I get a lot of credit card offers in the mail. I usually just junk them since they aren’t better than my current list of best no fee 0% APR offers, but this one caught my eye. The outside envelope mentioned “0% APR FOR LIFE” (emphasis their’s). I knew there had to be a catch, but I actually opened this one. I guess this is Discover Card’s new thing? Sorry, it looks to be a targeted mailing, so no online application link to the offer.

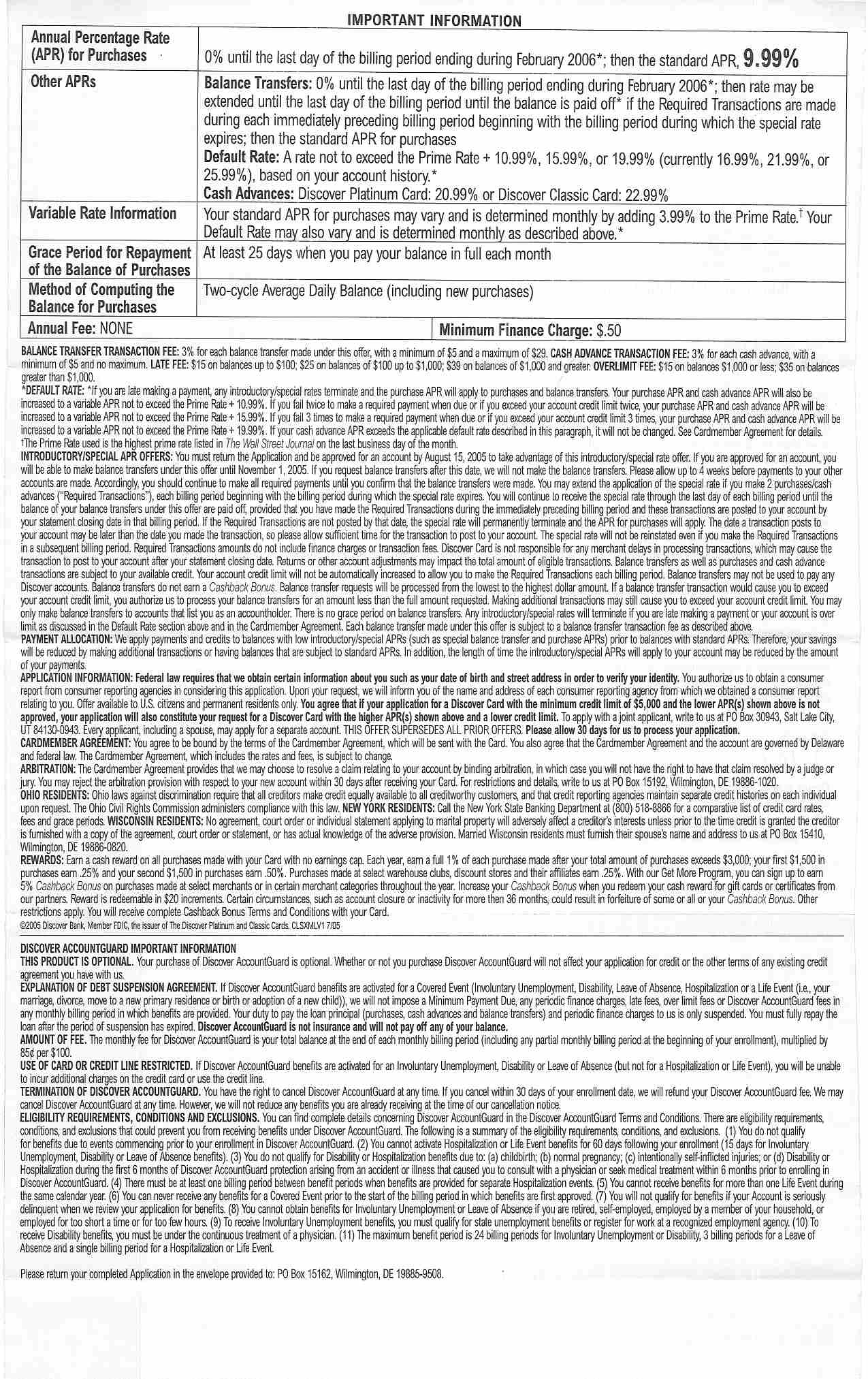

The terms of my offer are as follows: 0% APR on balance transfers until 2/06. The 0% APR can be extended for the life of the balance if I make two purchases or cash advances each billing period. The balance transfer transaction fee is 3%, with a minimum of $5 and a max of $29. This offer seemed juicy enough to crunch some numbers…

First off, the $29 max balance transfer fee is not that bad. If I manage to get at a least a $10,000 credit line, that’s only .29% of the balance or less.

Of course, the main catch is if you make a purchase on the account to extend the introductory 0% offer, any payment you make to the account will be applied to the balance transfer first. Basically, you can’t pay off your purchases until you pay off your balance transfer, which would defeat the whole thing. Thus, you’ll be paying interest charges on your purchases. The purchase APR is variable at 3.99% + Prime Rate. Right now that’d be 6.25 + 3.99 = 11.24%. There is also a minimum finance charge of $.50, and no annual fee.

So let’s see. There is no minimum amount, so if I charge $1 twice a month at the gas pump or at the grocery store, that’d be $2/month. I’d be charged 50 cents interest per month until my purchases got above $53.3 (assuming constant interest rate for simplicity), or about 2 years. For those 2 years, I’d only pay $12 in finance charges? Of course that will continue to rise, but this is sounding good.

What’s another big catch I found? The two transactions have to *post* to your account within the billing period. Just because you bought something on one day doesn’t mean it will *post* the same day or even within the next few days. “Discover Card is not responsible for any merchant delays in processing transactions, which may cause the transaction to post to your account after your statement closing date.” Hmm… how are we supposed to track that? You’d have to be pretty digilent, making the purchases near the very beginning of your statement cycle. I’m thinking $1 at Shell, then another $1 immediately at Chevron down the street. Say, every month on the 5th or whatever…

