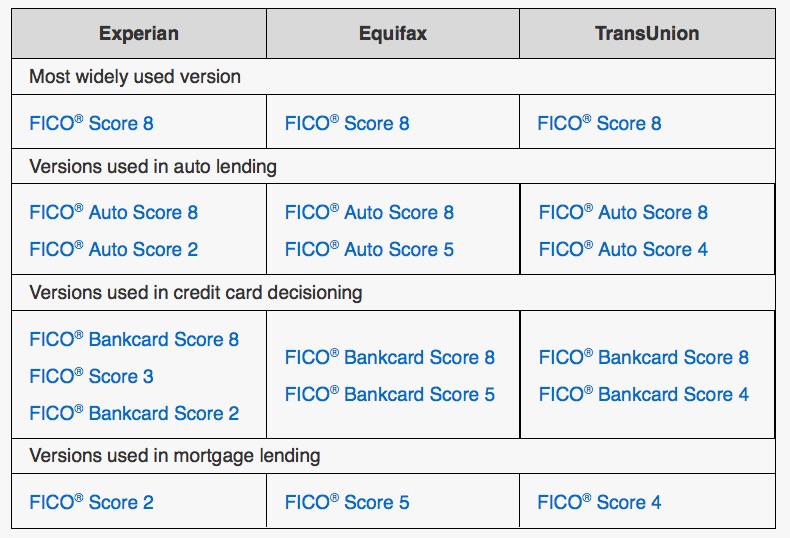

- FICO Score version: FICO® Bankcard Score 8 model. This is an industry-specific model tailored to credit card decisioning, with a range of 250 to 900. (The “classic” FICO range is 300-850.) This is one of the many FICO flavors. Score version is taken directly from Citi website and press release.

- Credit bureau: Equifax

- Update frequency: Monthly

- Limitations: Available to all “Citi-branded consumer credit cardmembers”. Reports are that the following cards are eligible:

- Citi® Double Cash Card (I have this and got my free score)

- Citi® / AAdvantage® Platinum Select® Mastercard® and Citi® / AAdvantage® Executive World Elite™ MasterCard (co-branded American Airlines)

