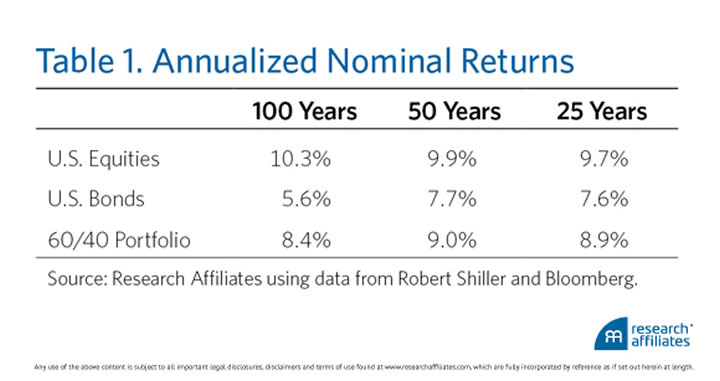

Via The Reformed Broker, investment manager Research Affiliates shares how a simple, balanced 60/40 portfolio (specifically 60% S&P 500 stocks, 40% 10-Year US Treasuries) did pretty darn good in the past 100, 50, and 25 years:

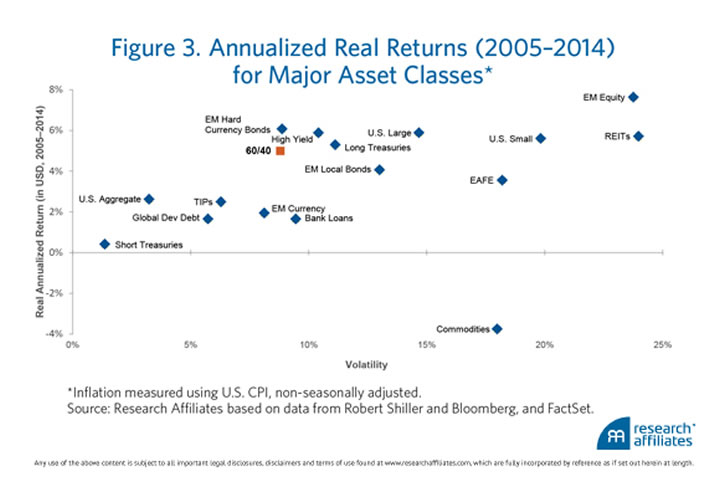

It even did well over the last 10 years, considering that “blip” we had in 2008. The 60/40 portfolio outperformed 9 of 16 core asset classes, all while maintaining lower-than-average volatility.

Of course, they also predict (using sound reasoning, in my opinion) that the same 60/40 portfolio will only produce a 1.2% inflation-adjusted return for the next 10 years. Still, I don’t know of any better options.

Vox has an

Vox has an  During the most recent State of the Union address, the President’s proposal includes removing one of the current key tax advantages for 529 college savings plans. It is important to remember that this is only a proposal and is unlikely to pass a Congress with a Republican-majority. But it does serve as a reminder that the features of all tax-advantaged accounts are subject to future change.

During the most recent State of the Union address, the President’s proposal includes removing one of the current key tax advantages for 529 college savings plans. It is important to remember that this is only a proposal and is unlikely to pass a Congress with a Republican-majority. But it does serve as a reminder that the features of all tax-advantaged accounts are subject to future change.  Apple

Apple

If you have self-employment or other income outside of your W-2 paycheck this year, you may need to send the IRS some money before the usual tax-filing time. Here are the due dates for paying quarterly estimated taxes in 2015; they are supposed to be in four equal installments. This is for federal taxes only, state and local tax due dates may be different.

If you have self-employment or other income outside of your W-2 paycheck this year, you may need to send the IRS some money before the usual tax-filing time. Here are the due dates for paying quarterly estimated taxes in 2015; they are supposed to be in four equal installments. This is for federal taxes only, state and local tax due dates may be different.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)