One other variable is what is the minimum payment every month? If it is 2%, it will take 50 months to pay off the balance, so the FOR LIFE part really just means two years. But since this offer is already good until February 2006 without any purchases, we’re looking at until February 2008. With the current interest rate outlook, this is very interesting… I’m calling tomorrow about the minimum payment, it’s late and I’m too tired from combing through fine print right now…

Anyone out there doing this besides Ian? Anything I missed? Does American Express, Visa, or Mastercard offer something similar? I scanned and uploaded the Terms & Conditions here (warning, it’s big) for those interested.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}

I have a similar offer from discover.

I guess i got it last year when they were still experimenting with the terms

My terms require me to make ONLY one purchase.( no minimum amount )

So i buy a pack of gum ( 0.20 Cents) or a cup of yoghurt (38 cents ) from walmart & meet my obligation.

I think the minimum payment is 2% or somewhere close to that.

I got a couple of these offers earlier this year and finally one with good terms came along, I took a shot. The only difference in my case was unlike most who do these offers to make a few bucks off the interest, I did it to try to tackle some outstanding debt on another card with a not so attractive rate.

Except for a slight rocky start, I have been pretty happy with the whole experience so far. My purchasing requirements are about to start and they sent a nice reminder note about it along with the usual tips and warnings about the merchant delay potential.

Also, 2% is my minimum payment.

I am looking to get the same offer, do you have any contact info for their marketing department, or is their any identifiying feature of the card?

As of right now I’m just crossing my fingers hoping it appears in my mailbox.

Question, do you currently have a discover card or is this an offer for new cardholders?

Hey Jonathon,

Has having all these different cards impacted your credit score? I read a lot of blogs where people are doing similiar things (especially the 0% apr and then investing the money for a gain of about 3% on someone else’s money).