- Citi® Dividend Platinum Select® Visa® Card

- Citi® Thank You Cards

- Citi Simplicity® Card

- Citi Forward® Card

- Citi Prestige® Card

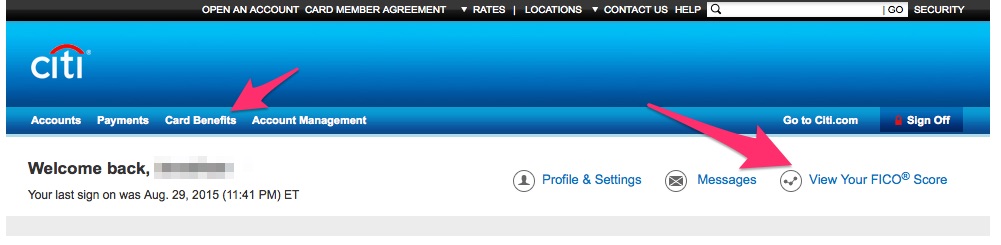

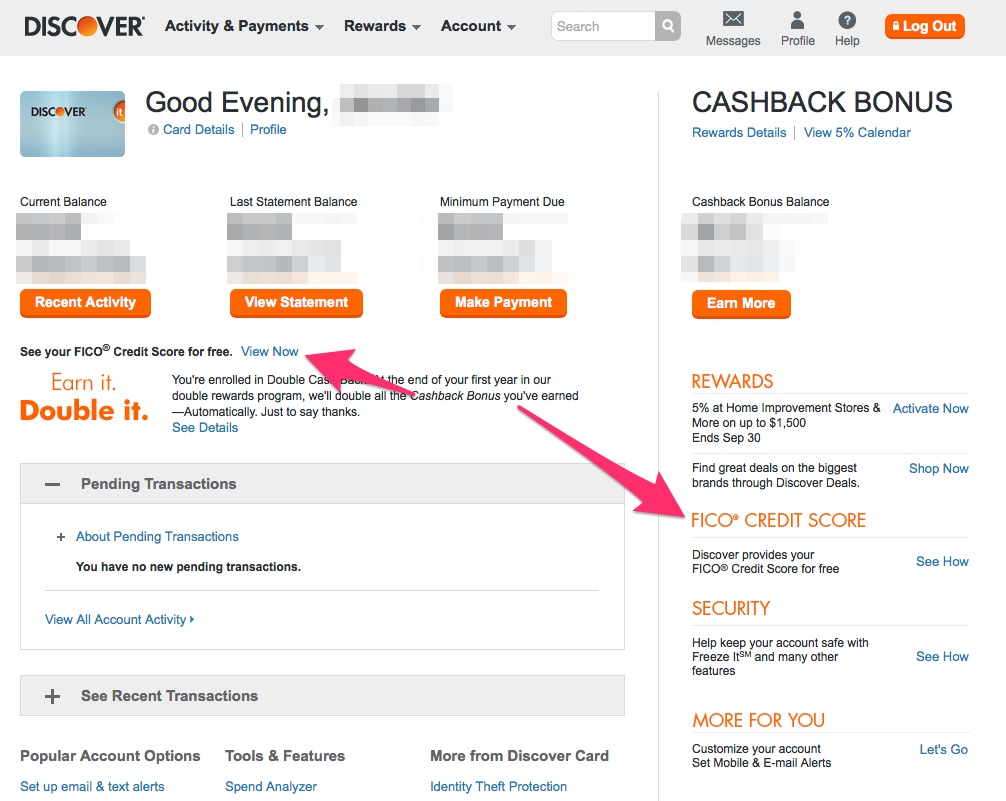

How to find the score. You can find the free FICO score on your online account access. According to a January 2015 press release, you can also request them to mail it to you. After logging in, look for either the “View your FICO Score” link or click on the “Card Benefits” tab. See screenshot below (click to enlarge):

