After my post counting down my years until early retirement earlier this week, I received a very thoughtful e-mail from reader Tim:

I’ve been reading and enjoying your blog for a long time, and think it’s one of the best out there for your mix of personality, short-term and long-term financial tips and advice. But one thing bothers me: the ongoing, almost central theme (obsession?) with early retirement. It seems to be the goal around which everything else in the blog revolves and leads toward.

Why is that? Do you hate your job so much, and can’t even imagine a job you would enjoy enough that you would want to do it whether you were paid or not? It doesn’t strike me that someone as industrious, curious and intellectually active as yourself would really ever retire. I understand there may be other activities you’d like to pursue, but my guess is that most of them would be potentially income-generating. So you’d still have a “job.” And if that’s the case, then why not pursue one or more of those things now, rather than delaying them until “retirement?”

It seems to me that “MyMoneyBlog” is likely one of those things, and I’m very glad you’re doing it. And if one reason is the hope to fully monetize the blog to the point of retirement from your nine-to-five job, then I hope you do that too.

But still, something about that recurrent theme of retiring just leaves me with a hollow, dead feeling in the pit of my stomach, as if we’re all inmates marking time on the wall of a dreary prison cell until our release. Maybe it’s the implied resignation to the assumption that joyless jobs are unavoidable – a bitter fact of life – that I reject. I just don’t like to think that as a society we accept a lifetime of delayed gratification as a given, and don’t rouse ourselves to do anything more about it than make sound financial plans to enjoy ourselves when the pain finally stops.

There are some great questions in there, and really it also showed me that I can improve on explaining my philosophies. I have all these ideas rattling around in my head, and not all of them reach the keyboard. My reply became rather long…

Definition of early retirement. I know that retirement is a very tricky word to use. For too many people, it conjures up images of playing golf and sitting around all day. Financial independence or financial freedom are better terms, and they all mean the same thing to me – I get to do whatever I want. Cook a new dish every day, rebuild a Land Rover Defender or Willys Jeep, volunteer, spend a year abroad, anything. F— You money.

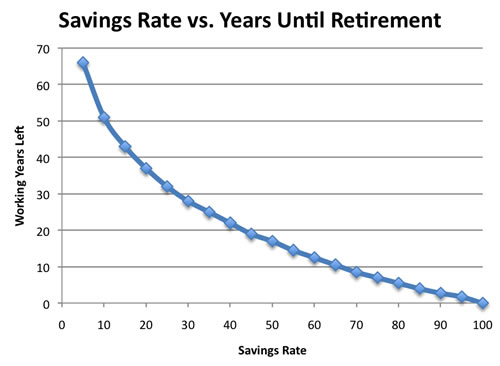

Delayed gratification. Going back to the early retirement curve, a major assumption is that your current expenses are the same as your future expenses. Let’s say your household earns $80k and lives on $40k. Well, that curve assumes you’ll be living on $40k in “retirement” as well. Using a food analogy, getting there is not a crash diet, but requires a permanent change to healthier eating habits. I don’t feel deprived with my current lifestyle as it pertains to spending, otherwise it wouldn’t be sustainable.

A job that I would do forever? I’ve thought about this. Let’s try to design the best job possible. To start, it should satisfy this Career Venn diagram which reminds us to seek the intersection of things that we do well, things that pay well, and things we like to do. In addition, it should provide all the factors that make a job satisfying beyond money: autonomy, complexity, and a connection between effort and reward.

Does my current job cause me pain? Does my wife’s job? Not really, we are white-collar professionals so we have a certain degree of autonomy and challenge to our work. But we also have managers, meetings, clients, and politics.

Is there any such ideal job that exists? Honestly, if it had to pay $50k a year and 40 hours a week, probably not for me. I am the type of person that likes to do something for a while, and then move on to something else. Even self-employment has it’s own set of restrictions. Even though blogging is a sweet gig :), having income that depends on advertising is very volatile.

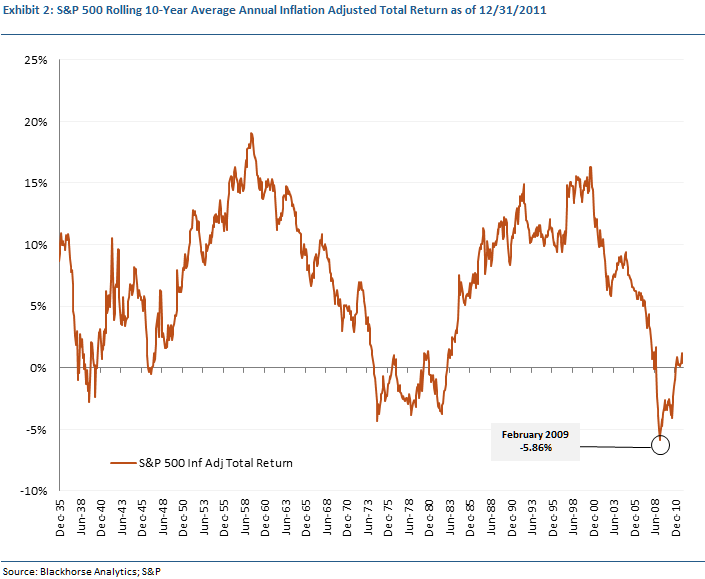

This is where financial freedom comes in, because it means more flexibility. I have realized over time that I will probably need to do something, and that is a big reason why I am happy with a 4% safe withdrawal rate. All the academic studies that calculate this withdrawal rate stuff assume that a theoretical person blindly takes out 4% inflation-adjusted to the CPI every single year. From reading experiences of real early retirees, they adjust and adapt.

Let’s say we want that 4% withdrawal rate to create $40,000 of income from investments, but it ends up that 3% is a more reasonable number. Now, I need to find a job that pays $10,000 a year. I could do all kinds of things that would be kind of cool for $10,000 a year, and I wouldn’t have to work 40 hours a week either. I could do just about anything – web design, tutor high school or college students, teach English in a foreign country, apprentice with a skilled craftsman, or work as a travel guide.

Indeed, the possibilities are endless. One day, if the stars align, we will have children. At that point, we plan on downshifting to working part-time so that we can both enjoy raising kids without all the financial stress that our parents had. Our portfolio can already cover half of our expenses. Once the kids go to school, there will be more time for work, if needed. In the end, I would say that I am obsessed with freedom and autonomy.

If you’re the person in your family or circle of friends that always seems to be asked computer questions, or are simply the person asking for help, what you really need is software that allows remote access between computers. That way, you can diagnose and fix problems from across the country without having to leave your desk.

If you’re the person in your family or circle of friends that always seems to be asked computer questions, or are simply the person asking for help, what you really need is software that allows remote access between computers. That way, you can diagnose and fix problems from across the country without having to leave your desk.

Updated with current price quotes for 2012!

Updated with current price quotes for 2012!

The Treasury

The Treasury

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)