I can’t help but think that the credit bureaus will knock down your credit score over time. Is this not correct?

Thanks

Hazzard

http://elym.blogspot.com

Thanks all, I called and the minimum payment is 2%, not bad. I’m going for it.

Beau, I do not have Discover card now, not sure if it’s for new cardholders. I used to have one. I would call 1-800-DISCOVER and ask. If needed, you can try to cancel your card and see if they’ll try and keep you with a better offer. Be careful though, I did this once and they just cancelled the card =(

Hazzard, yes it does hurt your credit score somewhat, but if you have a good amount of credit limit then your overall credit utilization isn’t that high and it’s not that bad. I wouldn’t be doing many of these if I was loan-searching unless I had some awesome FICO scores.

crap, I got overzealous in deleting a “easy money” spam comment that others got deleted too. Sorry! I think one was ATF warning of the two-cycle billing system, which is definitely a good caveat that I just learned about and will be posting about in a bit. I think the other one was just saying thanks for the lovely story. Again, sorry!

I have been doing this for 2 years with one Discover call that only requires 1 purchase a month and for 1 year and 9 months with another discover card that requires 2 charges a month. I’ve been doing the gas pump thing the entire time and thus far have been very happy with the results – 0.50 charge every month.

Note that the 2% minimum payment applies to the current balance, so I can still myself doing this with my balances for years to come.

Hi everyone, this may be a bit off topic, but I am curious. Obviously many people out there get stressed when dealing with their finances. I know I do at times. I’m wondering how you relax and take your mind off it all. I know I like to read or start some sort of home improvement project (do-it-yourself). Right now I’m reading a great book from Ken Ratcliffe called Manhook. Anyone know it? What do you all do?

Hi, seems this forum thread hasn’t been used recetly so I hope you all are still checking in from time to time. I don’t have any debt but need some cash and want to find the cheapest way to get it. 10K-50K would work best. Thing is that cash advances on these cards seems high. Anyone get good offers on low or 0% apr on cash advances for life of loan? Thx

Please read this series of posts on how to get cash from credit cards:

How to get cash out

And then check out this post of NO-FEE balance transfer credit cards at 0%. There are some really good offers still going on now.

No fee credit cards

Hope that helps,

Jonathan

Its simply a real good deal. I have this Card and started with a $9000 balance. It requires me to make a minimum of two $1 charges per month to keep the 0% going month after month forever. I can simply tell you this, I average charging $20 per month on the card and simply making my minimum payment for 18 months which has been between $150 to $160 have paid this card down to the current balance of $6500. I feel its a very good deal. It’s common sense that if your paying no interest on the transfer and only interest applies to your charges as long as you keep the charges low such as I’m doing than there will be very little interest and your paying much more to the principle.

I’m buying small purchases $1-$2 every Sunday, because of that posting question. As a matter of principle, I’m also trying to get items that I still will be using in 5 years, so I’m not paying even small interest on “edibles”. It’s an interesting challenge and is working so far. At some point I might have to resort to the pack of gum.

I got the same offer, 2 transactions every month. Last month, I forgot to make two transactions and fortunately they gave me more one last chance and extended the offer. Does anyone know an automatic monthly subscription that I can charge on my credit card which costs me less than a buck. Thanks for your help

I am so disappointed. I thought I had the same offer last year for January 2006 and my balance would be 0% for the life of my loan. My husband thought that offer was too good to be true. I thought my offer ended in September, so I called and was told that it ended in February, but I only got the 0% for one year. When the customer person checked, he told me he found my offer and would make sure it was noted. Now I call to make sure I know my posting dates, and guess what, no record that I got this offer just the 12-0% offer. I did not know about this 0% for life until I got it in the mail. I think they did a bate and switch on me.

