There is a lot of uncertainty in investing, and it always seems like especially now. Buy and hold has been called dead many times. However, if you look carefully, you’ll find that there are many people who have quietly grown their portfolio over the last decade using the boring principles of diversification, low-costs, and regular rebalancing. I would also add proper tax planning helps as well.

Here is some data from a WSJ article by Burton Malkiel (author of Random Walk Down Wall Street) that helps illustrates this. (Can’t view the article? Use this Google the title trick and click the first link.) The article is from several months ago, but the S&P 500 index back then was almost exactly the same as yesterday: 1,193 vs. 1,195.

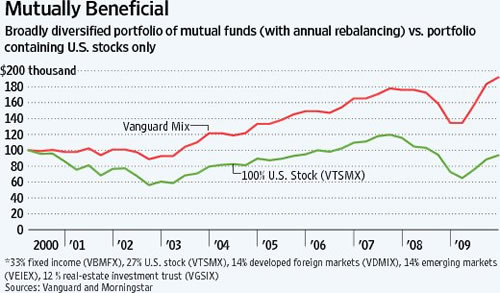

The chart below shows the growth of $100,000 invested at the start of 2000 until the end of 2009. As you can see, a 100% stock investment (in green) would have ended up at $93,717. Thus the term “lost decade for stocks”.

But what happens when you mix in some other assets, and rebalanced them annually? The red line is a portfolio consisting of 67% stocks and 33% bonds, all in low-cost index funds. The stock breakdown was 27% US, 14% Developed International, 14% Emerging Markets, and 12% REITs. The result was a ending balance of $191,859, which means an investor in 2000 could have, without special psychic powers, nearly doubled their portfolio over the same “lost decade”.

The diversified portfolio above matches rather well with my own asset allocation. For one, my AA also has 50/50 US/non-US split plus a chunk in REITs. Although I started out 85% stocks/15% bonds, I am now closer to 75% stocks. I have also rebalanced annually to maintain that ratio, but I do feel that my portfolio has still grown past my contributions even though I haven’t tracked my personal returns as well as I’d like.

Regular rebalancing is key. That is, keeping your target asset allocation by buying what is going down, and selling what is going up, in order to keep your desired risk profile. Both in early 2009 and last week, I was buying stocks. While there is debate on this, I believe that there is a reversion-to-the-mean effect that boosts your returns.

After the interest rate drama last week, I managed to lock in a refinance of my current 30-year mortgage (with 26 years left) which had a 4.75% fixed rate into a new 15-year mortgage at a 3.875% fixed rate. You’ll probably see lower rates in ads and elsewhere, but it did come with negative points that offset my closing costs completely and then some. Anyhow, I wanted to run the numbers to see the potential financial benefit.

After the interest rate drama last week, I managed to lock in a refinance of my current 30-year mortgage (with 26 years left) which had a 4.75% fixed rate into a new 15-year mortgage at a 3.875% fixed rate. You’ll probably see lower rates in ads and elsewhere, but it did come with negative points that offset my closing costs completely and then some. Anyhow, I wanted to run the numbers to see the potential financial benefit.

The Citi ThankYou Premier Card currently offers 30,000 bonus ThankYou Points after $2,000 in purchases within 3 months of account opening. That is enough to redeem for $300 in gift cards at stores including Walmart, Home Depot, Lowes, and CVS Pharmacy. Alternatively, you can get $399 in airfare or hotels when you redeem through their ThankYou Travel Center (prices match Expedia.com). If you redeemed for Walmart gift cards and exchanged them online at a site like

The Citi ThankYou Premier Card currently offers 30,000 bonus ThankYou Points after $2,000 in purchases within 3 months of account opening. That is enough to redeem for $300 in gift cards at stores including Walmart, Home Depot, Lowes, and CVS Pharmacy. Alternatively, you can get $399 in airfare or hotels when you redeem through their ThankYou Travel Center (prices match Expedia.com). If you redeemed for Walmart gift cards and exchanged them online at a site like  Reader Alison shares a unique savings account program for residents of Ohio. The SaveNOW program is a higher interest savings account supported by the state in order to encourage savings. The maximum balance on this account is $5,000 and pays 3.25% APY. The fine print regarding deposit limits is a bit confusing. It says:

Reader Alison shares a unique savings account program for residents of Ohio. The SaveNOW program is a higher interest savings account supported by the state in order to encourage savings. The maximum balance on this account is $5,000 and pays 3.25% APY. The fine print regarding deposit limits is a bit confusing. It says: Now that there is a

Now that there is a  This is the story of how I ended up buying an

This is the story of how I ended up buying an  The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)