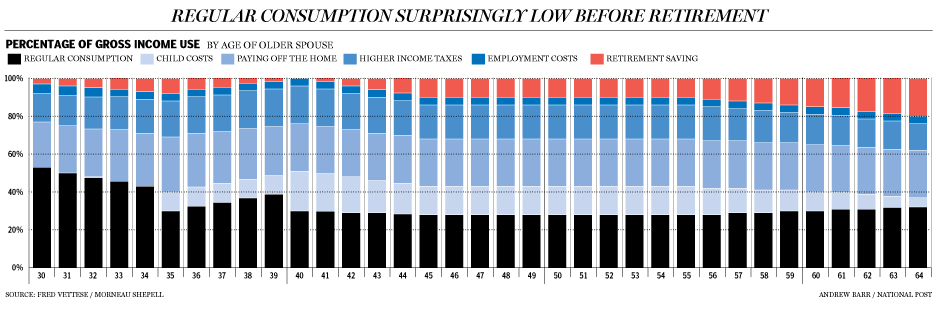

Common retirement planning advice tells you to plan on replacing 70-80% of your pre-retirement income. However, this Financial Post article argues that number may be closer to 35%. Article found via k66 of Bogleheads.

Essentially, the author segregates your income to “regular” spending and temporary “investment” spending that won’t continue into retirement. Regular consumption includes food, transportation, home and car maintenance, and insurance. Temporary spending include a mortgage, child-related costs, work-related costs, and retirement savings. The idea is that in retirement your house will be paid off and your kids will be financially self-sufficient, so those “investment” expenses will go away and you’ll need less money than you may think.

Here’s an illustration of how this would break down for a theoretical couple that bought a house at 30, had kids at 35, and retires at 65.

(click to enlarge)

Now, it’s easy to get hung up on how this chart doesn’t accurately reflect your life. It’s not supposed to! Instead, imagine for yourself what this chart might look like for your situation. For example, my parents definitely kicked up their savings rate post-kids and pre-retirement. For us, we had our highest savings rate pre-kids. You may need 20% of your current income, or you may need 80%. This is one place where a rule-of-thumb just isn’t useful.

I would note that the article doesn’t really mention health insurance or other health-related costs, possibly because it is a Canadian newspaper. Also, young people in the US probably spend at least a few years paying down college loans. Finally, some folks will need to account for new post-retirement spending that might pop up like travel and other costly recreational activities.

Consider the following questions that you may have asked yourself recently:

Consider the following questions that you may have asked yourself recently: (Update: Free promo is expired, it’s back at $9.99.) Just a quick note that there is a Kindle eBook about tax deductions for small businesses, including self-employed people, that is currently free called Small Business Tax Deduction Secrets by Stephen Nelson, CPA. The author participates in the

(Update: Free promo is expired, it’s back at $9.99.) Just a quick note that there is a Kindle eBook about tax deductions for small businesses, including self-employed people, that is currently free called Small Business Tax Deduction Secrets by Stephen Nelson, CPA. The author participates in the  A common piece of advice I’ve heard is “Take risks while you’re young.” This is often applied to personal finance, in terms of trying to land a higher-paying job, starting a new business, or pursuing your passion. The thinking goes something like this:

A common piece of advice I’ve heard is “Take risks while you’re young.” This is often applied to personal finance, in terms of trying to land a higher-paying job, starting a new business, or pursuing your passion. The thinking goes something like this: Speaking of

Speaking of  I’ve read a few books about dividend investing and remain interested in the idea, although I’m not confident enough (yet?) to allocate my portfolio that way. Portfolio manager and writer Mebane Faber has a short book called

I’ve read a few books about dividend investing and remain interested in the idea, although I’m not confident enough (yet?) to allocate my portfolio that way. Portfolio manager and writer Mebane Faber has a short book called  Ever since we started cutting back our work hours in order to share childcare duties, Mrs. MMB and I have kept a closer eye on our monthly spending patterns. One of the headaches for budgeters is dealing with large lump-sum payments like those for home/car repairs, healthcare bills (human repairs), and home/car/life insurance. Our homeowner’s insurance is due annually (we don’t use mortgage escrow anymore), life insurance is due annually, and auto insurance is due semi-annually.

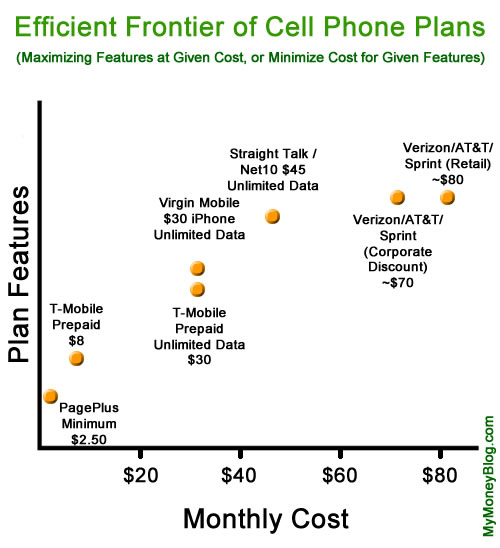

Ever since we started cutting back our work hours in order to share childcare duties, Mrs. MMB and I have kept a closer eye on our monthly spending patterns. One of the headaches for budgeters is dealing with large lump-sum payments like those for home/car repairs, healthcare bills (human repairs), and home/car/life insurance. Our homeowner’s insurance is due annually (we don’t use mortgage escrow anymore), life insurance is due annually, and auto insurance is due semi-annually.  The other day while I was trying to help someone find a cheaper cell phone plan, I realized two things:

The other day while I was trying to help someone find a cheaper cell phone plan, I realized two things:

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)