I had the same thing happen to me recently. This month when I went to pay my monthly bill, I noticed a finance charge and was very upset. I looked everywhere to find the letter that had the offer on it so I could use it to prove my case but was unable to locate it. So, I began searching on-line to see if I could find some proof that this offer really did exist. I’m glad I found this blog today so I had some ammunition to use when I called to complain. I called Discover and was told that indeed I had that offer and I kept up with my end of the deal by making multiple charges each month. Their rep states that she could not explain why this happened but said it would be corrected and all finance charges would be credited on the next statement. I certainly hope so!! I think that they figure that a good number of people will never complain and just pay the interest. I will let you know if they follow through with their claim.

I got Dicsover card a year ago with 0% APR for life time of balance transfer, and the only time I had my 0% APR cancelled is because I made my 2nd purchase a month too close to the end of billing cycle. That was my mistake, and they were nice enough to reinstated my offer since it was my first time. I am being very careful to make my purchases in the middle of billing cycle. I am looking for an offer like that on internet for one of my friends, and so far no luck. Does anyone knows if it became available on line or it’s only through mail?

I guess they’re counting on the lack of self-disapline most people in this world have. Sounds like you’re happy with the card, though. Wouldn’t you just hate it if you accidentaly paid the dentist with your 0% for Life Discover card? Thanks for blogging.

RAJ – Have Jonathon set up a paypal subscription for all the great advice this site gives.

Hi All.

Can someone please tell me if I got these numbers correct assuming I purchage 2 items (gums) at $1.00 each every month at 15% interest.

It seems harmless at first, but it goes up quickly. By year 4, you owe more than 10k buy charging $2 gums a month.

So the first month, I have $2.00 charge plus .30 interest. Next month I have $4.30 (another $2.00 plus 2.30 from previous month) PLUS .65 cents interest. This cycle repeats for 4 years:

Year (1)

Balnace = 2.00 0.30

Balnace = 4.30 0.65

Balnace = 6.95 1.04

Balnace = 9.99 1.50

Balnace = 13.48 2.02

Balnace = 17.51 2.63

Balnace = 22.13 3.32

Balnace = 27.45 4.12

Balnace = 33.57 5.04

Balnace = 40.61 6.09

Balnace = 48.70 7.30

Balnace = 58.00 8.70

Year (2)

Balnace = 68.70 10.31

Balnace = 81.01 12.15

Balnace = 95.16 14.27

Balnace = 111.43 16.72

Balnace = 130.15 19.52

Balnace = 151.67 22.75

Balnace = 176.42 26.46

Balnace = 204.89 30.73

Balnace = 237.62 35.64

Balnace = 275.26 41.29

Balnace = 318.55 47.78

Balnace = 368.34 55.25

Year (3)

Balnace = 425.59 63.84

Balnace = 491.42 73.71

Balnace = 567.14 85.07

Balnace = 654.21 98.13

Balnace = 754.34 113.15

Balnace = 869.49 130.42

Balnace = 1001.91 150.29

Balnace = 1154.20 173.13

Balnace = 1329.33 199.40

Balnace = 1530.73 229.61

Balnace = 1762.34 264.35

Balnace = 2028.69 304.30

Year (4)

Balnace = 2335.00 350.25

Balnace = 2687.24 403.09

Balnace = 3092.33 463.85

Balnace = 3558.18 533.73

Balnace = 4093.91 614.09

Balnace = 4709.99 706.50

Balnace = 5418.49 812.77

Balnace = 6233.27 934.99

Balnace = 7170.26 1075.54

Balnace = 8247.80 1237.17

Balnace = 9486.96 1423.04

Balnace = 10912.01 1636.80

Another thing I forgot to ask: Where is the cheapest place one can make a charge or contribution?

I am looking for under 1 dollar – does it exist? Is available on-line? If we can find a place that will accept a .25 discover charge, that would help.

Joe, you do have it right (with the exception that Discover charges a minimum finance charge of fifty cents). But there are a couple things to keep in mind:

1) You don’t have to charge $2/mo. You could charge two $0.25 packs of gum. This will bring your balance in month 48 down quite a bit.