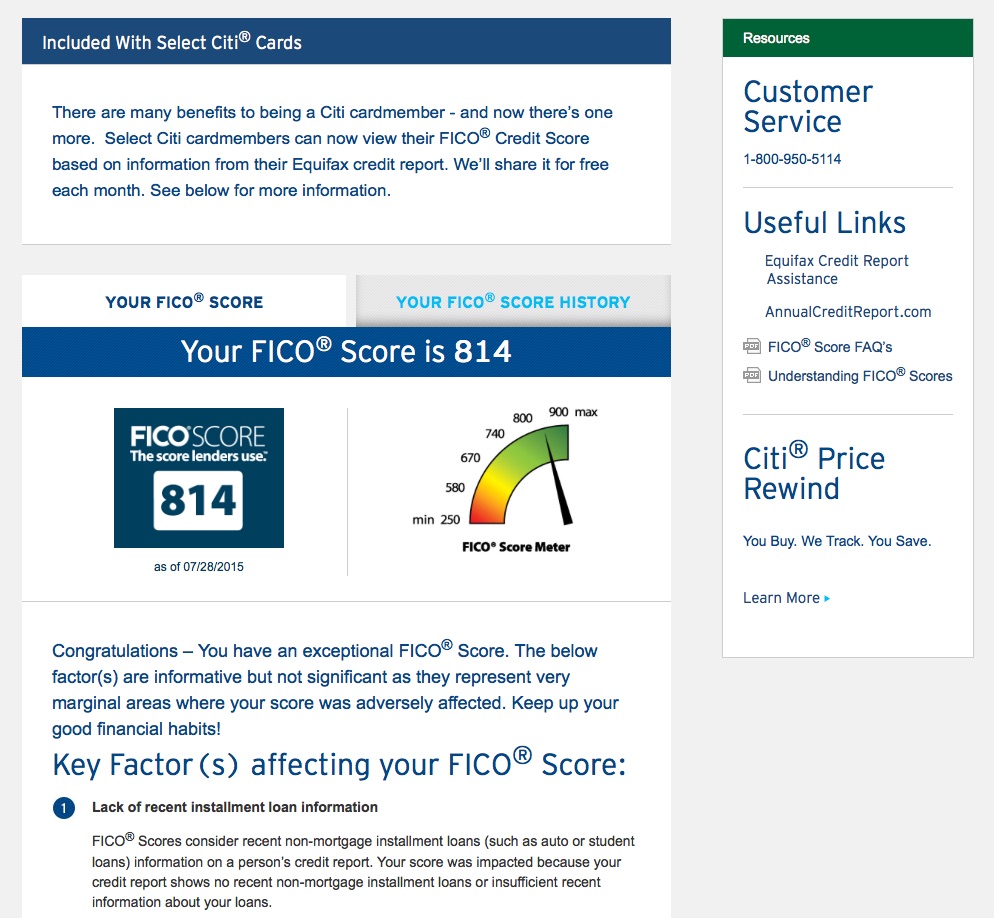

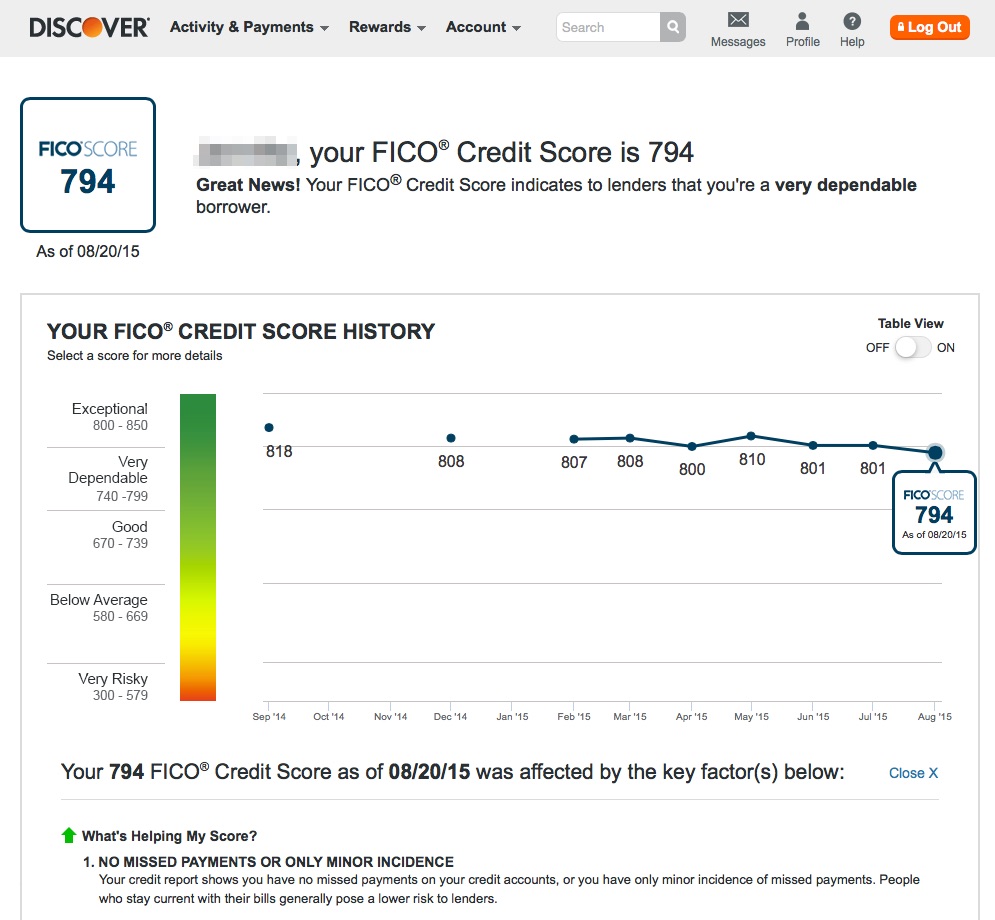

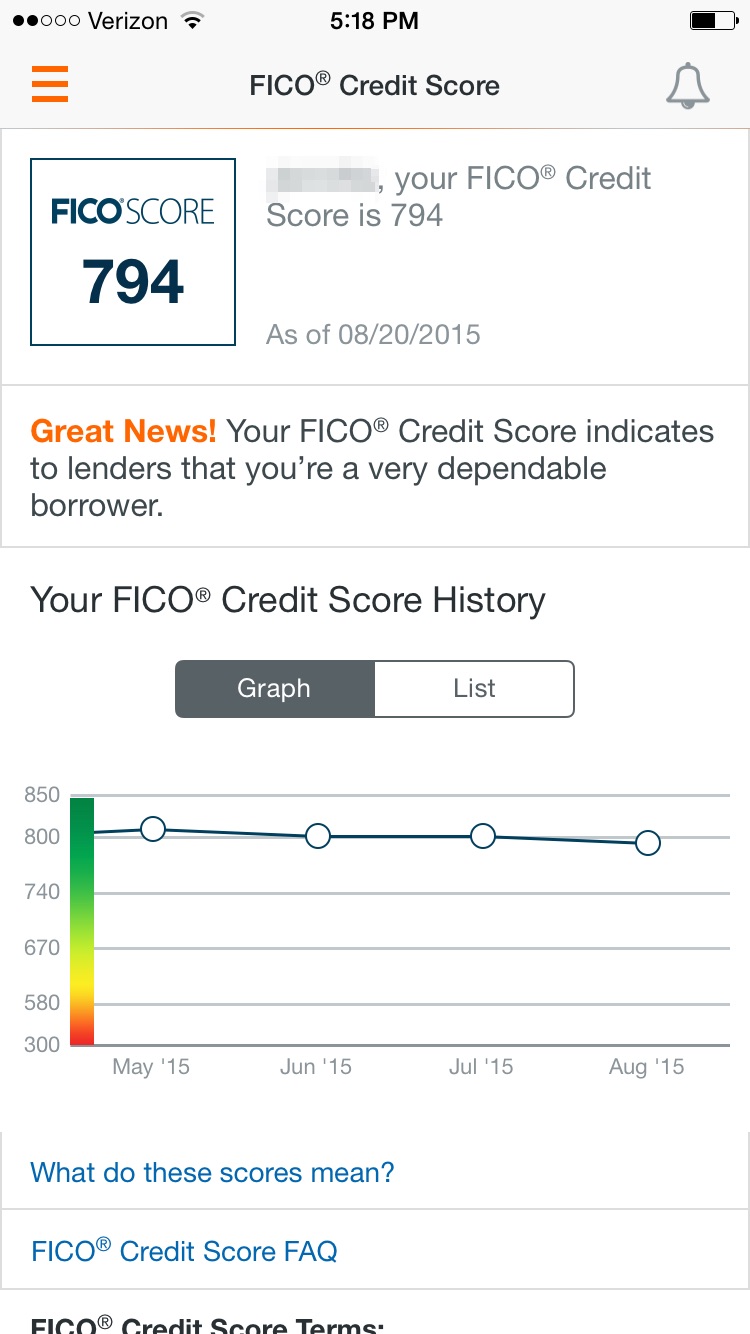

Here are some example screenshots of what information is provided. Here is the latest score, a score meter, and the top two factors impacting your score:

