Charlie Munger is best known as the long-time friend and business partner of Warren Buffett, and officially as the Vice-Chairman of Berkshire Hathaway. Even though he is Buffett’s partner in investing, Munger is different in that he does not enjoy the spotlight as much and is rather more blunt and cranky. For some reason that just makes me like him more. 🙂

Charlie Munger is best known as the long-time friend and business partner of Warren Buffett, and officially as the Vice-Chairman of Berkshire Hathaway. Even though he is Buffett’s partner in investing, Munger is different in that he does not enjoy the spotlight as much and is rather more blunt and cranky. For some reason that just makes me like him more. 🙂

Ever since I read more about him in the Buffett biography The Snowball, I have wanted to learn more about him via the book Poor Charlie’s Almanack: The Wit and Wisdom of Charles T. Munger, which is mostly a collection of his speeches but also includes some of his own personal notes and reflections from his peers and family. From the website:

For the first time ever, the wit and wisdom of Charlie Munger is available in a single volume: all his talks, lectures and public commentary. And, it has been written and compiled with both Charlie Munger and Warren Buffett’s encouragement and cooperation. So pull up your favorite reading chair and enjoy the unique humor, wit and insight that Charlie Munger brings to the world of business, investing and life itself.

The first thing you should know about this book is that it is not meant to be an investing How-To book. Yes, there is a lot of investing advice in it, but the book is more about how to live a successful and fulfilling life more than the accumulation of money. Munger puts more emphasis on integrity and how to think correctly than how to calculate a company’s return on capital.

Financial Independence

One of the reasons that Buffett and Munger appeal to me is that their primary motivation for doing what they do is not simply to be rich, it is to to be independent. Here’s a quote from Buffett on why he wanted to make money: [Read more…]

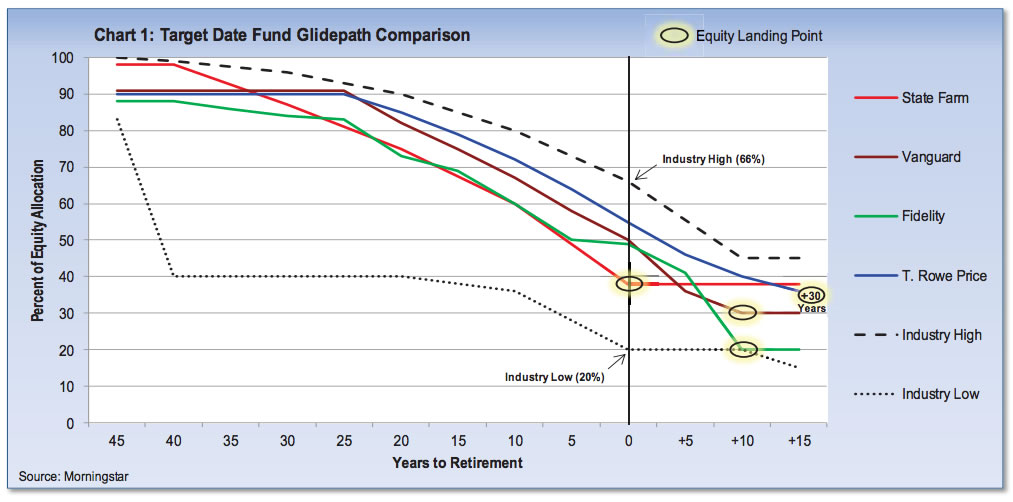

Vanguard has

Vanguard has  Here are a few promotions from Amazon that can save you some time and/or money.

Here are a few promotions from Amazon that can save you some time and/or money. The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)