2) BUT… assuming your numbers, the $1636.80 you’ve paid in interest is a very small percentage of what you COULD be paying.

Let’s say, for example, you kept $25,000 on the credit card that a very respectable rate of 9.99%. If you paid it off over 48 months, you’d end up paying $5,429.

By using the Discover 0% offer you save $3,792. That’s $79/mo. for the trouble of remembering to make two small charges a month. For me that’s a cable TV bill.

Maybe someone can help me figure out if I’ve answered Joe’s question correctly. Is it possible to pay off the finance charges each month, or do they get added to the higher APR balance? In month 12, is the high APR balance $24 or $58?

Joe – I’m afraid your numbers are not correct. The interest rate, say 15%, is not charged every month. It is an annual interest rate. Each month you’ll be charged 15%/12. For many months, you will simply be subject to the minimum finance charge of 50 cents or whatever is listed on the fine print.

Finance charges are usually categorized as purchases, and are thus at the higher APR for these kinds of offers.

—

For cheap purchases, try the post office, you can buy a stamp from their automatic machines for 37 cents with credit card.

Keep in mind, these offers vary by each people. Some have minimum purchase amounts of $1 or $2 or whatever.

(Thanks for the math lesson, Jonathan. Some of us are a little dense! 🙂

I knew it sounded like a lot of interest, but for some reason it wasn’t registering that the calculation was being made using a 180% APR.

BTW – according to the offer I’ve seen, wouldn’t the rate by 11.99, not 15%?

Thanks guys for the correction on the math. The APR is Anual percentage rate, so yes, I forgot to take the 15% and divide it by 12.

The numbers now come out much more resonable. Also, you are correct that the minimal finance charge is .50 cents. I will post another listing later for others to see/comment.

That’s a good ide about charging a stamp with Discovered card. Mine has no minimum, but it requires 2 purchaes a month.

Anyone know of an AUTOMATED way to have the card be charged? 🙂

Oh, one more question.

There is a $50 dollar charge for balance transfers (2% or $50 max of transfer amount).

So if I transfer $5,000, my new balance will be $5,050. Anyone knows if that $50 charge gets the 0% APR for life or the higher APR?

In my case, new purchases are at 15%. So I know when I buy my 2 $1 items a month, that the $2.00 bucks will be charged at 15%.

But the BIG question is will the $50 bucks transfer charge fee be hit with 15% or with the 0% APR?

Ok, here is another table with the CORRECT Apr 15% divided by 12 months. I looks a lot more reasonable.

Also, I made corrected the minimum finance charge to be .50

Year (1)

Balnace = 2.00 0.50

Balnace = 4.50 0.50

Balnace = 7.00 0.50

Balnace = 9.50 0.50

Balnace = 12.00 0.50

Balnace = 14.50 0.50

Balnace = 17.00 0.50

Balnace = 19.50 0.50

Balnace = 22.00 0.50

Balnace = 24.50 0.50

Balnace = 27.00 0.50

Balnace = 29.50 0.50

Year (2)

Balnace = 32.00 0.50

Balnace = 34.50 0.50

Balnace = 37.00 0.50

Balnace = 39.50 0.50

Balnace = 42.00 0.52

Balnace = 44.53 0.56

Balnace = 47.08 0.59

Balnace = 49.67 0.62

Balnace = 52.29 0.65

Balnace = 54.94 0.69

Balnace = 57.63 0.72

Balnace = 60.35 0.75

Year (3)

Balnace = 63.11 0.79

Balnace = 65.90 0.82

Balnace = 68.72 0.86

Balnace = 71.58 0.89

Balnace = 74.47 0.93

Balnace = 77.40 0.97

Balnace = 80.37 1.00

Balnace = 83.38 1.04

Balnace = 86.42 1.08

Balnace = 89.50 1.12

Balnace = 92.62 1.16

Balnace = 95.77 1.20

Year (4)

Balnace = 98.97 1.24

Balnace = 102.21 1.28

Balnace = 105.49 1.32

Balnace = 108.80 1.36

Balnace = 112.16 1.40

Balnace = 115.57 1.44

Balnace = 119.01 1.49

Balnace = 122.50 1.53

Balnace = 126.03 1.58

Balnace = 129.61 1.62

Balnace = 133.23 1.67

Balnace = 136.89 1.71

Year (5)

Hi.

