I’m currently reading The One-Page Financial Plan by Carl Richards, who also writes for the New York Times. Given the title, I thought it would be a quick read but it turns out to cover a variety of topics over its 200+ pages. So far, I like that it comes from the point of view of an experienced financial planner who spends his days talking with clients.

I’m currently reading The One-Page Financial Plan by Carl Richards, who also writes for the New York Times. Given the title, I thought it would be a quick read but it turns out to cover a variety of topics over its 200+ pages. So far, I like that it comes from the point of view of an experienced financial planner who spends his days talking with clients.

A valuable observation is that the most common financial mistake most people make is simply doing nothing. Either they are scared of what they might find, or they are overwhelmed by how hard it is to plan for something with such uncertainty. Future jobs and/or income? Uncertain. Childcare/Healthcare/Retirement costs? Uncertain. Future investment returns? Uncertain.

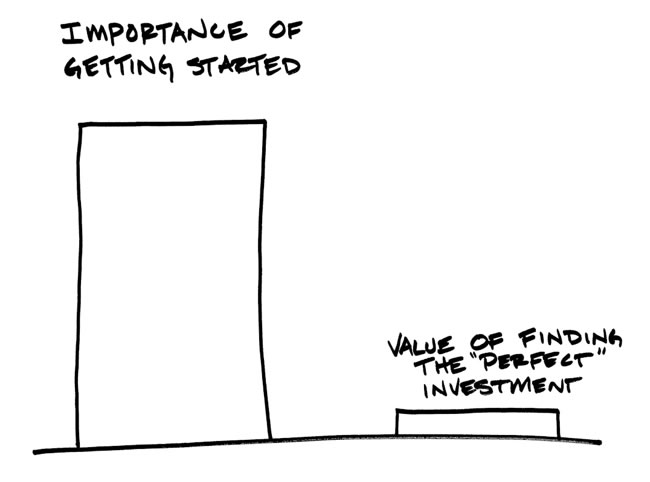

As a financial planner, his job is get people over this hurdle. Guessing is okay! You can always correct your course as you go along, but as long as you are facing the problem and doing something, you are much more likely to have a good result. Carl Richards is also known as “The Sketch Guy” and this one from the book illustrates things well:

However, you could replace “investment” with any decision that you have been putting off. Don’t worry about making mistakes (you will). Don’t worry about making the perfect or optimal decision (you won’t). Financial planning is not an exact science.

Here’s another take from inspirational speaker and writer James Clear in Why Getting Started is More Important Than Succeeding:

I can’t think of any skill more critical to the active pursuit of a healthy life than the willingness to start. Everything that signifies a happy, healthy and fulfilled existence — strong relationships, vibrant creativity, valuable work, a physical lifestyle, etc. — it all requires a willingness to get started over and over again.

Take note: being the best isn’t required to be happy or fulfilled, but being in the game is necessary.

Get started and correct your course as needed. In terms of personal finance, so many people have never drilled down to the real reasons why money is important to them, they have never calculated their net worth, never tracked and broken down their monthly expenses, and thus never properly prioritized their time, energy, and money accordingly. But that’s okay, as now is still a great time to get started! I have finished the book yet, but apparently you can fit an entire plan on one page. 🙂

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)