![]()

Automated portfolio managers like Wealthfront will set you up with a diversified mix of index funds and manage it for you for a small fee. I’m an investing geek, so I always lean towards keeping the small fee and manage things myself. But an important variable to this equation is tax-loss harvesting. Tax-loss harvesting tries to improve your returns by minimizing your tax bill, but it is also tedious work that is ideally suited to handing over to a computer.

If the management fee they charge is say 0.25%, as long as the benefit from tax-loss harvesting is at least 0.25%, then you’re already ahead of the game. The problem is that predicting the actual benefit of TLH is difficult. Wealthfront claims that based on past data, their tax-loss harvesting implementation could add 1.55% annually to your after-tax returns. Here is their whitepaper showing the assumptions they used to get that number.

Up until recently, you also needed $100k in your portfolio. But Wealthfront has recently announced that as of April 2015, their daily tax-loss harvesting service will be available to all taxable accounts with no minimum balance requirement:

We’re proud to announce that our daily tax-loss harvesting service will be made available to all Wealthfront taxable accounts, starting in April. At Wealthfront, we believe everyone deserves sophisticated financial advice, and this brings us one step closer to that goal.

I would not have predicted this a few years ago: automated tax-loss harvesting for any account size and at such a low cost. A customer with just $500 would be getting TLH and portfolio management for free. (As of February 2017, the minimum needed to open a Wealthfront account is only $500.)

I would say that I am confident the benefit of TLH over the long-run will be greater than zero. However, I would not count on 1%. But even if we split the difference and assume it is 0.5%, then using such a service still has to be considered as it is greater that their management fee of 0.25%.

Current sign-up promotions. The standard fee schedule for Wealthfront is that your first $10,000 is managed for free. Assets above that are charged a flat 0.25% fee annually. With a special invite link, you can get your first $15,000 managed for free, forever (an additional $5k). You can then invite your own friends (they get another $5k managed for free, and you get another $5k managed for free.)

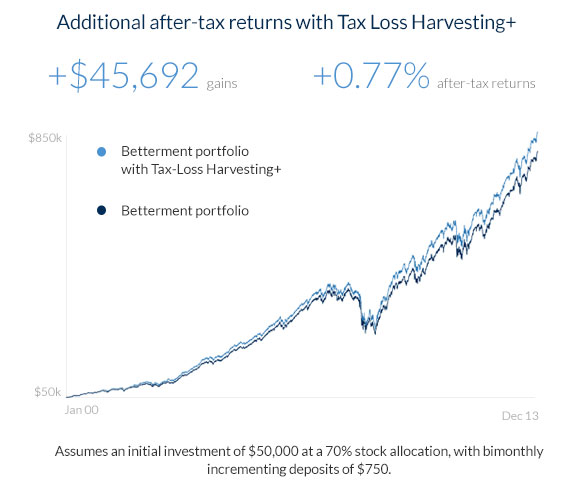

(Note: Competitor Betterment also has a similar tax-loss harvesting service. The post structure is similar, but I wanted to make sure any readers that may see only one post get the full context.)

Here’s a reader question that arrived this week:

Here’s a reader question that arrived this week: The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)