My Discover card credit limit is 6,500 and they wont raise it. My American Express is at 4.99% and they gave me 20,000 credit limit.

Are there any other Zero % APR for Life credit cards out there?

Any tricks on increasing the limit such as canceling the CC card and wait til they “invite” you again?

I’ve been doing this for years now and I have one of the cards (spouse has 2). When we started it was one purchase per month; and the newest card is 2. One card had a balance of 12k initially it is now down to less than 4k and my interest pmt is now only 78 cents/mo. The newest was for only 5k and we couldn’t get more (for lack of history) and I used some for actual purchases and some for “savings”.

I had to be very disciplined in making purchases, and instead of driving around I just make two individual purchases on the spot for gas or I use the self service line in some stores at least ten days before the new billing date.

This program works only if you are on top of your financial game and it has really paid off for me. If you don’t get it in the mail you might want to call them for it but it does come and go so don’t rely on it being there.

They used to raise the credit limit but they now want you to use the card so if you don’t they won’ t raise it in time to take advantage of the 0% which used to have an intro period of 12mos now it is about 8 mos.

I’ve been using my Discover for some time now, also with the 0 APR APR. Originally when they approved me it wasn’t a high enough credit limit for me to pay off my auto loan. I had to speak with 3-4 managers and I finally got them to increase my credit line. Off the record I have extensive credit and a score of close to 765. I’ve been making my 2 charges each month. Originally I started to make (2) $1.00 charges at the gas pump. I would charge $1.00 then shut the pump off then charge another $1.00 at the same pump in a second transaction. This saves the hassle of going up the road to another gas station. After a few months I decided to try to make (2) charges of 50 cents each at the gas pump (that doesn’t get much gas these days)… so my APR continues to remain at 0% and over 1 year my total charges is only $12.00 and I’m paying around 53 cents in interest for a $12,000 balance (was higher a while back). I think the card is great. They actually sent me a second application for a 0% for life and I applied for it but was turned down since I owe $$ on some of my other cards. I can’t say anything bad about Discover. I wonder if they knew that people would get by the required 2 charges a month by charging 50 cents.. They aren’t making the interest they had probably hoped.

Guys, I just found a place to make automatic weekly donations or automatic monthly donations online with your discover card. Hopefully this will help people out that are looking for an AUTOMATED way to fulfill their monthly transaction commitment with discover. I have just used this website to make a weekly 50 cent donation for 300 weeks!

Here is the website!

https://www.mysecuredonation.com/all-st-catholic-church.php

So, I received this offer a couple months ago. I applied and was approved and promptly transferred $25,000 from a home equity loan onto the card. The minimum payment is 2%, so $500 isn’t too bad.

BUT… Surprise, surprise!!

Before I even make my first payment, I get a notice that the terms of my card are changing. The minimum payment is increasing to 4% ($1,000/mo). So, instead of avoiding four years of interest on the principal, you only get two.

This is a pretty low move for Discover, in my opinion. As soon as I’m done taking advantage of this offer, the card is getting cancelled.

Thanks Carol!

I can make .25 cents weekly donations. Sweet and it’s tax deductable. Nice find in automating this process.

I have direct pay setup with Discover, so everything is automatic now.

Hi,

Which online donation website accept .25 donation weekly, i would like to set it up also. Can you please post the link for it.