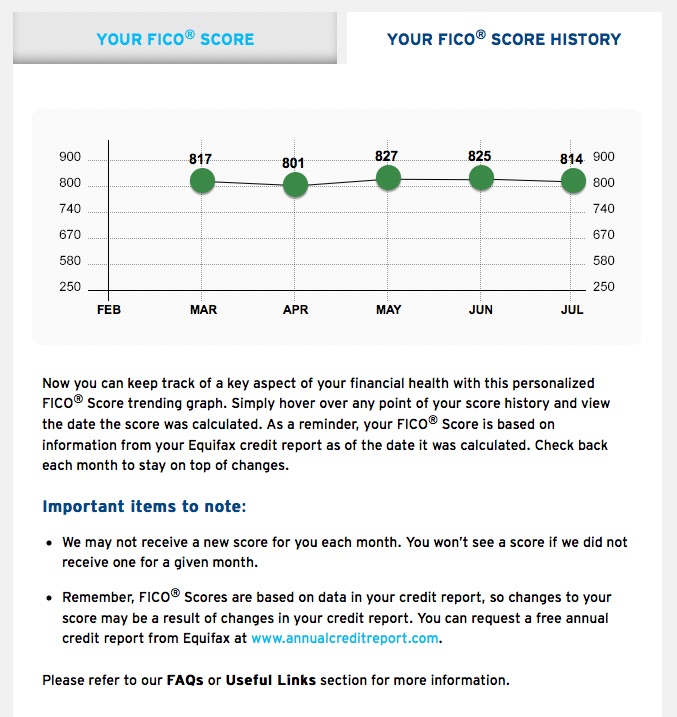

They also provide a score history:

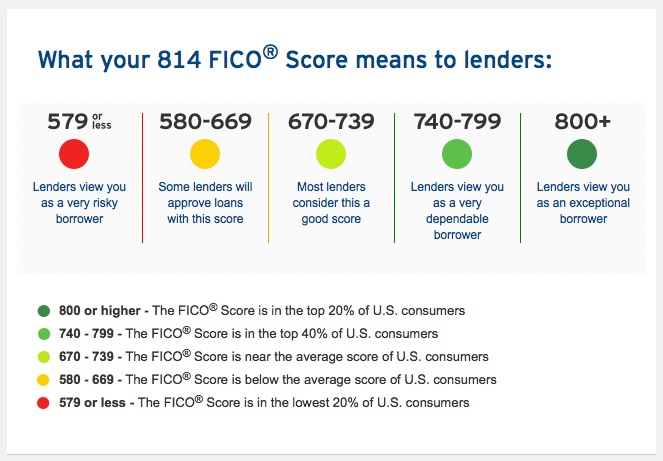

Here is a visual of the score range to help understand what each range means to lenders:

Fine print:

Your FICO® Score is calculated based on data from Equifax using the FICO® Bankcard Score 8 model and may be different from other credit scores. FICO® Scores are intended for and delivered only to the Primary cardmember and only if a FICO® Score is available. Disclosure of this score is not available for all Citi products and Citi may discontinue displaying the score at our discretion.

