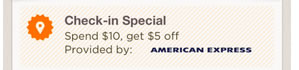

Update: Foursquare and American Express are running this promotion again nationwide – even if you did it already previously – this time for $5 off $10 at participating small businesses. I just looked for restaurants nearby that accepted AmEx and found several that are eligible = another cheap date night! Just “check-in” and you can load the discount onto your linked credit card. Thanks EC for the tip.

Foursquare is a location-aware smartphone app where you can “check-in” at specific places and share information. First, connect your foursquare account to any eligible American Express Card at sync.americanexpress.com. Then follow the quoted directions below on your smartphone. I want to say that all this should work with an iPod Touch or iPad as well, but I haven’t tried.

Check in at a merchant with a Special, load the Special to your card, and then pay for your over $10 purchase with your American Express ® Card. No need to show your phone to a cashier or anything – you’ll receive the credit on your Amex statement within 5 business days. You can find dozens of deals in your area just by hitting ‘Specials’ on the ‘Explore’ tab on your foursquare app (there are hundreds of thousands of participating businesses).

p.s. You can still score free points from Hilton Honors and other rewards programs by “checking in” using the Foursquare app when you register with TopGuest. You can get 50 Hilton points every day you check in at a Hilton hotel, for example. You only need to be within 10 miles of the hotel to check in the first time, and in future times you need to be nearby at all. I can check in once a day, every day, for 50 points, although I usually forget to.

Speaking of credit card rewards optimization, I was thinking about how the algorithm might work for me. I’m curious if others have a similar system. Man, I have a lot of cards…

Speaking of credit card rewards optimization, I was thinking about how the algorithm might work for me. I’m curious if others have a similar system. Man, I have a lot of cards… Do you dream of working for yourself instead of “The Man”? Indeed, early retirement and/or financial independence is often achieved by successful small business owners. In addition, any retirement plan will be more robust if you can earn some extra money on your own as needed. As such, I definitely support the growth of freelancers doing their own thing. However, you may hit roadblocks like loneliness, distractions at home, or lack of resources.

Do you dream of working for yourself instead of “The Man”? Indeed, early retirement and/or financial independence is often achieved by successful small business owners. In addition, any retirement plan will be more robust if you can earn some extra money on your own as needed. As such, I definitely support the growth of freelancers doing their own thing. However, you may hit roadblocks like loneliness, distractions at home, or lack of resources.

Since I spent July 4th trying to build my own

Since I spent July 4th trying to build my own

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)