I also received my card on Jan 2005 with 0% for life with a $12K balance transfer from my Home Equity line. The transfer fee was $75. I never carry any balance on a credit card so BIG mistake from me – I thought I can use the card and pay my min payment (2%) and what I have spend for the month. After 2 months I called them and they told me that the payments are only applied against the lowest rate (0%) and the rest is at %13.75. Unfortunately I charged about $650 on the card and over the 2.5 years I’ve paid $360. It runs about $13.80 a month. At $300 payment a month I still have $28 months to pay it off and will pay an additional $378 in bank charges. I did indeed saved a lot more in interest charges from my house equity line.

If anyone knows of another deal like this for 0% for life let me know.

For the people that want to make 2 auto payments a month. If you have a paypal account set up a repeating payment from your paypal to your discover card for something like .25 cents

There is no minimum for my 2 payments a month. I just called them and confirmed. Now I can charge 1 cent from paypal per transaction

I agree with Buck. Why not just charge $.01? Either automatically or at the gas pump.

I am not sure how to do that in Paypal. Buck or Jerad can you explain more? Do you need to have 2 Paypal accounts? Where do you point your paypal payment to go?

If you setup the Discover card on Paypal as your debiting account.

Send .25 to where?

Thanks

Greg

Does it just loop?

So you debit .25 from discover through paypal and back to your paypal account?

Even Better….

Donate!!!

Humane Society

https://secure.hsus.org/01/sustainingmember

There are more out there. Just google “monthly donation”

I’ve got a similar deal with a Citi card and I make 2 one-cent donations via paypal to an online charity as soon as I get my monthly statement (as well as the min payment). So far the only interest has been the BT fee + 50 cents (once) + 2 cents * no. of months

THE CATCH!!!! You must make a minimum payment of 4% if your special introductory rates balance transfers combine for > 90% of the total balance….. there goes my plan to transfer my $28K car loan …. since they would require me to either pay $1140 per month or spend an addition $3000 ( to lower the payment to $560) that would be charging interest @$10.99 -18.99 …..call in 12% apr or 1% per month… if I charge the $3k then make the small .50 charges each month…. I would be charged $30 plus per month until I pay off my balance transfer… sounds like I will be paying ~$2000 in interest after 5 yrs. and I am left with a $5000 balance once my BT is paid off…

Please advise as how to set up paypal account to pay discovercard…Which page in paypal website to navigate…Suggest steps to be performed???

I am reporting back months later to report that is does work! 🙂

I was able to move part of my car loan to my discover card and it works. Yes, there is a minimum finance charge of .50 cents, but that’s peanuts compared to thousands they are lending.

Zero (almost) Percent for LIFE works!

There’s no minimum purchase requirement, so why not charge just two one-cent amounts?

I had a similar offer with Discover, I knew it was too good to be true so I called and sure enough the CSR told me what was written above. This actually sounds like a great deal if you’re in debt (which I’m not) since you don’t have to pay any apr for the transfer, just for purchases (and the transfer fee) after a certain date. I would have applied if not for another card that I have which has 0% apr on purchases till a much much later date … um er 1 year with my 5k limit 🙁 gmflexcard.com — watch out — GM (not Discover?) does a hard pull on your credit if you’re interested in that GM deal (lowers score) 🙁 . If this Discover offer does come around again and I can extend my time to pay back my up to 5k cc “debt” (which is gaining interest in my savings account 🙂 ) I will take it and then pay everything off when the 0% purchase apr stops, although I guess I could fund my paypal account for 2 cents a month — find out the minimum you can purchase first, bet there’s a catch either with the card and/or with paypal 🙂 — I just don’t want to further ruin my credit score by having to pay apr, sigh…. I think the cash back bonus is really good if you actually receive a check in the mail for the “cash back.” So if you’re in cc debt over your ears and need relief go for this Discover deal (though if I know Discover — they’ll reject you 🙂 ), the 0% apr for purchases is still a good deal (timing is just off for me with my GM card).