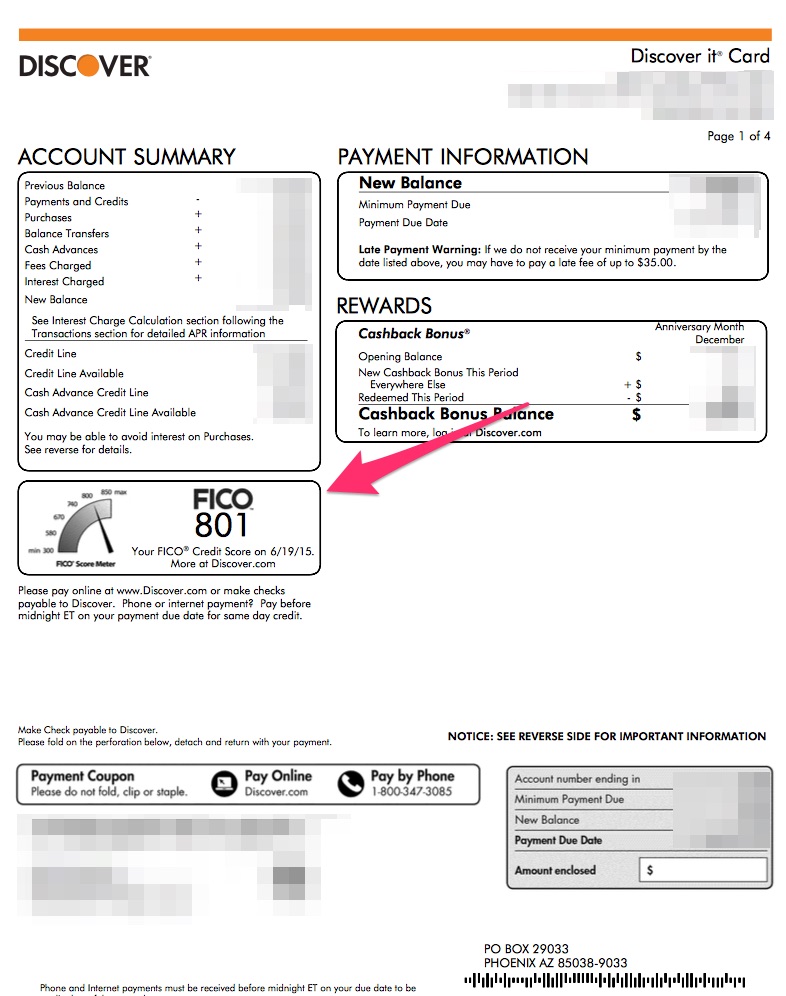

This post provides updated information and instructions regarding the free FICO score that is available to Discover credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to Discover credit card holders.

