Recently, I came across an investment tip called the Overnight Rule from Carl Richards via the NYT Bucks Blog:

Recently, I came across an investment tip called the Overnight Rule from Carl Richards via the NYT Bucks Blog:

Imagine that all your investment holdings were sold overnight by accident.

You can’t undo the trades, and now all you have is cash.

Would you buy back everything you owned previously again at their current prices? If not, why are you holding them now?

I think this provides a fresh look at your portfolio, as many times we hold investments for irrational reasons. For example, there is the well-documented trait of loss aversion (even though readers of this blog may be immune), where investors really hate selling at a loss, even more than they love selling with a gain.

Perhaps you bought the stock at $20 a share, and it is now at $15 a share. You want to get rid of it “just as soon as it gets back to $20 a share”, so that so you can say you didn’t lose money on it. It’s better to admit the mistake and put your money in something better.

Then there is regret aversion. Perhaps you bought it at $50 a share and now it’s at $400 a share. You get to tell your friends how you bought Apple at $50 a share. You’re afraid it’s overpriced, but you don’t want to miss out if it rises some more. You sit on your gains and choose inaction instead of having to make a hard decision even though your money could be better deployed elsewhere.

Maybe it is company stock from your job, or shares that you inherited from a beloved family member. Whether is it some form of sentimental attachment, inertia, or plain laziness – you may want to consider your reasons for holding them.

There is a small exception to this rule if you are sitting on large capital gains in a taxable account and don’t want to realize them and get hit with the tax bill, especially if the alternative investment is also very similar (ex. mutual funds with similar holdings). However, even in this scenario you want to make sure that you’re not holding a poor investment just to put off a tax bill.

I did not come up with this myself, but read about this rule somewhere online within the last month. I’ve searched for the source but can’t find it, so please let me know if you do. Found it, thanks!

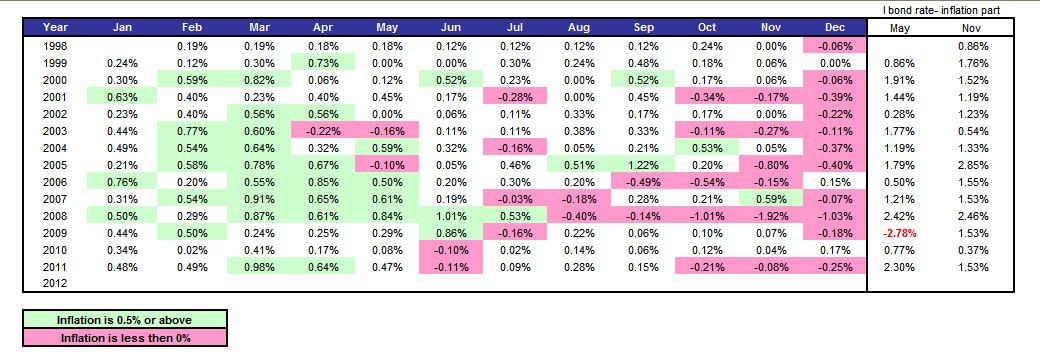

(In this post, I’m not going to provide all the background information on savings bonds that I normally do. For that, please read the older posts in my

(In this post, I’m not going to provide all the background information on savings bonds that I normally do. For that, please read the older posts in my

You’re probably aware of the wonders of the

You’re probably aware of the wonders of the  Clover is a new person-to-person payment system for use between phone numbers. Simple fees (none for personal use), simple interface. If you sign-up via invite from a registered user, you’ll get up to $10 off your first purchase. The referrer gets $5 too. You don’t even need a credit card or bank account to start, just a phone number (landline numbers work, but it’s optimized for Android and iPhone/iPod Touch users).

Clover is a new person-to-person payment system for use between phone numbers. Simple fees (none for personal use), simple interface. If you sign-up via invite from a registered user, you’ll get up to $10 off your first purchase. The referrer gets $5 too. You don’t even need a credit card or bank account to start, just a phone number (landline numbers work, but it’s optimized for Android and iPhone/iPod Touch users).

The Daily Beast has an article

The Daily Beast has an article  If you have some American Express Membership Rewards points lying around, perhaps from the

If you have some American Express Membership Rewards points lying around, perhaps from the

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}