Any offers for 0% for 6 months on cash advance, other than Visa or Master Card?

Can someone explain how to set up paypal to charge 2 automatic charges from the discover card?

I have TWO Discover cards that I have a 0% for life of the balance transfer. I make 4 purchases per month at the gas pump of approx. 1 gal each and save my receipts. I did have to ‘argue’ with Discover one time and they allowed me the benefit of the doubt. I have had my 1st card for almost 7 years and the second one for almost 2 years now. That is a total of $36,000 at 0%!! I am very diligent. I check my account online every month to make sure the purchases are posted. It is SO worth it. I can’t wait until I pay off the first one which has about $3500 left so I can cancel it and get another one (they will only let you have two at a time). I guess their main money making idea on this is most people either forget to purchase 2x/mo or just use the card for several purchases. There is NO CATCH….I’ve been at this for 6 years and am thrilled.

So they actually let you have 2 at a time in your name solely? I had one for me and one for my wife, but are you saying you have them in your name? I would love to do that.

thanks

I spoke with Discover in Utah today, April 5th 2010. I have the 0% transfer balance for life for about 3 years, initially starting with an $8,000 transfer, now paid down to roughly $4,000. I have diligently made two one cent transactions a month just after my statement at the grocery store (I typically buy a bag of ramen noodles for 14 cents – deposit 13 cents in coins and pay the remainder on the card – I buy two bags of ramen – perform each as a seperate transaction during the same trip to the store and then have satisfied the requirements of the deal.) Today I received a letter from Discover saying that the two monthly purchases were not required in the future to maintain the deal and that I could overpay my next statement and the overage would directly apply to the $90 in purchases over the past three years that was actually accruing interest. It seems that a number of merchants were getting pretty pissed off at Discover for charges under a $1 – charges that they often had to pay more than the actual charge itself. So, in the end, I’ve gotten an $8,000 loan for five years for roughly $50 in interest (though actually a little less since I pay 2% of the amount due each month over the period). Some product manager or vp of sales and promotions at Discover has no doubt been fired and had his back pee’ed on by every Discover employee that did not get a bonus in the past 4 years. I appreciate the free loan – but I wouldn’t invest in this company given the idiocy of the execs in charge. These clowns underestimated the intelligence of the American public and have been served their proper due.

That’s nice. If I don’t have to make two .10 cents purchases a month anymore, that’s extra nice.

I too took out a large 10 grand loan and have only paid peanuts on finance charges 🙂 Not sure who in sales came up with this Zero APR loan, but those of us who took advangage of it as smilling all the way to the bank.

Thanks ex-employee discover person 🙂

Just got notified that 2 monthly purchases are necessary any longer!

I have two of these cards and also just received the same letters. I think Discover has been caught doing something very wrong. Last June, I made my monthly purchases at my Post Office for two 5 cent stamps, for each of my two cards, like I do every month. When my statements arrived, Discover had CHANGED the POST dates on ONE of my cards, by two days. That put that card in default and my interest rate went to 30%. I called and told them that I would get the USPS involved and that the POST dates on my other card, which I used at exactly the same time, had not been changed. I accused Discover of FRAUD and they quickly “reinstated” my 0% !!!! As a “courtesy”. Any lawyers out there? I wonder if I have a case.

Amazing DISCOVER trying to pull a fast one on you. Disgusting.

What I do is that I make two .10 cents Gas purchases a month and I get two receipts at the pump with the date as proof and I have a written receipt should I need it for backups.

CHASE tried to pull a fast one on me a few years ago with a similar situation. I had to fight them tooth and nail, but I prevailed.

As the saying goes, you have to protect your ASSets.

Has anyone received a promotion like this from JP Morgan CHASE? Zero percent for the LIFE OF THE LOAN?

I did and I took advantage of it – or at least I thought I did. I set my card to be paid automatically and signed up for paperless – online statements. Easy?

Well, Chase decided to change the terms of the