If you have an Android smartphone or tablet, Amazon just released

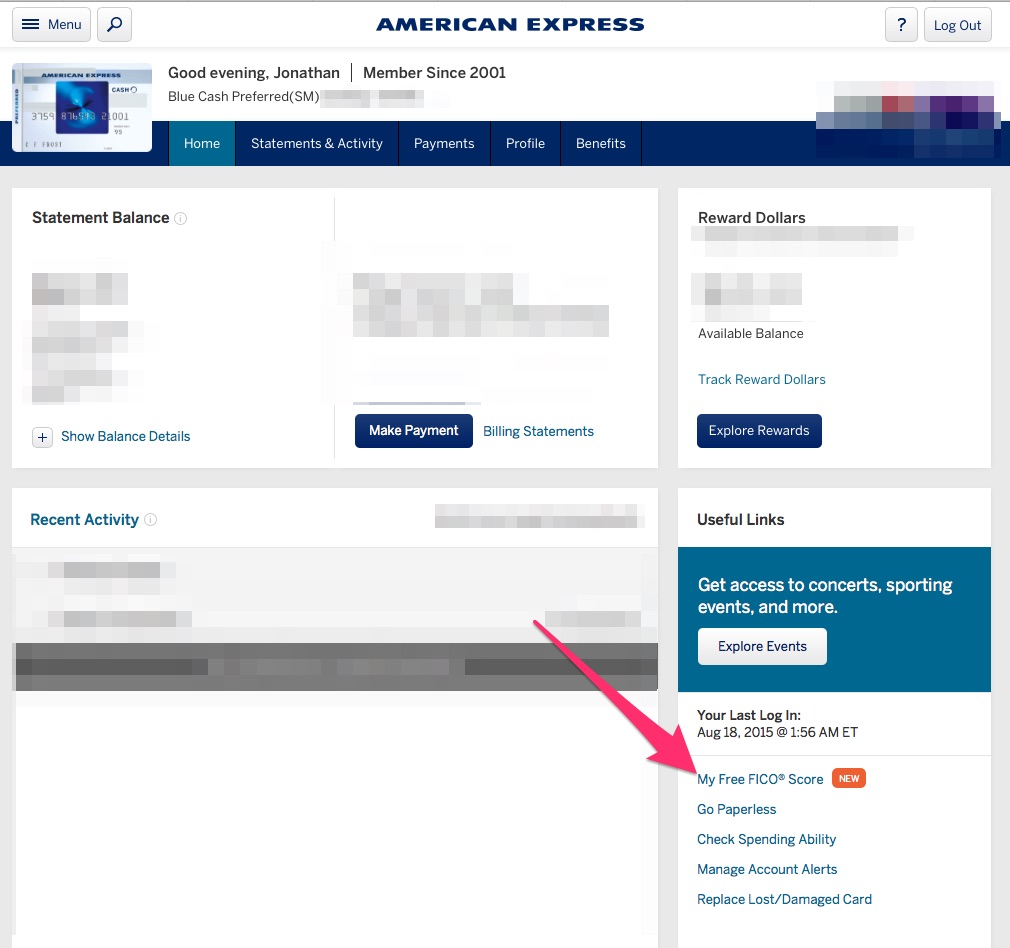

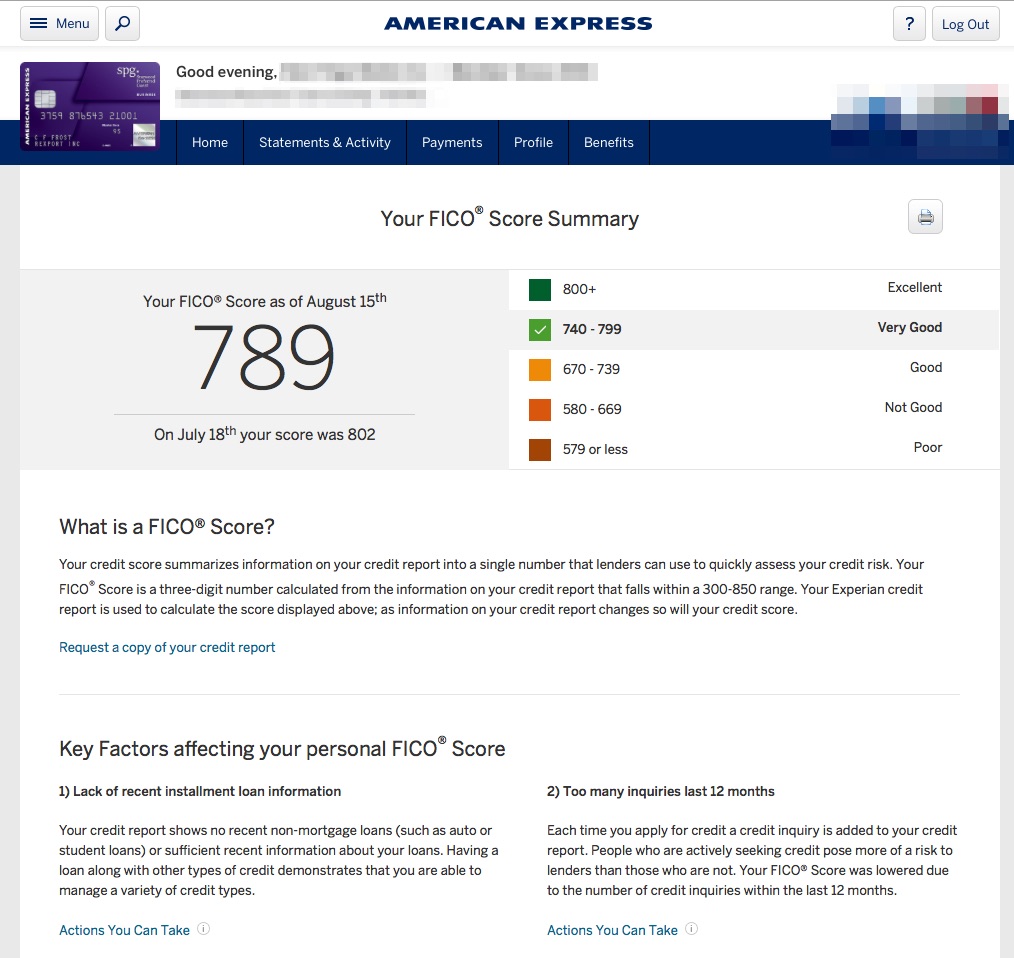

If you have an Android smartphone or tablet, Amazon just released  This post provides updated information and instructions regarding the free FICO score that is available to American Express credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to American Express credit card holders.

Every week it seems there is a new way to get a free FICO score. Over the last 10 years, I’m pretty sure I’ve only paid for a FICO score once when I was paranoid about my first mortgage application. Why aren’t they charging us $15 a pop anymore? My opinion is that FICO realized that:

Every week it seems there is a new way to get a free FICO score. Over the last 10 years, I’m pretty sure I’ve only paid for a FICO score once when I was paranoid about my first mortgage application. Why aren’t they charging us $15 a pop anymore? My opinion is that FICO realized that:

Expedia.com has revamped their in-house loyalty rewards program. Citi and Expedia have partnered on a new set of co-branded credit cards.

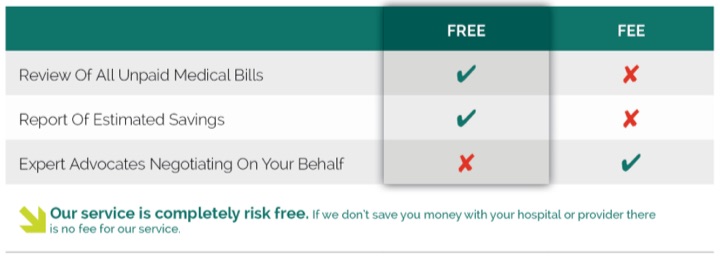

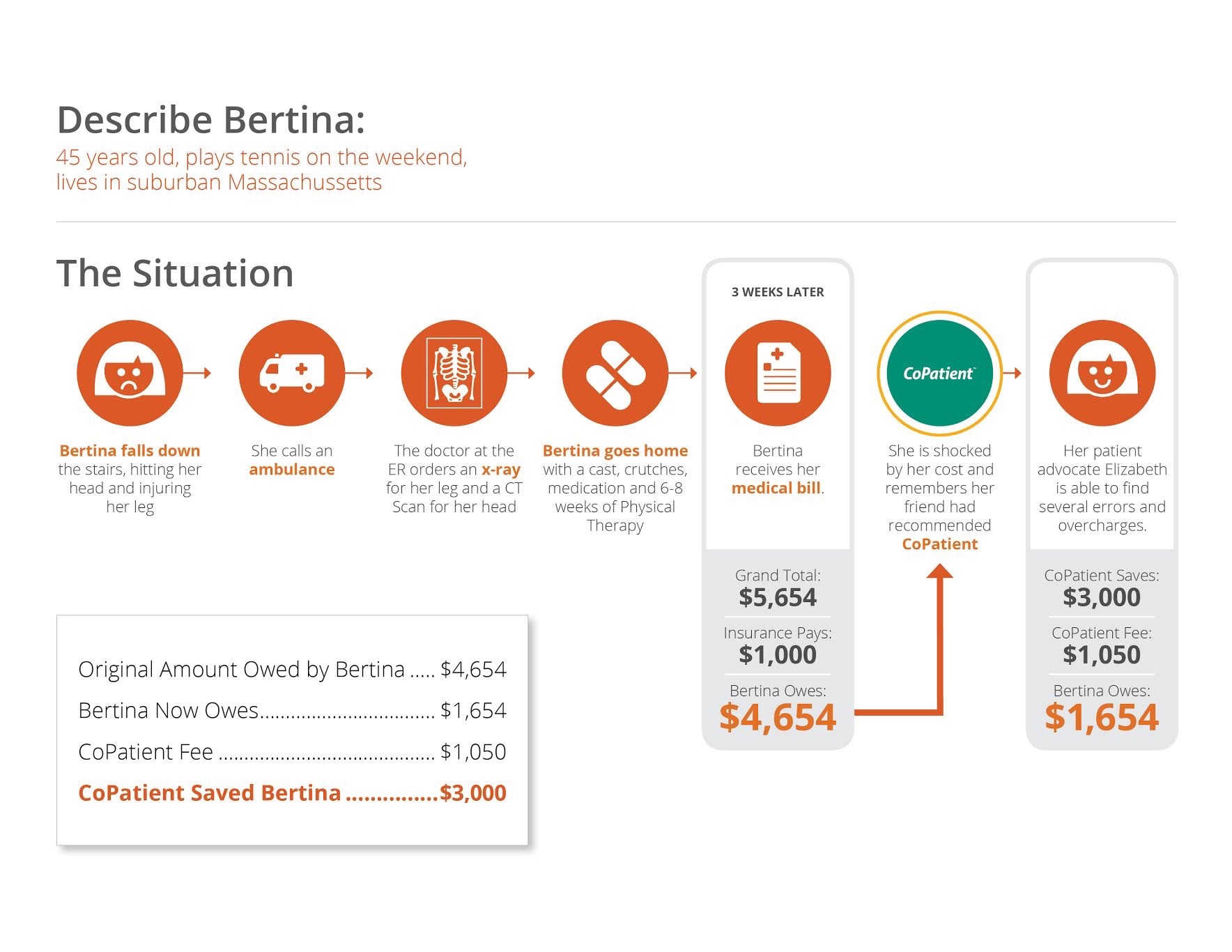

Expedia.com has revamped their in-house loyalty rewards program. Citi and Expedia have partnered on a new set of co-branded credit cards.  High-deductible health plans are still growing in popularity. While these can be a great way to save on your monthly premiums, it also means that when you do have to visit the emergency room, you get to tackle nearly the entire bill instead of a small co-pay. The problem is that most medical bills cannot be understood by mere mortals. Likely, the doctors and nurses themselves have no clue how that $6,344 bill for a broken arm got generated.

High-deductible health plans are still growing in popularity. While these can be a great way to save on your monthly premiums, it also means that when you do have to visit the emergency room, you get to tackle nearly the entire bill instead of a small co-pay. The problem is that most medical bills cannot be understood by mere mortals. Likely, the doctors and nurses themselves have no clue how that $6,344 bill for a broken arm got generated.

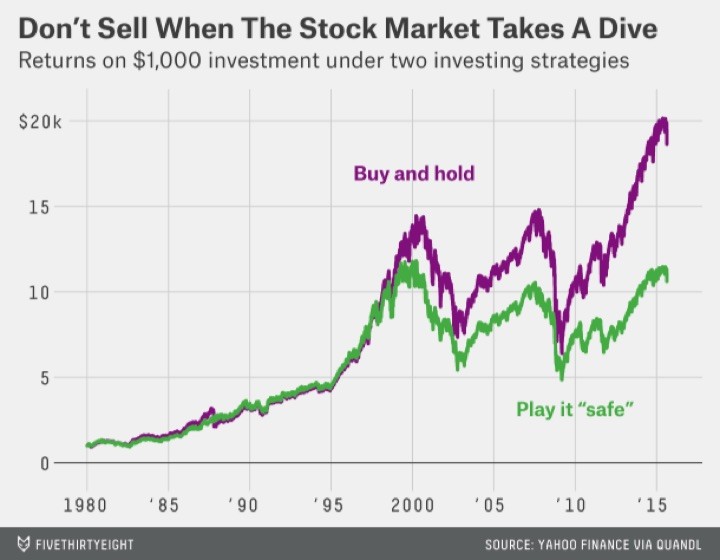

After you spend enough time consuming financial media week after week, you start seeing patterns in the noise. I understand why of course, as creating content to feed the beast can get quite exhausting. But hopefully, by pointing out these out, you as an individual investor can realize that there may or may not be any substance behind the marketing buzzwords and short-term forecasts. Entertaining? Yes. Useful and actionable? Much less likely.

After you spend enough time consuming financial media week after week, you start seeing patterns in the noise. I understand why of course, as creating content to feed the beast can get quite exhausting. But hopefully, by pointing out these out, you as an individual investor can realize that there may or may not be any substance behind the marketing buzzwords and short-term forecasts. Entertaining? Yes. Useful and actionable? Much less likely. The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)